Answered step by step

Verified Expert Solution

Question

1 Approved Answer

IMA EDUCATIONAL Case Case Journal Study Lone Star Lodging Thomas Calderon University of Akron INTRODUCTION James W. Hesford* University of Lethbridge Dhillon School of

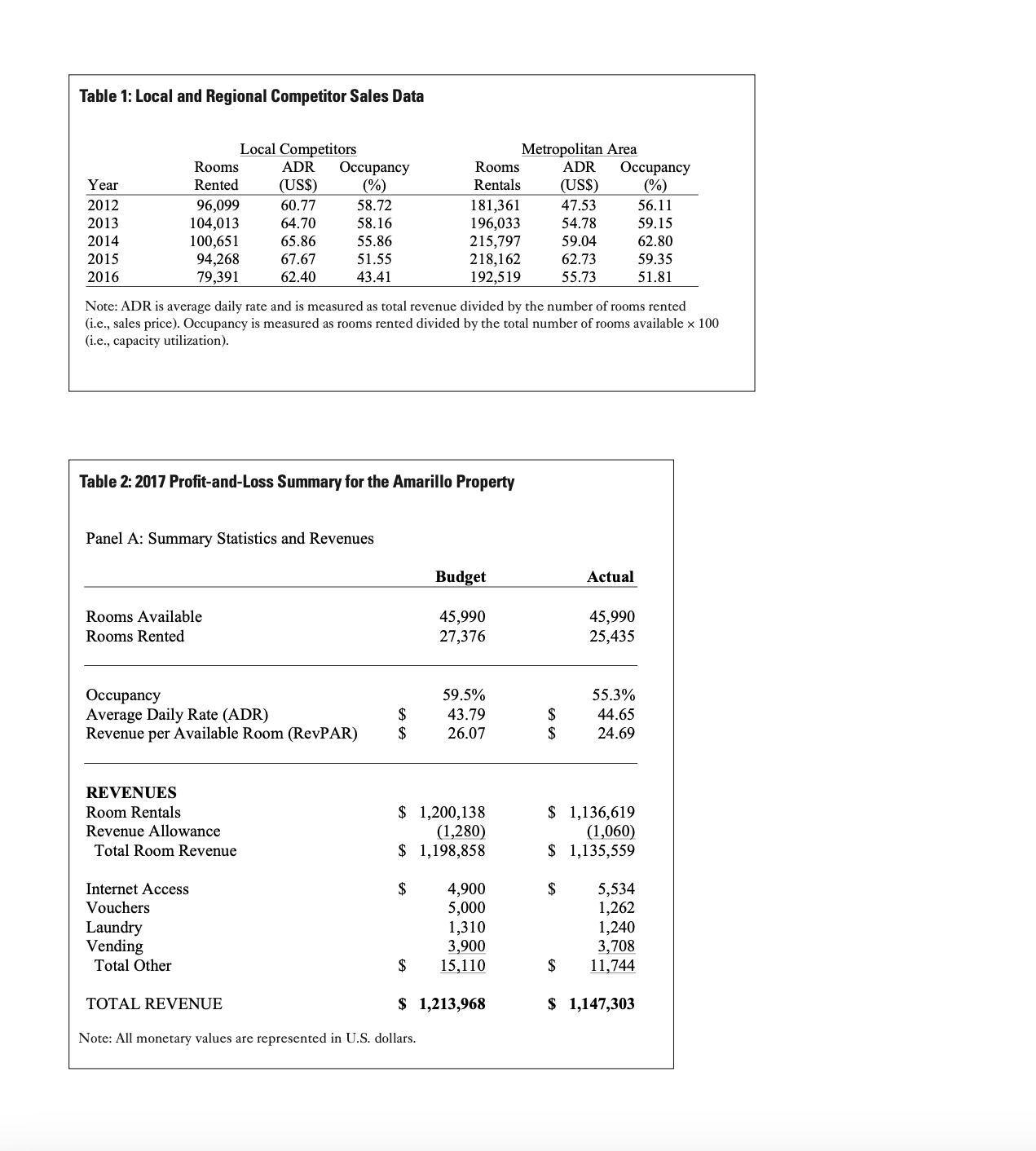

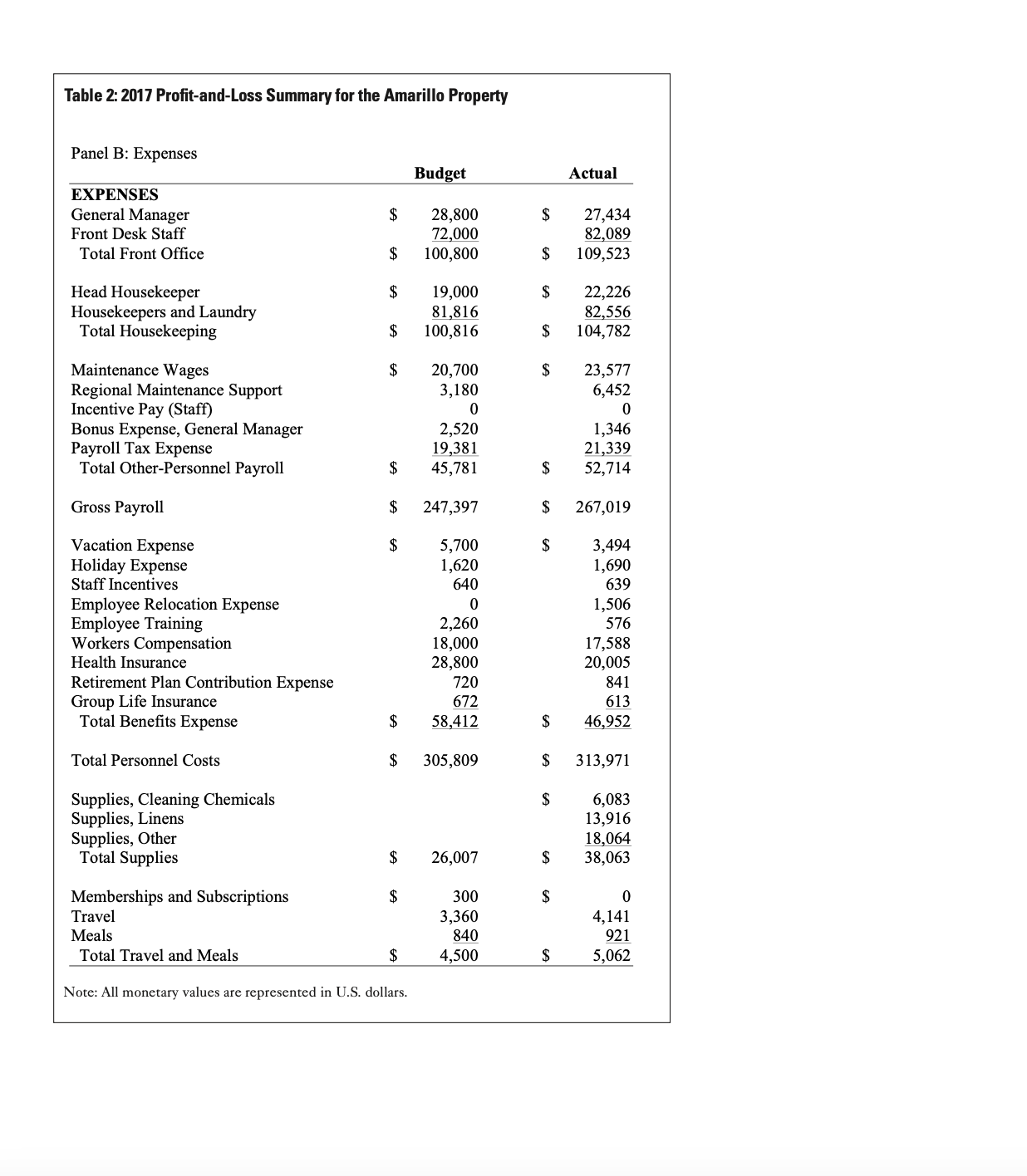

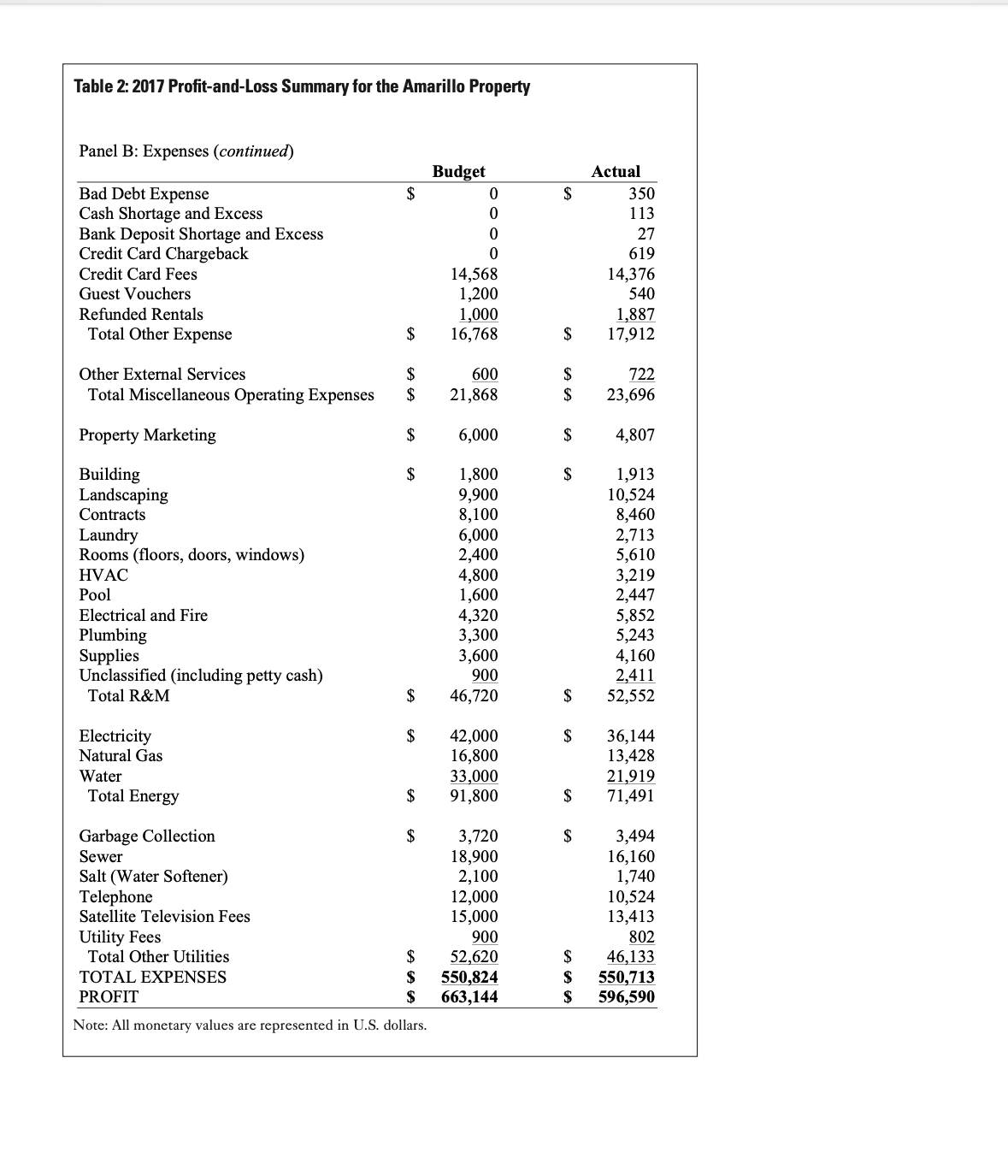

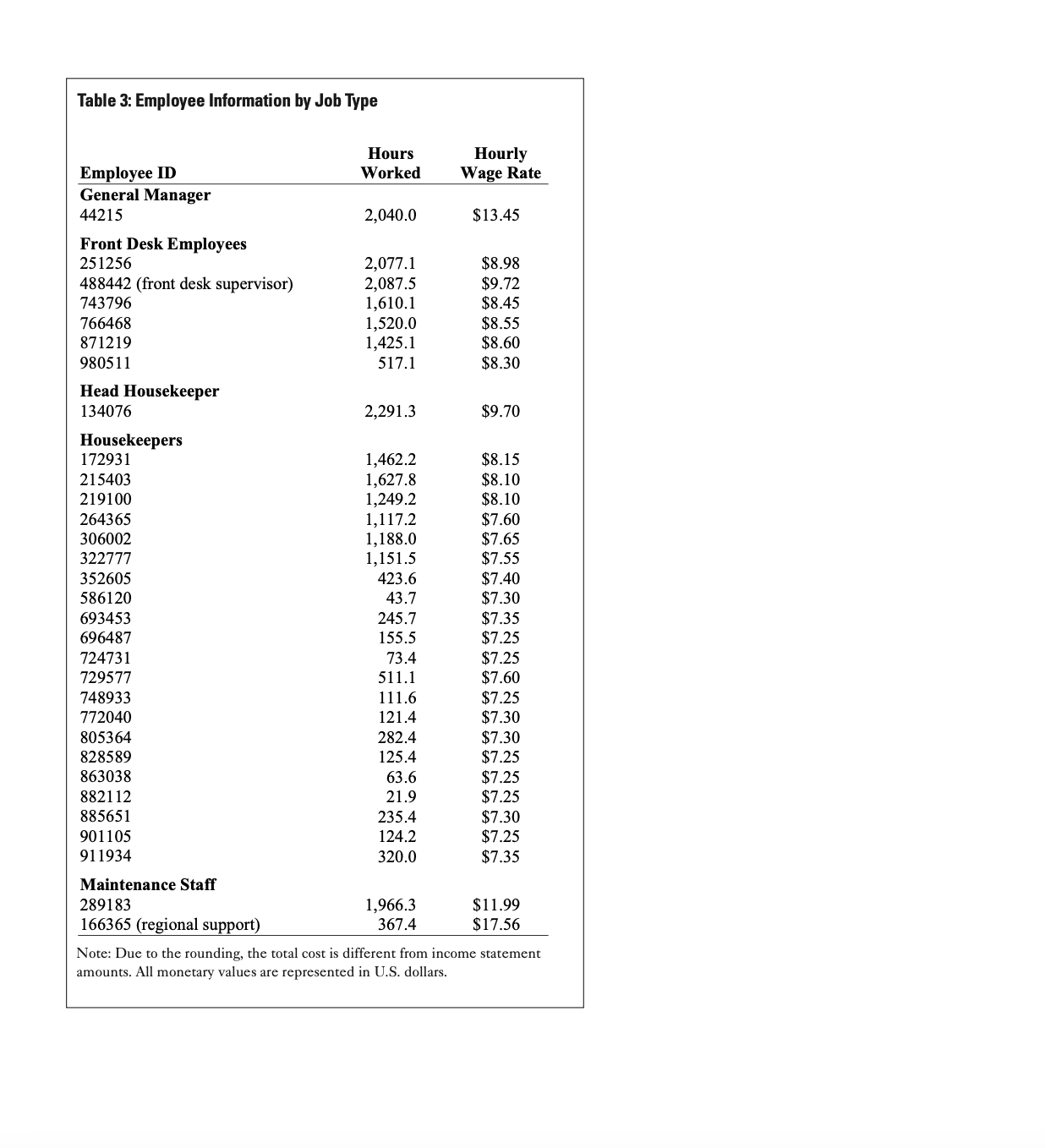

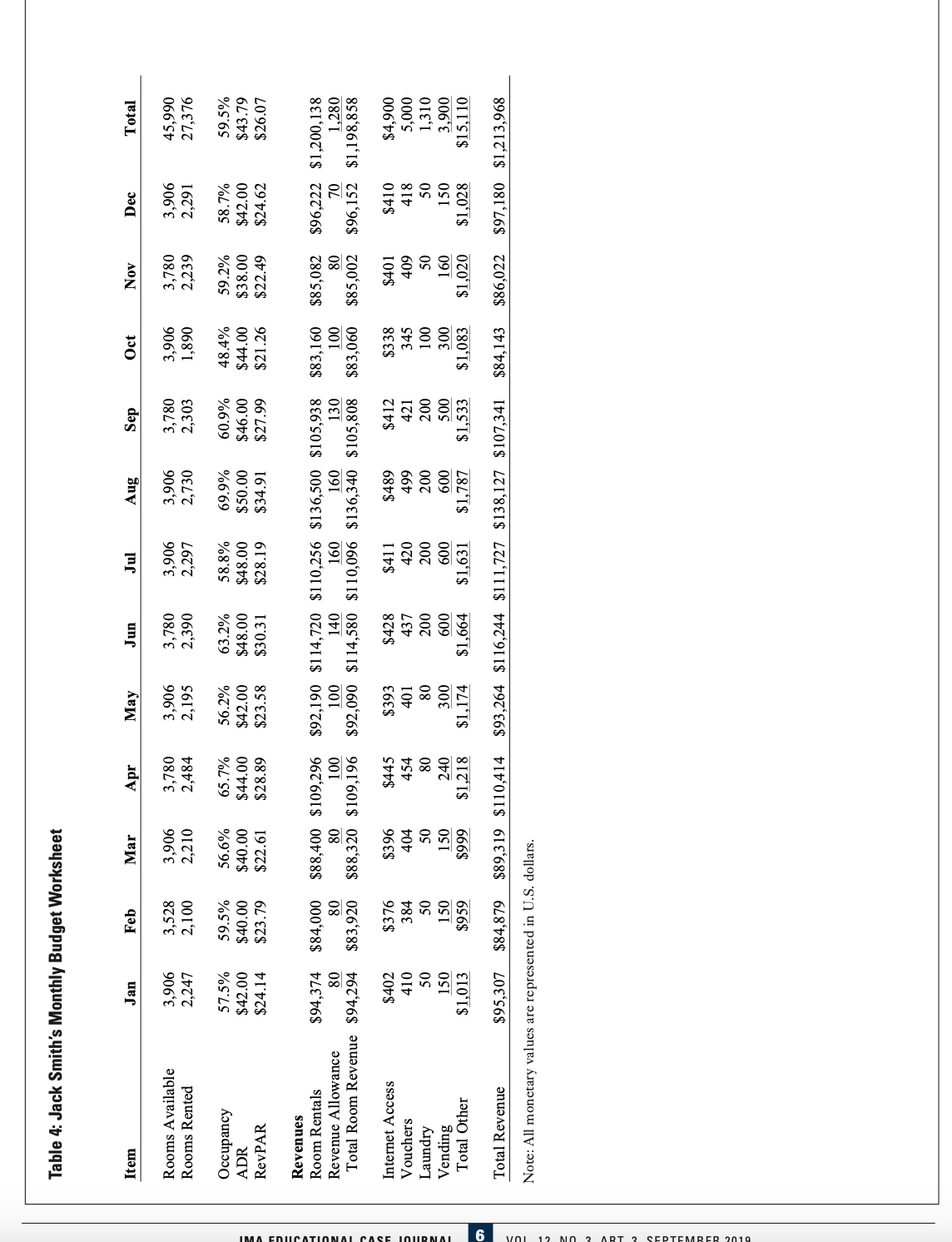

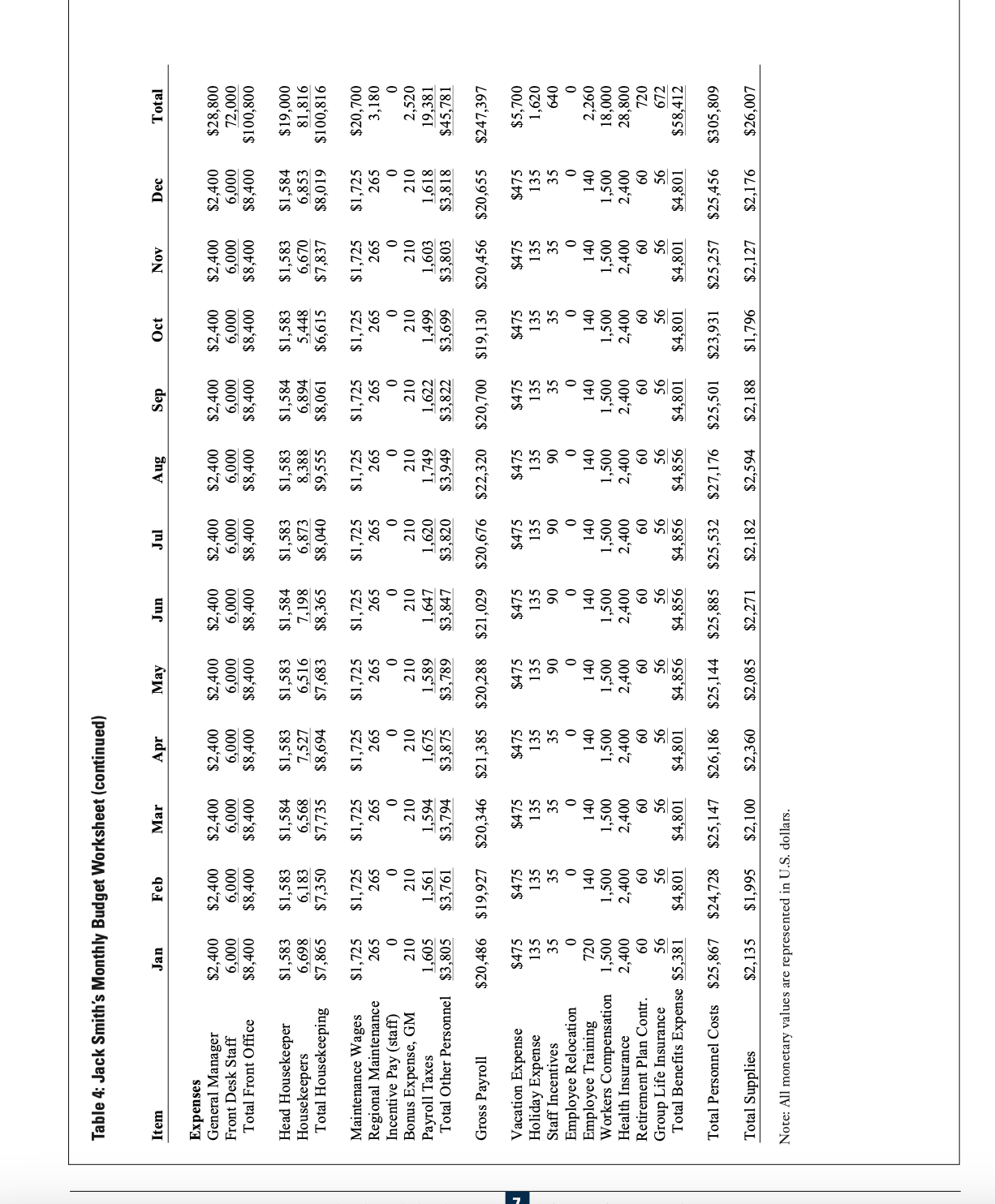

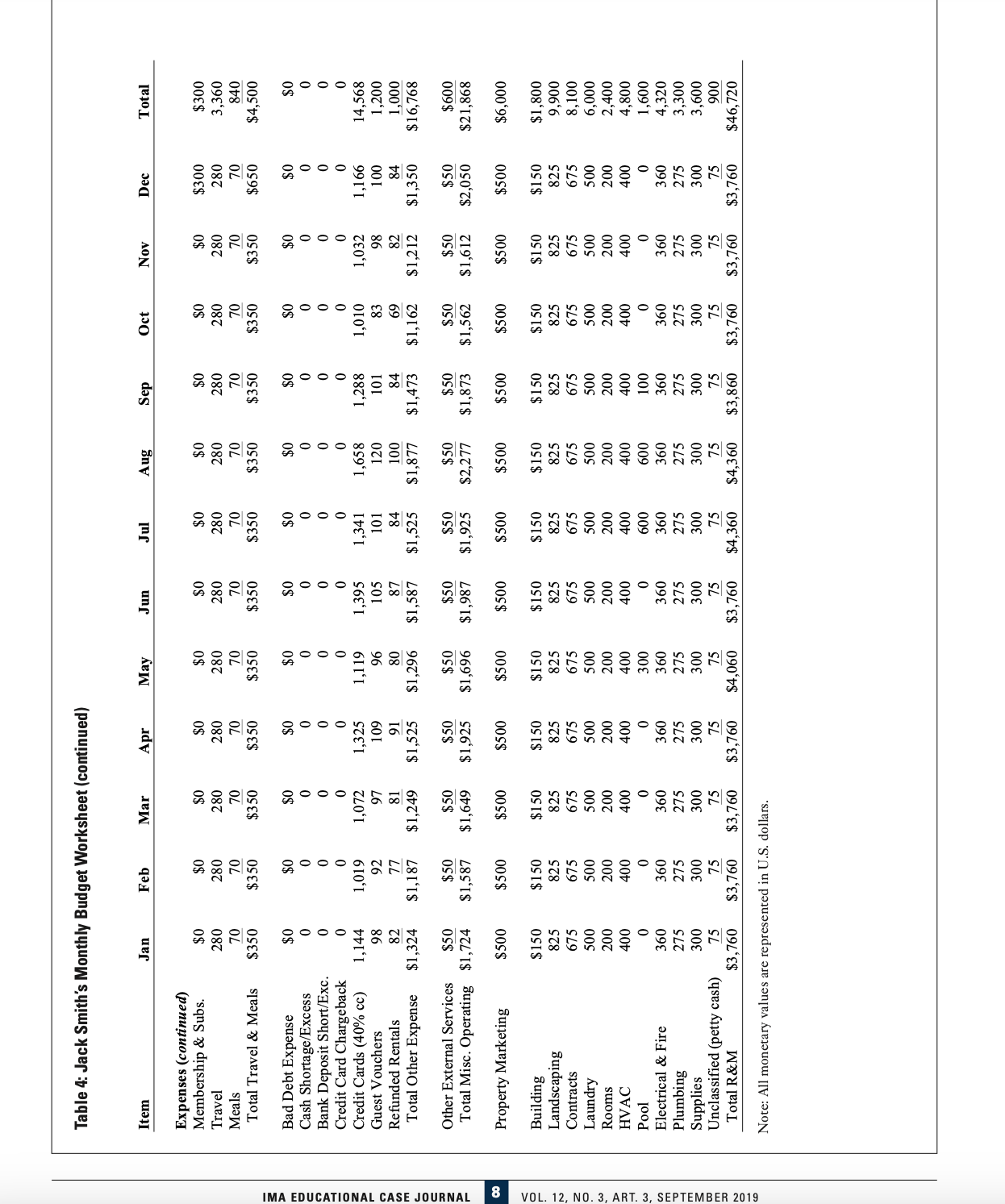

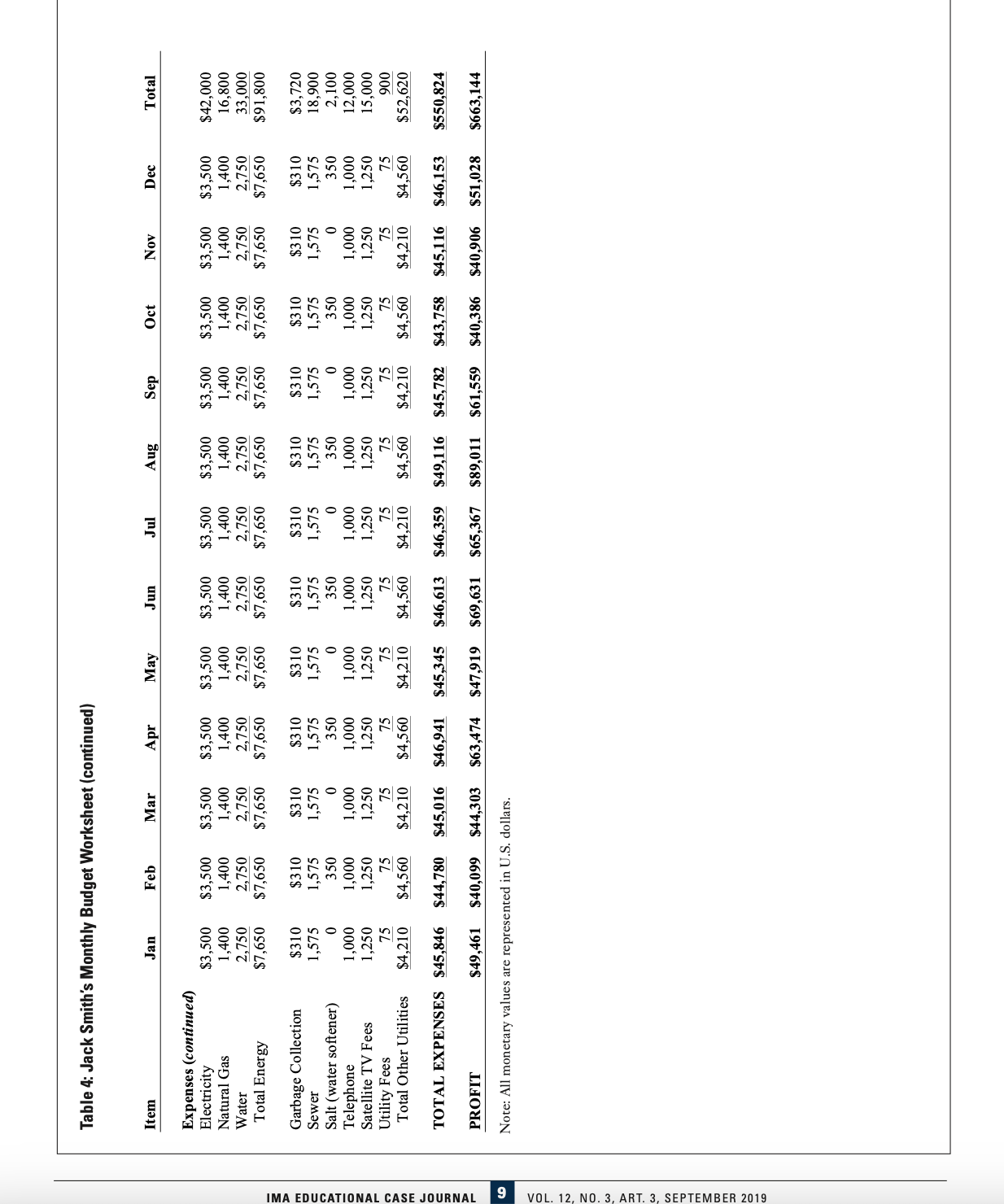

IMA EDUCATIONAL Case Case Journal Study Lone Star Lodging Thomas Calderon University of Akron INTRODUCTION James W. Hesford* University of Lethbridge Dhillon School of Business Sitting at his desk reviewing the results of the last year, Jack Smith reflected on his second year as General Manager of the Lone Star Motel. Next week is the Regional Operations Review in nearby Lubbock, Texas, where managers from surrounding areas will gather with Victoria Jennings, Regional Vice President of Operations. Smith will need to summarize the hotel's performance and, recalling variance analysis, thought this tool would be a rigorous way to conduct his analysis. COMPANY BACKGROUND The Lone Star Motel is a 126-room economy-lodging hotel in Amarillo, Texas. Built in 1980, it is part of Lone Star Lodging, a privately-owned hotel chain headquartered in suburban Houston, Texas. Lone Star Lodging operates a network of 207 hotels in four states: Texas, New Mexico, Oklahoma and Arkansas. About half of the hotels are owned and operated by the company. PRESENT SITUATION Renovated two years ago, the hotel competes with 16 other economy-lodging hotels in a market that is more competitive than most. However, when thinking about its market share, company management actually considers three nearby hotels to be the hotel's direct competitors. Sales data on regional and local competitors for the past five years are regularly obtained from an industry benchmarking firm (see Table 1). In the hospitality industry, average sales price is average daily rate (ADR), defined as the total room revenue divided by the number of rooms rented. Another industry-standard metric, occupancy, represents capacity utilization. Occupancy is defined IMA