Answered step by step

Verified Expert Solution

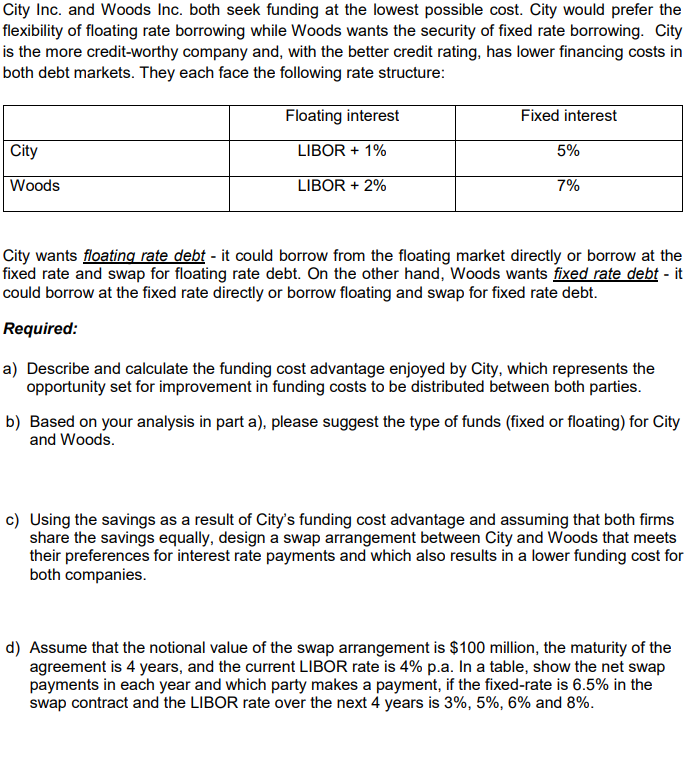

Question

1 Approved Answer

I'm trying these with a friend, but still can't make it through. I would appreciate if anyone can help asap. even if you don't know

I'm trying these with a friend, but still can't make it through. I would appreciate if anyone can help asap. even if you don't know whole things, partly also would be great, Thank you.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Trends Of Modernization In Budgeting And Finance

Authors: Denis Ushakov

1st Edition

1522577602,1522577610