Question

I would like to get help completing this problem. I was working on it and got all the way up to requirement #4 and got

I would like to get help completing this problem. I was working on it and got all the way up to requirement #4 and got stuck. I am struggling to grasp the concept of how to properly record the trade-in, etc. I'm attaching my working copy.

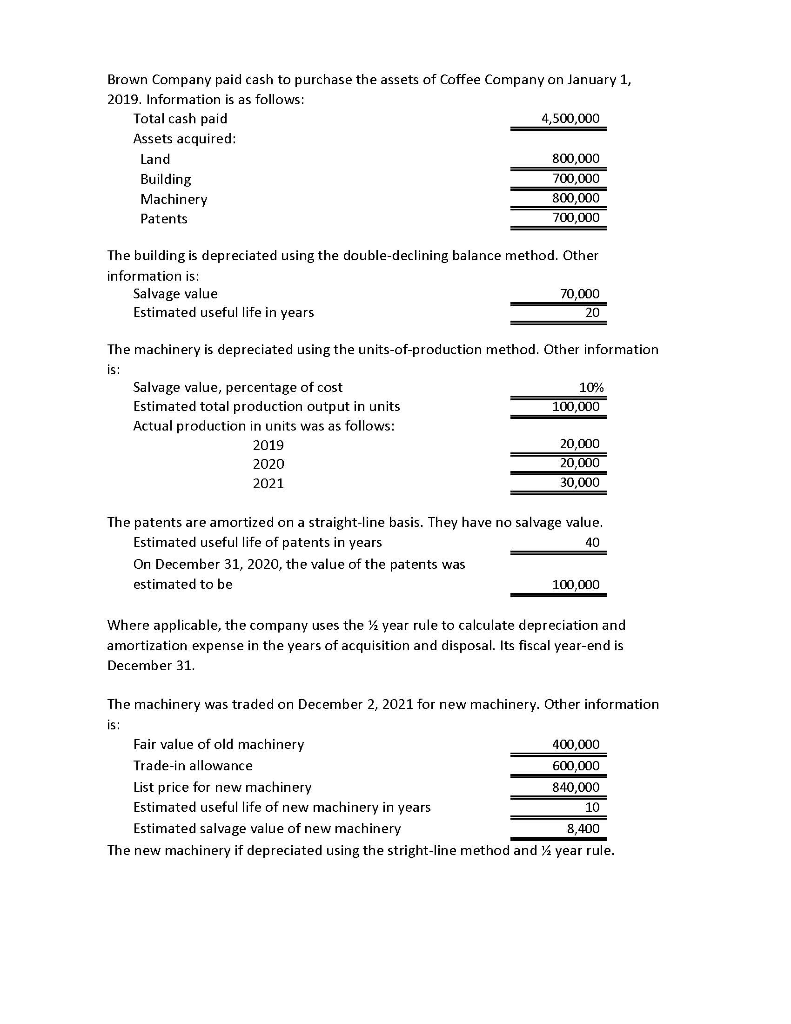

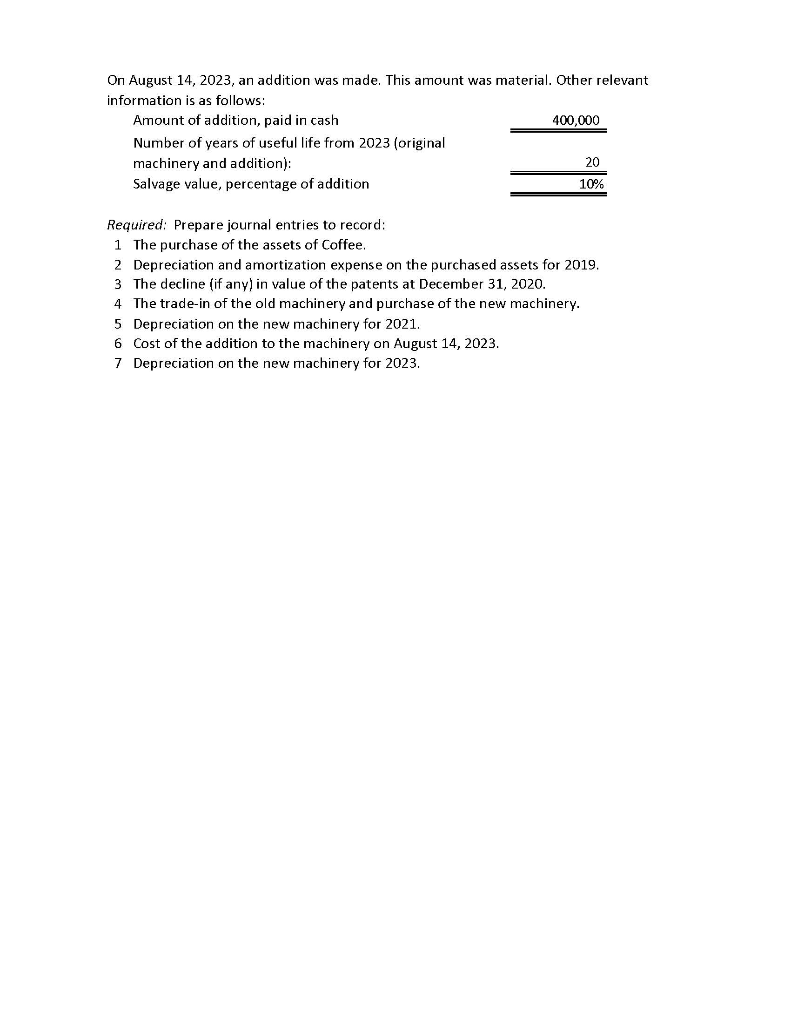

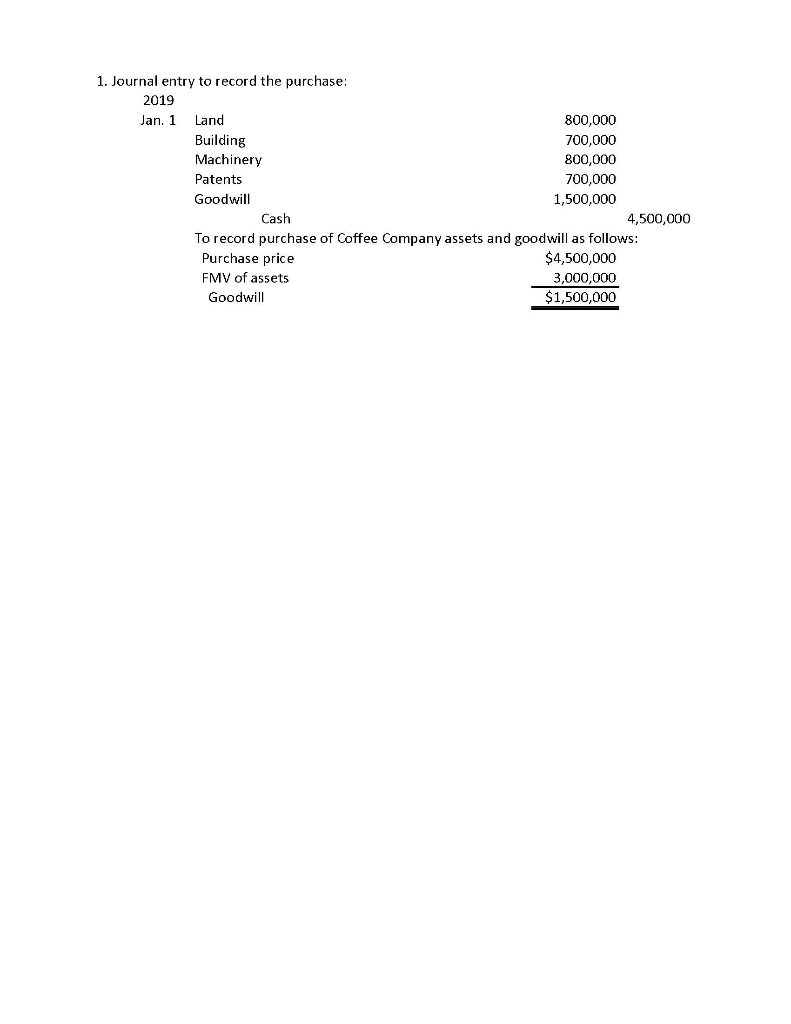

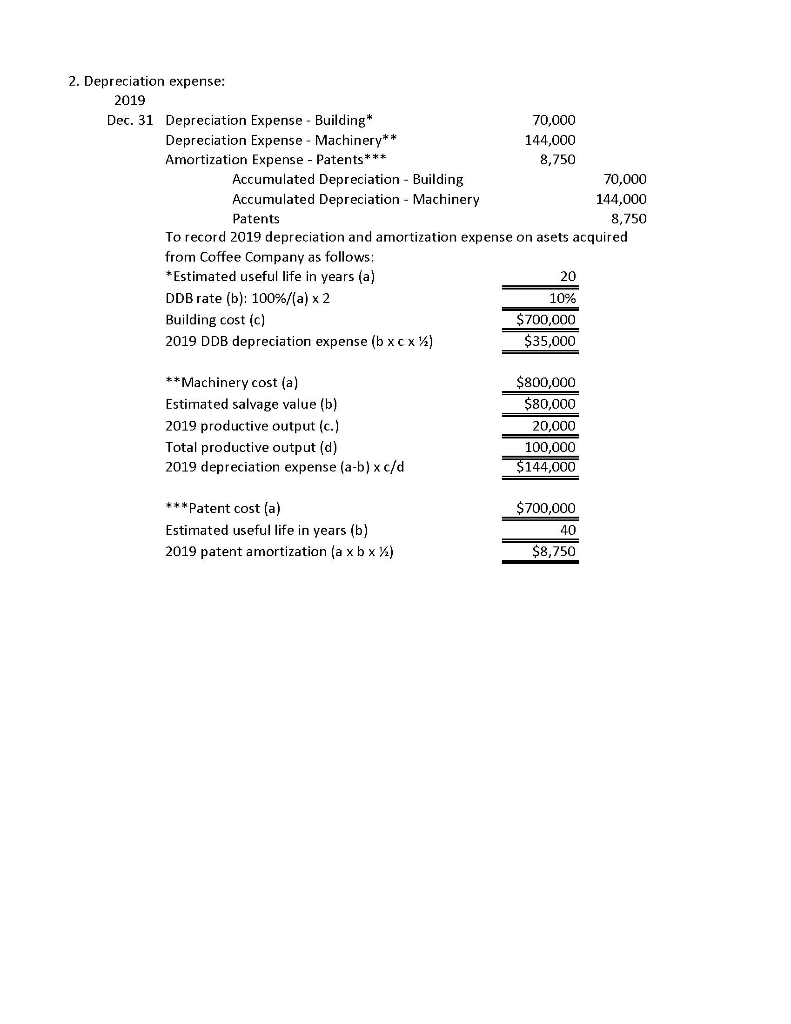

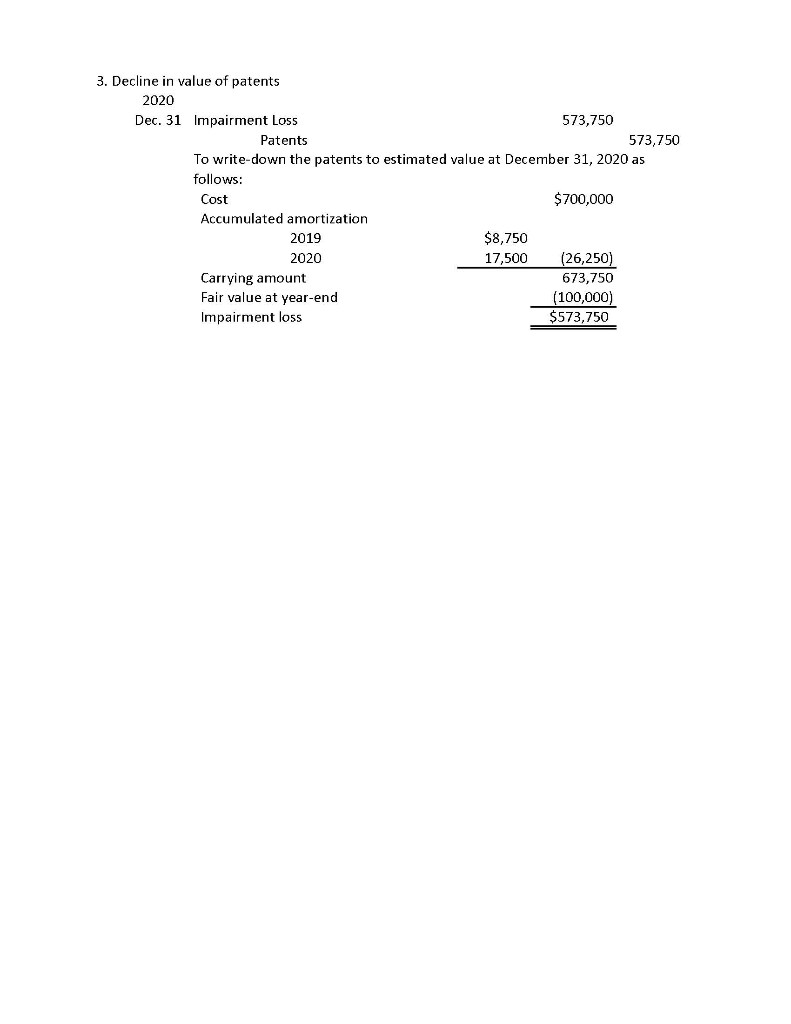

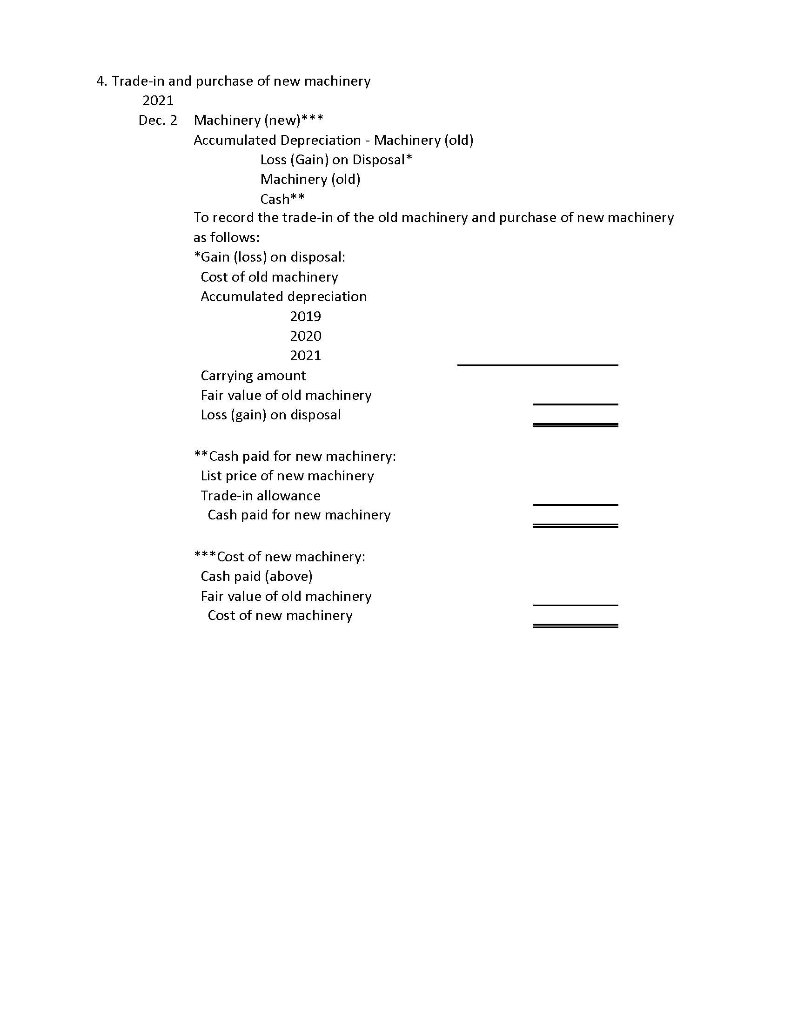

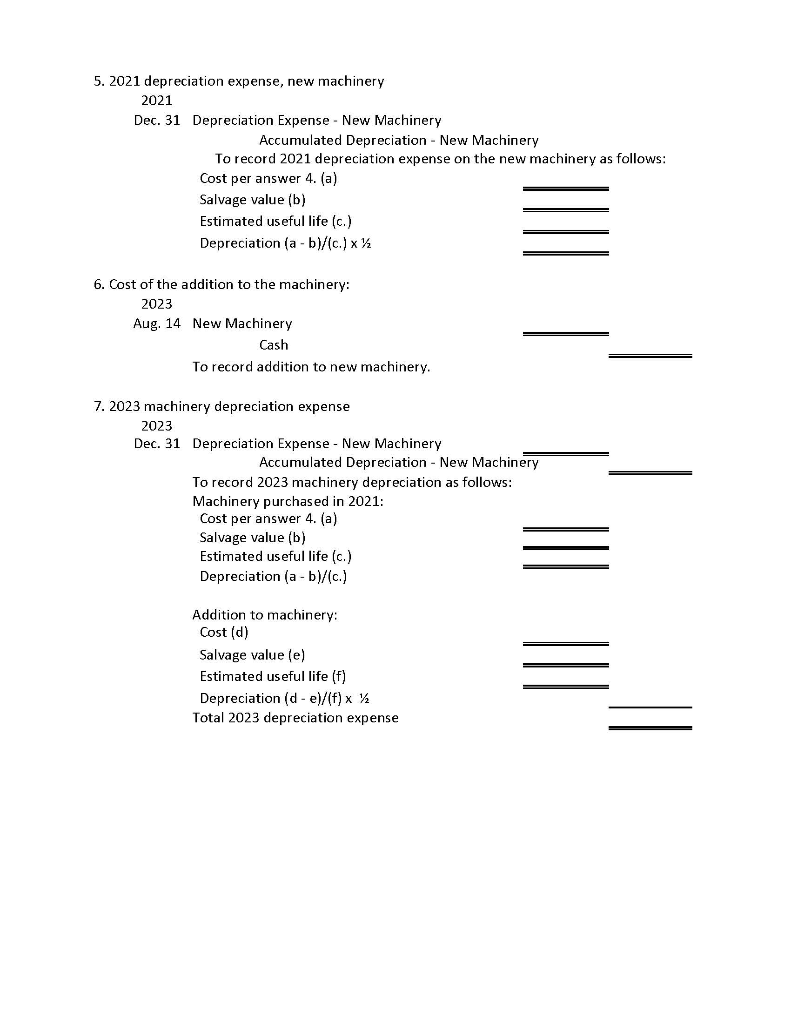

Brown Company paid cash to purchase the assets of Coffee Company on January 1, 2019. Information is as follows: Total cash paid 4,500,000 Assets acquired: Land 800,000 Building 700,000 Machinery 800,000 Patents 700,000 The building is depreciated using the double-declining balance method. Other information