EDUCATIONAL CASE JOURNAL ima Mina Pizzini McCoy College of Business Texas State University 1 The Association of Accountants and Financial Professionals in Business ISSN 1940-204X Michael J. Turner The University of Queensland UQ Business School as the total number of rooms rented (output) divided by the number of rooms available during the period (capacity). In preparing his budget, Smith expected the 2017 market size to be 10% higher than the 2016 market size. For 2017, the benchmarking firm reported that local competitors rented 77,291 rooms at an ADR of $59.80. VOL. 12, NO. 3, ART. 3, SEPTEMBER 2019 Smith turned to the report detailing budgeted and actual revenue and expense data (see Table 2). Accounting provided Smith with the hours worked by hotel staff. The maintenance worker and general manager are normally full-time workers (that is, 40 hours per week, 50 weeks a year). All other workers are considered full time, though many of them work less than 40 hours per week (see Table 3). In preparing the budget, Smith planned on housekeeping staff using a standard time of 30 minutes per room with a wage rate of $7.00 per hour. The head housekeeper's wage was budgeted at $9.50 per hour and usually works 40 hours. With a small staff, the head housekeeper also cleans rooms. Her productivity appears lower (that is, cleans fewer rooms) because of her supervisory duties (inspections and employee training) and the need to complete the room inventory form. Accordingly, during slow periods, the head housekeeper may work fewer hours. Smith anticipated having one person staffing the front desk at all hours. With the exception of the general manager, employees do not get paid vacation time. Further, with high turnover, most employees do not receive benefits (healthcare and retirement contributions). Table 4 shows the monthly budget Smith developed to submit to corporate accounting as his required annual budget. A description of accounts is given in the Appendix. Next week is Smith's operations review meeting with Victoria Jennings. Having gathered all the data needed for a comprehensive variance analysis, he would like your help doing the calculations, interpreting the numbers, and preparing his report and presentation. 