if anyone can do this on excel and are able to email it to me I would be more than thankful!

thank you in advance!

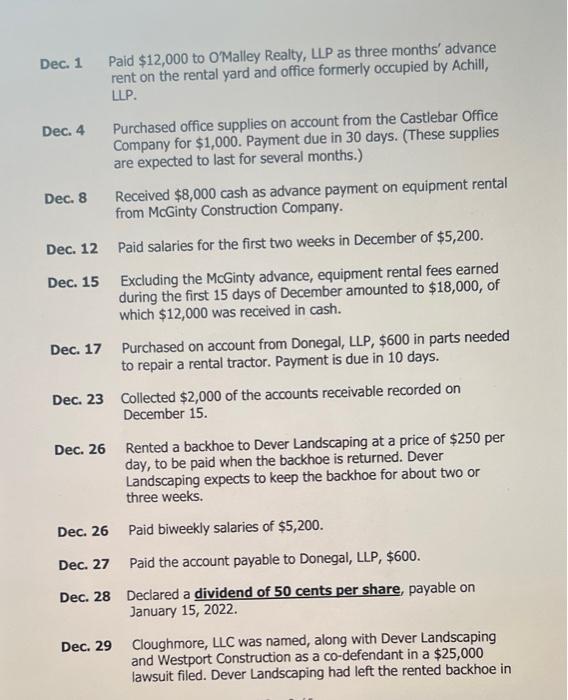

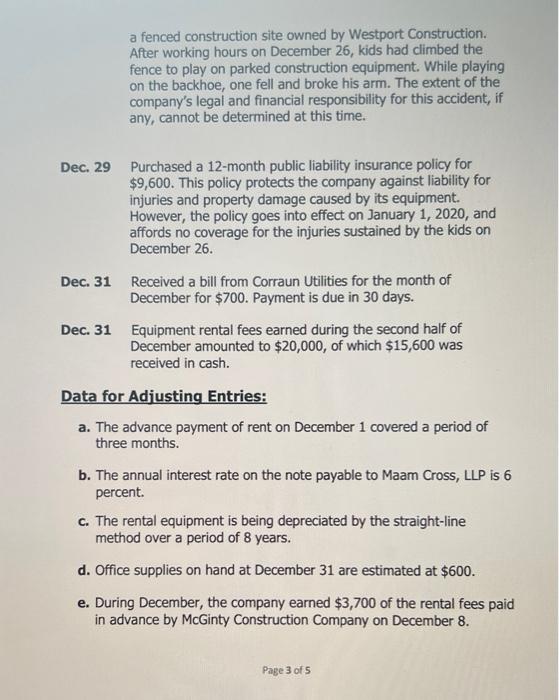

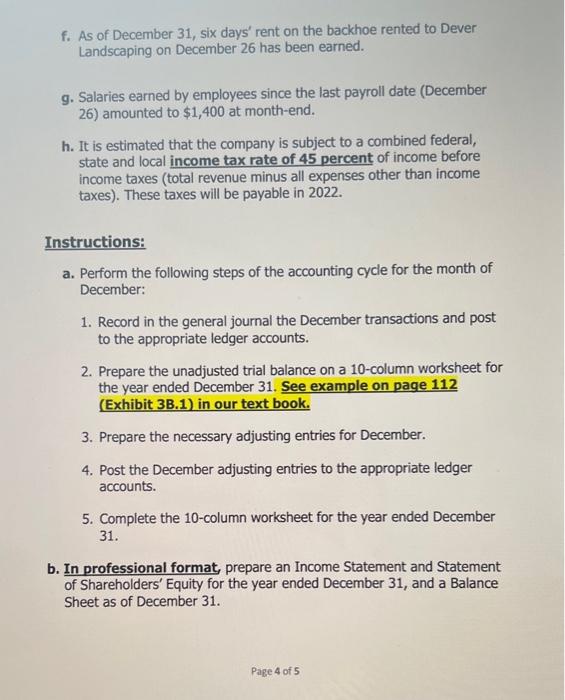

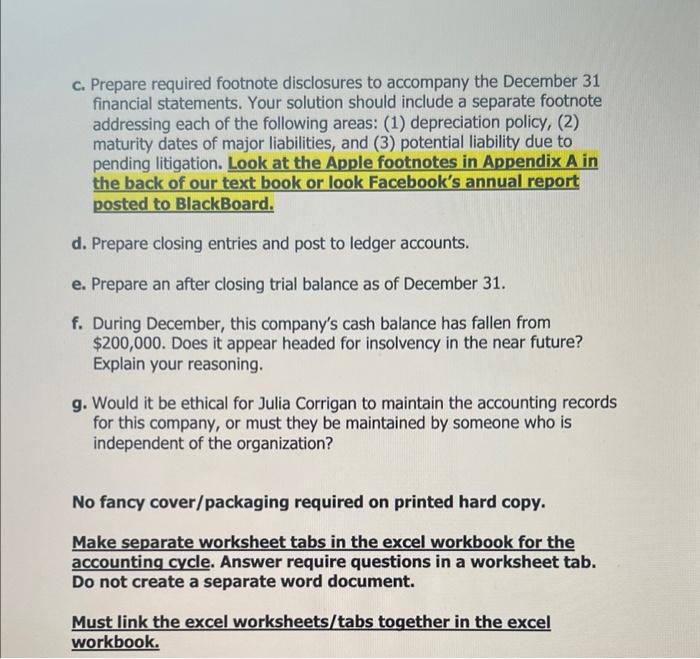

A COMPREHENSIVE ACCOUNTING CYCLE PROBLEM On December 1, 2021, Thomas and Julia Corrigan formed Cloughmore, LLC. They began operations using the following accounts: Cash Income Taxes Payable Capital Stock Accounts Receivable Prepaid Rent Retained Earnings Dividends Unexpired Insurance Office Supplies Income Summary Rental Fees Earned Rental Equipment Salaries Expense Accumulated Depreciation: Rental Equipment Maintenance Expense Utilities Expense Notes Payable Accounts Payable Rent Expense Interest Payable Salaries Payable Dividends Payable Office Supplies Expense Depreciation Expense Interest Expense Income Taxes Expense Unearned Rental Fees The LLC performs adjusting entries monthly. Closing entries are performed annually on December 31. During December, the LLC entered into the following transactions: Dec. 1 Issued to Thomas and Julia Corrigan 1,000 shares of capital stock in exchange for a total of $200,000 cash. Dec. 1 Purchased for $240,000 the equipment formally owned by a competitor named Maam Cross, LLP. Paid $140,000 cash and issued a one year note payable for $100,000. The note, plus all 12 months of accrued interest, are due November 30, 2022. Dec. 1 Paid $12,000 to O'Malley Realty, LLP as three months' advance rent on the rental yard and office formerly occupied by Achill, LLP. Dec. 4 Purchased office supplies on account from the Castlebar Office Company for $1,000. Payment due in 30 days. (These supplies are expected to last for several months.) Dec. 8 Received $8,000 cash as advance payment on equipment rental from McGinty Construction Company. Dec. 12 Paid salaries for the first two weeks in December of $5,200. Dec. 15 Excluding the McGinty advance, equipment rental fees earned during the first 15 days of December amounted to $18,000, of which $12,000 was received in cash. Dec. 17 Purchased on account from Donegal, LLP, $600 in parts needed to repair a rental tractor. Payment is due in 10 days. Dec. 23 Collected $2,000 of the accounts receivable recorded on December 15. Dec. 26 Rented a backhoe to Dever Landscaping at a price of $250 per day, to be paid when the backhoe is returned. Dever Landscaping expects to keep the backhoe for about two or three weeks. Dec. 26 Paid biweekly salaries of $5,200. Dec. 27 Paid the account payable to Donegal, LLP, $600. Dec. 28 Declared a dividend of 50 cents per share, payable on January 15, 2022. Dec. 29 Cloughmore, LLC was named, along with Dever Landscaping and Westport Construction as a co-defendant in a $25,000 lawsuit filed. Dever Landscaping had left the rented backhoe in a fenced construction site owned by Westport Construction. After working hours on December 26, kids had climbed the fence to play on parked construction equipment. While playing on the backhoe, one fell and broke his arm. The extent of the company's legal and financial responsibility for this accident, if any, cannot be determined at this time. Dec. 29 Purchased a 12-month public liability insurance policy for $9,600. This policy protects the company against liability for injuries and property damage caused by its equipment. However, the policy goes into effect on January 1, 2020, and affords no coverage for the injuries sustained by the kids on December 26. Dec. 31 Received a bill from Corraun Utilities for the month of December for $700. Payment is due in 30 days. Dec. 31 Equipment rental fees earned during the second half of December amounted to $20,000, of which $15,600 was received in cash. Data for Adjusting Entries: a. The advance payment of rent