is: Salvage value 70,000 Estimated useful life in years 20 The machinery is depreciated using the units-of-production method. Other information is: Salvage value, percentage of cost 10% Estimated total production output in units 100,000 Actual production in units was as follows: 2019 20,000 2020 20,000 2021 30,000 The patents are amortized on a straight-line basis. They have no salvage value. Estimated useful life of patents in years 40 On December 31, 2020, the value of the patents was estimated to be 100,000 Where applicable, the company uses the year rule to calculate depreciation and amortization expense in the years of acquisition and disposal. Its fiscal year-end is December 31. The machinery was traded on December 2, 2021 for new machinery. Other information is: Fair value of old machinery 400,000 Trade-in allowance 600,000 List price for new machinery 840,000 Estimated useful life of new machinery in years 10 Estimated salvage value of new machinery 8,400 The new machinery if depreciated using the stright-line method and / year rule. On August 14, 2023, an addition was made. This amount was material. Other relevant information is as follows: Amount of addition, paid in cash 400,000 Number of years of useful life from 2023 (original machinery and addition): 20 Salvage value, percentage of addition 10% Required: Prepare journal entries to record: 1 The purchase of the assets of Coffee. 2 Depreciation and amortization expense on the purchased assets for 2019. 3 The decline (if any) in value of the patents at December 31, 2020. 4 The trade-in of the old machinery and purchase of the new machinery. 5 Depreciation on the new machinery for 2021. 6 Cost of the addition to the machinery on August 14, 2023. 7 Depreciation on the new machinery for 2023. 1. Journal entry to record the purchase: 2019 Jan. 1 Land 800,000 Building 700,000 Machinery 800,000 Patents 700,000 Goodwill 1,500,000 Cash 4,500,000 