2019 IMA APPENDIX. ACCOUNT DESCRIPTIONS REVENUE ACCOUNTS Room Rentals. Revenue derived from room rentals. It is the average daily rate times rentals. Revenue Allowance. Revenue allowances are refunds offered at the property at time of departure. Internet Access. Revenue derived from the sale of daily guest Wi-Fi/Internet access. Vouchers. Revenue from guests paying for their stay with guest vouchers. Laundry. Revenue from customer use of coin-operated laundry equipment (washer and dryer). Vending. Revenue received from customer purchases at on- site vending machines. EXPENSE ACCOUNTS General Manager. Wages paid to the general manager. Managers receive free, on-site housing and utilities (electric, telephone, cable TV). Front Desk Staff. Wages paid to employees working the front desk for customer check-in. Total Housekeeping. Wages paid to employees that clean the rooms and clean laundry. Maintenance Wages. Wages paid to an on-site maintenance worker. Regional Maintenance Support. Wages for the regional maintenance person when on-site. Incentive Pay (Staff). Amounts paid to motivate employees. This is usually zero. Bonus Expense, General Manager. Bonus expense paid to the general manager when specific performance targets are met. Bonus amounts are fixed for each goal, and 90% of general managers receive their full bonus (bonuses are highly achievable). Payroll Tax Expense. Amounts paid for payroll taxes. It is 8.5% of amounts paid to employees. Vacation Expense. Amounts accrued to pay for the general manager's vacation. Holiday Expense. Amounts accrued to pay for the general manager's paid holidays. Staff Incentives. Amounts paid for anything that incentives hotel staff. For example, many general managers provide pizza parties on employee birthdays, or lunch on busy days. Employee Relocation Expense. Amounts paid to reimburse employees who relocate to a new property. This amount is usually zero, and the company only pays to relocate a general manager (a rare event). Employee Training. Amounts paid for employee training. Training is provided for general managers and managers-in- training. Workers Compensation. The amounts charged to workers' compensation are based on expected insurance claim plus any expenses that develop over time. Amounts are actuarial estimates and, while budgeted by the general manager, the manager does not determine the amounts. Health