on December 1 covered a period of three months. b. The annual interest rate on the note payable to Maam Cross, LLP is 6 percent. c. The rental equipment is being depreciated by the straight-line method over a period of 8 years. d. Office supplies on hand at December 31 are estimated at $600. e. During December, the company earned $3,700 of the rental fees paid in advance by McGinty Construction Company on December 8. Page 3 of 5 f. As of December 31, six days' rent on the backhoe rented to Dever Landscaping on December 26 has been earned. g. Salaries earned by employees since the last payroll date (December 26) amounted to $1,400 at month-end. h. It is estimated that the company is subject to a combined federal, state and local income tax rate of 45 percent of income before income taxes (total revenue minus all expenses other than income taxes). These taxes will be payable in 2022. Instructions: a. Perform the following steps of the accounting cycle for the month of December: 1. Record in the general journal the December transactions and post to the appropriate ledger accounts. 2. Prepare the unadjusted trial balance on a 10-column worksheet for the year ended December 31. See example on page 112 (Exhibit 3B.1) in our text book. 3. Prepare the necessary adjusting entries for December. 4. Post the December adjusting entries to the appropriate ledger accounts. 5. Complete the 10-column worksheet for the year ended December 31. b. In professional format, prepare an Income Statement and Statement of Shareholders' Equity for the year ended December 31, and a Balance Sheet as of December 31. Page 4 of 5 c. Prepare required footnote disclosures to accompany the December 31 financial statements. Your solution should include a separate footnote addressing each of the following areas: (1) depreciation policy, (2) maturity dates of major liabilities, and (3) potential liability due to pending litigation. Look at the Apple footnotes in Appendix A in the back of our text book or look Facebook's annual report posted to BlackBoard. d. Prepare closing entries and post to ledger accounts. e. Prepare an after closing trial balance as of December 31. f. During December, this company's cash balance has fallen from $200,000. Does it appear headed for insolvency in the near future? Explain your reasoning. g. Would it be ethical for Julia Corrigan to maintain the accounting records for this company, or must they be maintained by someone who is independent of the organization? No fancy cover/packaging required on printed hard copy. Make separate worksheet tabs in the excel workbook for the accounting cycle. Answer require questions in a worksheet tab. Do not create a separate word document. Must link the excel worksheets/tabs together in the excel workbook. A COMPREHENSIVE ACCOUNTING CYCLE PROBLEM On December 1, 2021, Thomas and Julia Corrigan formed Cloughmore, LLC. They began operations using the following accounts: Cash Income Taxes Payable Capital Stock Accounts Receivable Prepaid Rent Retained Earnings Unexpired Insurance Dividends Office Supplies Income Summary Rental Equipment Rental Fees Earned Accumulated Depreciation: Rental Equipment Salaries Expense Maintenance Expense Notes Payable Utilities Expense Rent Expense Accounts Payable Office Supplies Expense Interest Payable Salaries Payable Dividends Payable Depreciation Expense Interest Expense Income Taxes Expense Unearned Rental Fees The LLC performs adjusting entries monthly. Closing entries are performed annually on December 31. During December, the LLC entered into the following transactions: Dec. 1 Issued to Thomas and Julia Corrigan 1,000 shares of capital stock in exchange for a total of $200,000 cash. Dec. 1 Purchased for $240,000 the equipment formally owned by a competitor named Maam Cross, LLP. Paid $140,000 