Answered step by step

Verified Expert Solution

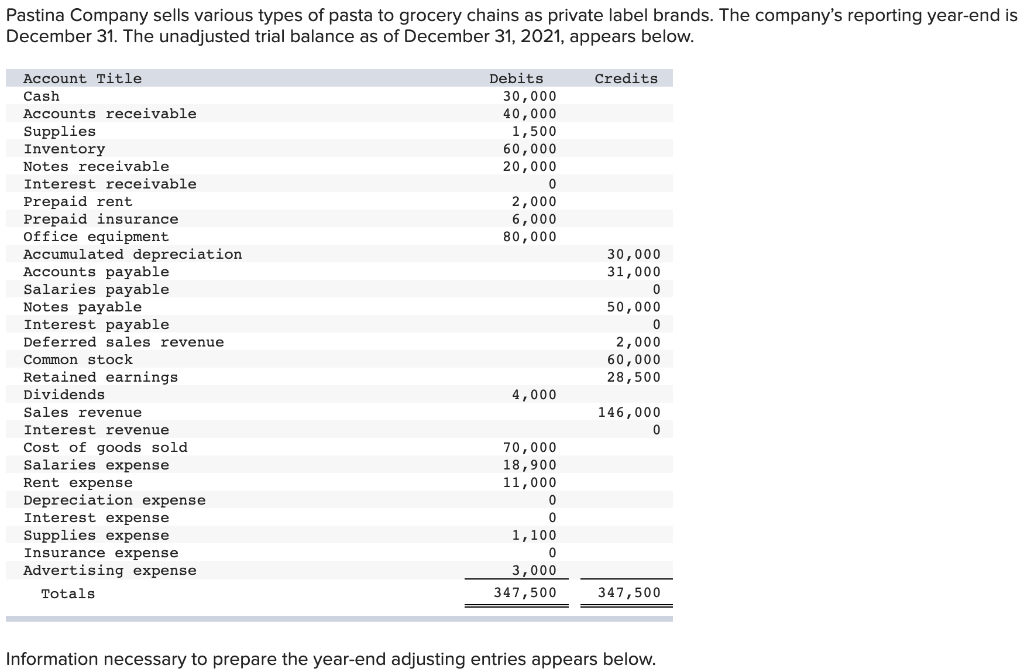

Question

1 Approved Answer

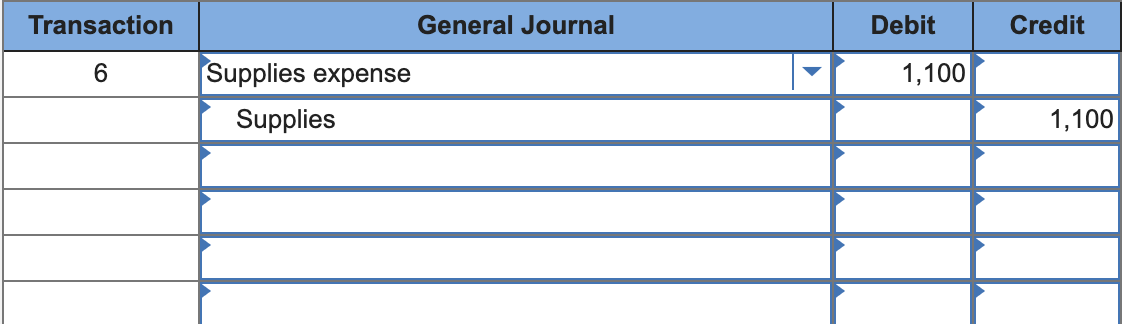

I'm having trouble finding out where I'm going wrong, I've tried $1,100 & $300 ($1100-$800) were both counted as wrong. What am I missing here?

I'm having trouble finding out where I'm going wrong, I've tried $1,100 & $300 ($1100-$800) were both counted as wrong. What am I missing here? Thanks in advance!

I'm having trouble finding out where I'm going wrong, I've tried $1,100 & $300 ($1100-$800) were both counted as wrong. What am I missing here? Thanks in advance!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Principle And Practice

Authors: Satyabrata Tripathy

1st Edition

9332519382, 9789332519381