Insurance. Amounts paid for employee group health insurance. Since benefits are provided after 6 months of service, most staff do not participate in the insurance plan. (This is because employee turnover in low-skill, hospitality jobs is very high; at the Amarillo property, turnover for housekeeping staff was 211% in the prior year.) Retirement Plan Contribution Expense. Amounts paid by the company for employee retirement contributions. As with health insurance, few employees are with the hotel long enough to participate in the plan, and contributions are often solely for the general manager (where job tenure averages about 2.8 years). Group Life Insurance. Expenses related to the provision of group life insurance. As with the prior two benefits plans, group life insurance is typically only provided to the general manager. Supplies. Expenses for all supplies. In prior years, supplies were listed in one category, but after the 2017 budget was prepared, the company developed several sub-accounts for supplies. Supplies at most hotels include guest amenities (soap, shampoo and hand cream), cleaning chemicals (carpet and floor cleaners and surface cleaners), postage, uniforms, freight, coffee and linens. Memberships and Subscriptions. Amounts paid for memberships (such as for the local chamber of commerce). Travel. Amounts paid to reimburse employees who travel for company business. Most of the time the only reimbursement is for personal use of the car to make the daily cash deposit at the bank (mileage multiplied by the IRS-approved mileage reimbursement rate). Off-site travel is rare as regional managers visit properties for performance reviews and support. Meals. Reimbursement for meal expenses. Expenses are typically incurred when a general manager is out of town for a meeting (such as the national or a regional meeting) or doing part-time duty as a relief general manager (from time to time a manager may be terminated and it may take some weeks or months to find a replacement). Meal expenses are relatively rare. Bad Debt Expense. Amounts recorded to this account reflect credit transactions that have been "written off." Since most transactions are handled in cash or with a credit card, bad debt expense is uncommon. Cash Shortage and Excess. These amounts arise when the actual