Question

If Alejandro names Mercedes as the successor annuitant of his spousal RRIF, and he subsequently dies in 2028, what are the tax consequences? Successor annuitant

If Alejandro names Mercedes as the successor annuitant of his spousal RRIF, and he subsequently dies in 2028, what are the tax consequences?

Successor annuitant is (more or less) the same thing as a “beneficiary”. So if Alejandro arranges to do this for Mercedes, why would he do it and what are the financial benefits, and what are the tax consequences if Alejandro dies?

How much of the $75,000 long service payment, if any, can Mercedes shelter from tax?

Some companies will offer senior management who have worked for a company as a loyal employee for many years a special, lump-sum, payment when they retire? If Mercedes receives a payment like this, what are the tax issues (if any) for Mercedes and the company?

What are the implications, if any, of Mercedes transferring the eligible portion of the retiring allowance discussed in question #4 above to a spousal RRSP where she is the contributor?

If Mercedes receives this payment from her company, what are the rules and tax issues if she wants to transfer all, or some, of this payment into the spousal RRSP in Alejandro’s name?

Assume the maximum annual pension entitlement for a defined benefit pension plan has not changed over the last nine (9) years and is still $2,697 per year of service.

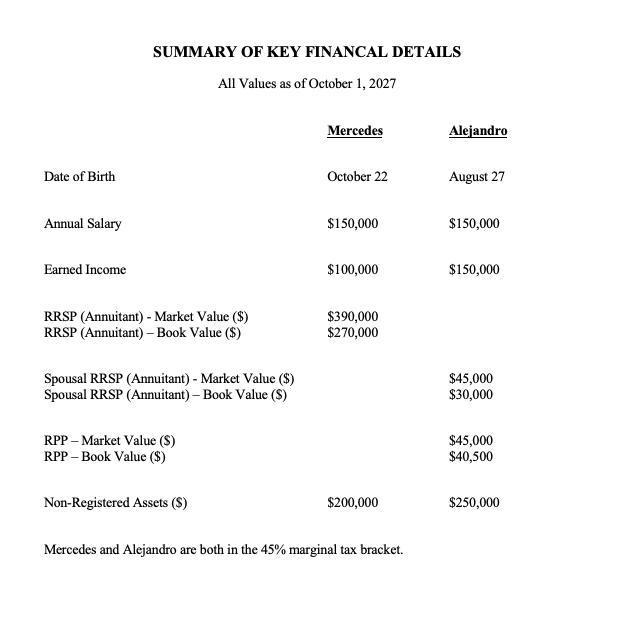

It is now nine years later and things have changed. Mercedes and Alejandro will be ages 60 and 62, respectively, on January 1, 2028 and they have decided that they would like to retire within the next few months. They both feel that they have sufficient income and savings that will allow them to enjoy a comfortable lifestyle during retirement, but they have never worked with a financial advisor, so this assumption is simply a feeling they have. Therefore, before making the final decision about retirement, the San Martin's have approached you (now October 2027) to help them assess their financial decision relative to the important decision. Alejandro now holds a senior management position with Shoppers Drug Mart, where he has worked for the past three years. Prior to this job, he worked for Grande Pharmacia for roughly 27 years. When Alejandro left Grande Pharmacia, he decided to take a deferred annuity, to begin at age 65, as the settlement of his pension options. His deferred annuity is a life annuity with a 100% survivor option. The monthly payment of $2,200 begins at the end of the month in which he reaches age 65. At Shoppers Drug Mart, Alejandro participates in a defined contribution pension plan, which he joined at the time he was hired. The market value of his pension assets is $45,000, while the book value is $40,500. The plan allows for a two-year vesting period. Upon termination of employment, or at retirement, the pension plan allows funds to transfer to a LIRA, provided the individual is age 71 or less during the year when the transfer occurs. Mercedes is now the Vice-President of Finance for Starlight Inc. Six years ago, the company established an individual pension plan for their senior executives, which included Mercedes. This non-contributory IPP provides a 2% benefit for each year of service at the company and is based on career average earnings. At present, Mercedes has six years of participation in the plan, prior to which she did not participate in any pension plan. Mercedes began working at Starlight on July 1, 2012. She has been discussing the possibility of retirement with her employer and they have offered her a $75,000 payment in recognition of her long service with the company. Prior to her participation in the IPP, Mercedes contributed regularly to an RRSP and has accumulated substantial assets. During that period, she made $45,000 in contributions to a spousal RRSP, where she was the contributor and Alejandro was the annuitant. For Mercedes and Alejandro, the time has come and retirement is now right around the corner. They now want to know whether the retirement plan they have been building will provide long- term financial security for them after they stop working. So they are looking for your help and have given you the following list of questions to answer for them. For any calculations, assume that the market value and book value of the assets remain unchanged between October 1, 2027 and January 1, 2028. Also, only use information in Part 2 of this case to

Step by Step Solution

3.40 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

If Alejandro names Mercedes as the successor annuitant of his spousal RRIF and he subsequently dies in 2028 what are the tax consequences If Alejandro names Mercedes as the successor annuitant of his ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

South Western Federal Taxation 2016 Corporations Partnerships Estates And Trusts

Authors: James Boyd, William Hoffman, Raabe, David Maloney, Young

39th Edition

978-1305399884