cash and issued a one year note payable for $100,000. The note, plus all 12 months of accrued interest, are due November 30, 2022. Page 1 of 5 A COMPREHENSIVE ACCOUNTING CYCLE PROBLEM On December 1, 2021, Thomas and Julia Corrigan formed Cloughmore, LLC. They began operations using the following accounts: Cash Income Taxes Payable Capital Stock Accounts Receivable Prepaid Rent Retained Earnings Dividends Unexpired Insurance Office Supplies Income Summary Rental Fees Earned Rental Equipment Salaries Expense Accumulated Depreciation: Rental Equipment Maintenance Expense Utilities Expense Notes Payable Accounts Payable Rent Expense Interest Payable Salaries Payable Dividends Payable Office Supplies Expense Depreciation Expense Interest Expense Income Taxes Expense Unearned Rental Fees The LLC performs adjusting entries monthly. Closing entries are performed annually on December 31. During December, the LLC entered into the following transactions: Dec. 1 Issued to Thomas and Julia Corrigan 1,000 shares of capital stock in exchange for a total of $200,000 cash. Dec. 1 Purchased for $240,000 the equipment formally owned by a competitor named Maam Cross, LLP. Paid $140,000 cash and issued a one year note payable for $100,000. The note, plus all 12 months of accrued interest, are due November 30, 2022. Dec. 1 Paid $12,000 to O'Malley Realty, LLP as three months' advance rent on the rental yard and office formerly occupied by Achill, LLP. Dec. 4 Purchased office supplies on account from the Castlebar Office Company for $1,000. Payment due in 30 days. (These supplies are expected to last for several months.) Dec. 8 Received $8,000 cash as advance payment on equipment rental from McGinty Construction Company. Dec. 12 Paid salaries for the first two weeks in December of $5,200. Dec. 15 Excluding the McGinty advance, equipment rental fees earned during the first 15 days of December amounted to $18,000, of which $12,000 was received in cash. Dec. 17 Purchased on account from Donegal, LLP, $600 in parts needed to repair a rental tractor. Payment is due in 10 days. Dec. 23 Collected $2,000 of the accounts receivable recorded on December 15. Dec. 26 Rented a backhoe to Dever Landscaping at a price of $250 per day, to be paid when the backhoe is returned. Dever Landscaping expects to keep the backhoe for about two or three weeks. Dec. 26 Paid biweekly salaries of $5,200. Dec. 27 Paid the account payable to Donegal, LLP, $600. Dec. 28 Declared a dividend of 50 cents per share, payable on January 15, 2022. Dec. 29 Cloughmore, LLC was named, along with Dever Landscaping and Westport Construction as a co-defendant in a $25,000 lawsuit filed. Dever Landscaping had left the rented backhoe in a fenced construction site owned by Westport Construction. After working hours on December 26, kids had climbed the fence to play on parked construction equipment. While playing on the backhoe, one fell and broke his arm. The extent of the company's legal and financial responsibility for this accident, if any, cannot be determined at this time. Dec. 29 Purchased a 12-month public liability insurance policy for $9,600. This policy protects the company against liability for injuries and property damage caused by its equipment. However, the policy goes into effect on January 1, 2020, and affords no coverage for the injuries sustained by the kids on December 26. Dec. 31 Received a bill from Corraun Utilities for the month of December for $700. Payment is due in 30 days. Dec. 31 Equipment rental fees earned during the second half of December amounted to $20,000, of which $15,600 was received in cash. Data for Adjusting Entries: a. The advance payment of rent on December 1 covered a period of three months. b. The annual interest rate on the note payable to Maam Cross, LLP is 6 percent. c. The rental