cash on hand differs from the amount that should be on hand, according to the property's financial records. Since there are multiple employees handling cash, the amounts are not easily traced to a specific person. Discrepancies can occur from providing the incorrect change for a cash transaction, receiving an amount less than billed, and so on. Bank Deposit Shortage and Excess. These amounts arise when the bank deposit does not match the amount that was supposed to have been deposited. When a discrepancy occurs, the bank's amount is taken as the correct amount because of counting machines and good video surveillance at banks. If the general manager makes random, counting mistakes, these discrepancies should be small and should average out to zero. A persistent shortage is a strong signal that cash is being misappropriated. The general manager is the only person to make the daily bank deposit, so any shortage or excess is the responsibility of one person. Credit Card Chargeback. Amounts refunded to credit card companies. These occur because of fraudulent credit card use and customer complaints (i.e., the firm grants a refund several days after the visit). Credit Card Fees. Amounts paid to credit card companies for processing credit cards. Typically, this averages about 3% of the transaction cost. At most properties, more than 70% of transactions are settled in cash. Guest Vouchers. Guests who received a voucher for compensation are able to use that voucher for a free night's stay at any branded hotel in the network. The hotel who hosts a guest with a voucher records the revenue, the property that issued the guest voucher is charged for the guest visit, and its expense is recorded to this account. Refunded Rentals. These amounts are for customer refunds that occur off-property, often weeks after a guest's visit. Almost always, these refunds are handled by the customer service staff at the corporate headquarters. Functionally, it is no different in financial impact than a revenue allowance. 