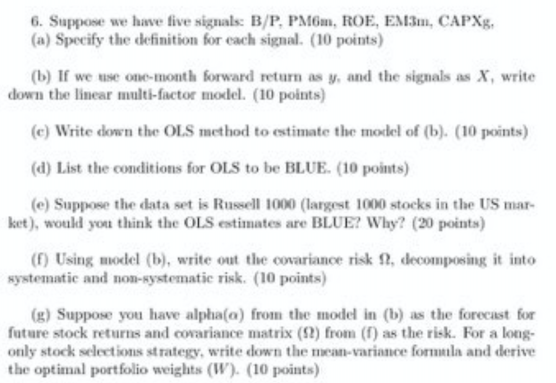

Question

i want full answer if you can please. it will be helpful. However I can understand that according to your policy sometimes you can only

i want full answer if you can please. it will be helpful. However I can understand that according to your policy sometimes you can only answer 1 part. so if you gone answer only one part so please answer part f

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Cases An Active Learning Approach

Authors: Mark S. Beasley, Frank A. Buckless, Steven M. Glover, Douglas F. Prawitt

2nd Edition

0130674842, 978-0130674845