To record purchase of Coffee Company assets and goodwill as follows: Purchase price $4,500,000 FMV of assets 3,000,000 Goodwill $1,500,000 2. Depreciation expense: 2019 Dec. 31 Depreciation Expense - Building* 70,000 Depreciation Expense - Machinery** 144,000 Amortization Expense - Patents*** 8,750 Accumulated Depreciation - Building 70,000 Accumulated Depreciation - Machinery 144,000 Patents 8,750 To record 2019 depreciation and amortization expense on asets acquired from Coffee Company as follows: * Estimated useful life in years (a) 20 DDB rate (b): 100%/(a) x 2 10% Building cost (c) $700,000 2019 DDB depreciation expense (bxcx) $35,000 $800,000 $80,000 **Machinery cost (a) Estimated salvage value (b) 2019 productive output (c.) Total productive output (d) 2019 depreciation expense (a-b)xc/d 20,000 100,000 $144,000 $700,000 ***Patent cost (a) Estimated useful life in years (b) 2019 patent amortization (a xbx) 40 $8,750 3. Decline in value of patents 2020 Dec. 31 Impairment Loss 573,750 Patents 573,750 To write down the patents to estimated value at December 31, 2020 as follows: Cost $700,000 Accumulated amortization 2019 $8,750 2020 17,500 (26,250) Carrying amount 673,750 Fair value at year-end (100,000) Impairment loss $573.750 4. Trade-in and purchase of new machinery 2021 Dec. 2 Machinery (new)*** Accumulated Depreciation - Machinery (old) Loss (Gain) on Disposal* Machinery (old) Cash ** To record the trade-in of the old machinery and purchase of new machinery as follows: *Gain (loss) on disposal: Cost of old machinery Accumulated depreciation 2019 2020 2021 Carrying amount Fair value of old machinery Loss (gain) on disposal ** Cash paid for new machinery: List price of new machinery Trade-in allowance Cash paid for new machinery *** Cost of new machinery: Cash paid (above) Fair value of old machinery Cost of new machinery 5. 2021 depreciation expense, new machinery 2021 Dec. 31 Depreciation Expense - New Machinery Accumulated Depreciation - New Machinery To record 2021 depreciation expense the new machinery as follows: Cost per answer 4. (a) Salvage value (b) Estimated useful life (c.) Depreciation (a - b)/(c.)x = 6. Cost of the addition to the machinery: 2023 Aug. 14 New Machinery Cash To record addition to new machinery. 7. 2023 machinery depreciation expense 2023 Dec. 31 Depreciation Expense - New Machinery Accumulated Depreciation - New nery To record 2023 machinery depreciation as follows: Machinery purchased in 2021: Cost per answer 4. (a) Salvage value (b) Estimated useful life (c.) Depreciation (a - b)/(c.) Addition to machinery: Cost (d) Salvage value (e) Estimated useful life (f) Depreciation ( de)/(f) x Total 2023 depreciation expense

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting An Introduction To Concepts Methods And Uses

Authors: Sidney Davidson, Roman L. Weil, Clyde P. Stickney

2nd Edition

0030452961, 978-0030452963