11 Other External Services. Amounts paid to any third-party providers that are not related to maintenance. Security services is the most common expense related to this account. Property Marketing. Amounts spent by the general manager for local advertising and marketing. Marketing activities include newspaper advertising, coupon booklets, billboards, direct mail, sponsoring a community athletic club, and so on. Building. Repairs and maintenance expenses related to the building. Landscaping. Amounts paid for lawn care, new shrubbery, tree trimming, and so on. Contracts. Amounts paid to third parties that provide services to the hotel. This would include, for example, service contracts for the laundry equipment and pest control (e.g., termites, bed bugs and rodents). Laundry. Repairs and maintenance expenses related to the laundry equipment (washer, dryer, folder). Rooms (floors, doors, windows, et cetera). All expenses related to the repair and maintenance of the guest rooms (carpets, walls, windows and light fixtures, except those items accounted for elsewhere [such as plumbing and climate control equipment]). HVAC. Repair and maintenance expenses related to heating, ventilation and air conditioning units. In most properties, including the case property, HVAC is handled by in-wall, all-in-one units. Pool. All amounts paid for maintaining the swimming pool. This would include paint, chemicals, pump repairs, diving board repairs, upkeep of the surface and fences surrounding the pool, and so on. Electrical and Fire. All costs related to the repair and maintenance of electrical and fire safety equipment. Plumbing. All expenses related to repairs and maintenance of plumbing and related fixtures (e.g., showers, bathtubs and toilets). Supplies. Amounts paid for supplies related to repairs and maintenance (e.g., duct tape, silicone and nails). Unclassified (including petty cash). This category is for all expenses related to repairs and maintenance that are not classified in any of the other accounts for repairs and maintenance. Electricity. Amounts paid for electricity. Electricity is used in guest rooms (outlets, lighting, air conditioner, etc.), in the lobby, for exterior lighting (parking lot, corridors), and in the laundry room. Natural Gas. Amounts paid for natural gas. Natural gas is used for the boiler (water) and dryer (laundry). Rooms are heated using electricity. Water. Amounts paid for water. Water is used in guest rooms, the washing machine, the pool, and for watering the lawn. Garbage Collection. Garbage is picked up twice a week by a licensed waste hauler from waste