Answered step by step

Verified Expert Solution

Question

1 Approved Answer

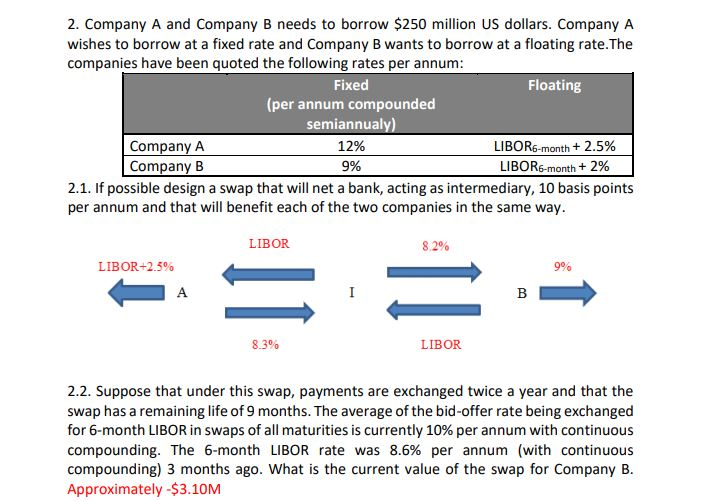

i would like to know how they go the answers in red pleas ASAP 2. Company A and Company B needs to borrow $250 million

i would like to know how they go the answers in red pleas ASAP

2. Company A and Company B needs to borrow $250 million US dollars. Company A wishes to borrow at a fixed rate and Company B wants to borrow at a floating rate.The companies have been quoted the following rates per annum: Fixed Floating (per annum compounded semiannualy) Company A 12% LIBOR6-month + 2.5% Company B 9% LIBOR6-month + 2% 2.1. If possible design a swap that will net a bank, acting as intermediary, 10 basis points per annum and that will benefit each of the two companies in the same way. LIBOR 8.2% LIBOR+2.5% 9% A I = 09 8.3% LIBOR 2.2. Suppose that under this swap, payments are exchanged twice a year and that the swap has a remaining life of 9 months. The average of the bid-offer rate being exchanged for 6-month LIBOR in swaps of all maturities is currently 10% per annum with continuous compounding. The 6-month LIBOR rate was 8.6% per annum (with continuous compounding) 3 months ago. What is the current value of the swap for Company B. Approximately -$3.10M 2. Company A and Company B needs to borrow $250 million US dollars. Company A wishes to borrow at a fixed rate and Company B wants to borrow at a floating rate.The companies have been quoted the following rates per annum: Fixed Floating (per annum compounded semiannualy) Company A 12% LIBOR6-month + 2.5% Company B 9% LIBOR6-month + 2% 2.1. If possible design a swap that will net a bank, acting as intermediary, 10 basis points per annum and that will benefit each of the two companies in the same way. LIBOR 8.2% LIBOR+2.5% 9% A I = 09 8.3% LIBOR 2.2. Suppose that under this swap, payments are exchanged twice a year and that the swap has a remaining life of 9 months. The average of the bid-offer rate being exchanged for 6-month LIBOR in swaps of all maturities is currently 10% per annum with continuous compounding. The 6-month LIBOR rate was 8.6% per annum (with continuous compounding) 3 months ago. What is the current value of the swap for Company B. Approximately -$3.10MStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Return Distributions In Finance

Authors: Stephen Satchell, John Knight

1st Edition

0750647515, 978-0750647519