equipment is being depreciated by the straight-line method over a period of 8 years. d. Office supplies on hand at December 31 are estimated at $600. e. During December, the company earned $3,700 of the rental fees paid in advance by McGinty Construction Company on December 8. Page 3 of 5 f. As of December 31, six days' rent on the backhoe rented to Dever Landscaping on December 26 has been earned. g. Salaries earned by employees since the last payroll date (December 26) amounted to $1,400 at month-end. h. It is estimated that the company is subject to a combined federal, state and local income tax rate of 45 percent of income before income taxes (total revenue minus all expenses other than income taxes). These taxes will be payable in 2022. Instructions: a. Perform the following steps of the accounting cycle for the month of December: 1. Record in the general journal the December transactions and post to the appropriate ledger accounts. 2. Prepare the unadjusted trial balance on a 10-column worksheet for the year ended December 31. See example on page 112 (Exhibit 3B.1) in our text book. 3. Prepare the necessary adjusting entries for December. 4. Post the December adjusting entries to the appropriate ledger accounts. 5. Complete the 10-column worksheet for the year ended December 31. b. In professional format, prepare an Income Statement and Statement of Shareholders' Equity for the year ended December 31, and a Balance Sheet as of December 31. Page 4 of 5 c. Prepare required footnote disclosures to accompany the December 31 financial statements. Your solution should include a separate footnote addressing each of the following areas: (1) depreciation policy, (2) maturity dates of major liabilities, and (3) potential liability due to pending litigation. Look at the Apple footnotes in Appendix A in the back of our text book or look Facebook's annual report posted to BlackBoard. d. Prepare closing entries and post to ledger accounts. e. Prepare an after closing trial balance as of December 31. f. During December, this company's cash balance has fallen from $200,000. Does it appear headed for insolvency in the near future? Explain your reasoning. g. Would it be ethical for Julia Corrigan to maintain the accounting records for this company, or must they be maintained by someone who is independent of the organization? No fancy cover/packaging required on printed hard copy. Make separate worksheet tabs in the excel workbook for the accounting cycle. Answer require questions in a worksheet tab. Do not create a separate word document. Must link the excel worksheets/tabs together in the excel workbook. A COMPREHENSIVE ACCOUNTING CYCLE PROBLEM On December 1, 2021, Thomas and Julia Corrigan formed Cloughmore, LLC. They began operations using the following accounts: Cash Income Taxes Payable Capital Stock Accounts Receivable Prepaid Rent Retained Earnings Unexpired Insurance Dividends Office Supplies Income Summary Rental Equipment Rental Fees Earned Accumulated Depreciation: Rental Equipment Salaries Expense Maintenance Expense Notes Payable Utilities Expense Rent Expense Accounts Payable Office Supplies Expense Interest Payable Salaries Payable Dividends Payable Depreciation Expense Interest Expense Income Taxes Expense Unearned Rental Fees The LLC performs adjusting entries monthly. Closing entries are performed annually on December 31. During December, the LLC entered into the following transactions: Dec. 1 Issued to Thomas and Julia Corrigan 1,000 shares of capital stock in exchange for a total of $200,000 cash. Dec. 1 Purchased for $240,000 the equipment formally owned by a competitor named Maam Cross, LLP. Paid $140,000 cash and issued a one year note payable for $100,000. The note, plus all 12 months of accrued interest, are due November 30, 2022. Page 1 of 5