containers located at a corner of the property. Garbage is usually limited to a handful of providers, some of which are national firms. Sewer. Amounts paid to the city for hook-up to the city sewer system. Salt (Water Softener). Amounts paid for salt used in a water softener. Telephone. All costs related to telephone equipment repairs and monthly telecommunications fees. Satellite Television Subscription Fees. Expenses for subscription of television programming delivered by a satellite provider. Utility Fees. Amounts paid to utilities firms for connection and service fees. IMA EDUCATIONAL CASE JOURNAL 12 ABOUT IMA (INSTITUTE OF MANAGEMENT ACCOUNTANTS) IMA, the association of accountants and financial professionals in business, is one of the largest and most respected associations focused exclusively on advancing the management accounting profession. Globally, IMA supports the profession through research, the CMA (Certified Management Accountant) program, continuing education, networking and advocacy of the highest ethical business practices. IMA has a global network of more than 100,000 members in 140 countries and 300 professional and student chapters. Headquartered in Montvale, N.J., USA, IMA provides localized services through its four global regions: The Americas, Asia/Pacific, Europe, and Middle East/India. For more information about IMA, please visit www.imanet.org. VOL. 12, NO. 3, ART. 3, SEPTEMBER 2019 Table 1: Local and Regional Competitor Sales Data Year 2012 2013 2014 2015 2016 Rooms Rented 96,099 104,013 100,651 94,268 79,391 Rooms Available Rooms Rented Internet Access Vouchers Laundry Vending Local Competitors Panel A: Summary Statistics and Revenues Total Other REVENUES Room Rentals Revenue Allowance Total Room Revenue ADR Occupancy (%) (US$) 60.77 58.72 64.70 58.16 65.86 55.86 67.67 51.55 62.40 43.41 Table 2: 2017 Profit-and-Loss Summary for the Amarillo Property Occupancy Average Daily Rate (ADR) Revenue per Available Room (RevPAR) TOTAL REVENUE Note: ADR is average daily rate and is measured as total revenue divided by the number of rooms rented (i.e., sales price). Occupancy is measured as rooms rented divided by the total number of rooms available x 100 (i.e., capacity utilization). $ $ Rooms Rentals 181,361 196,033 $ 215,797 218,162 192,519 Note: All monetary values are represented in U.S. dollars. Budget 45,990 27,376 $ 1,200,138 (1,280) $ 1,198,858 Metropolitan Area 59.5% 43.79 26.07 $ 4,900 5,000 1,310 3,900 15,110 $ 1,213,968 ADR Occupancy (US$) (%) 56.11 59.15 62.80 59.35 51.81 47.53 54.78 59.04 62.73 55.73 Actual 45,990 25,435 55.3% 44.65 24.69 $ 1,136,619 (1,060) $ 1,135,559 $ 5,534 1,262 1,240 3,708 $ 11,744 $ 1,147,303 Table 2: 2017 Profit-and-Loss Summary for the Amarillo Property Panel B: Expenses EXPENSES General Manager Front Desk Staff Total Front Office Head Housekeeper Housekeepers and Laundry Total Housekeeping Maintenance Wages Regional Maintenance Support Incentive Pay (Staff) Bonus Expense, General Manager Payroll Tax Expense Total Other-Personnel Payroll Gross Payroll Vacation Expense Holiday Expense Staff Incentives Employee Relocation Expense Employee Training Workers Compensation Health Insurance Retirement Plan Contribution Expense Group Life Insurance Total Benefits Expense Total Personnel Costs Supplies, Cleaning Chemicals Supplies, Linens Supplies, Other Total Supplies Memberships and Subscriptions Travel Meals Total Travel and Meals $ $ $ $ $ $ 20,700 3,180 0 2,520 19,381 45,781 $ 247,397 $ $ $ Budget $ 28,800 72,000 100,800 Note: All monetary values are represented in U.S. dollars. 19,000 81,816 100,816 720 672 $ 58,412 $ 305,809 5,700 1,620 640 0 2,260 18,000 28,800 26,007 300 3,360 840 4,500 $ $ S $ $ $ $ $ Actual $ 267,019 $ S 27,434 82,089 109,523 $ 22,226 82,556 104,782 23,577 6,452 0 1,346 21,339 52,714 841 613 $ 46,952 $ 313,971 3,494 1,690 639 1,506 576 17,588 20,005 6,083 13,916 18,064 38,063 0 4,141 921 5,062 Table 2: 2017 Profit-and-Loss Summary for the Amarillo Property Panel B: Expenses (continued) Bad Debt Expense Cash Shortage and Excess Bank Deposit Shortage and Excess Credit Card Chargeback Credit Card Fees Guest Vouchers Refunded Rentals Total Other Expense Other External Services Total Miscellaneous Operating Expenses Property Marketing Building Landscaping Contracts Laundry Rooms (floors, doors, windows) HVAC Pool Electrical and Fire Plumbing Supplies Unclassified (including petty cash) Total R&M Electricity Natural Gas Water Total Energy Garbage Collection Sewer Salt (Water Softener) Telephone Satellite Television Fees Utility Fees Total Other Utilities TOTAL EXPENSES PROFIT $ $ $ $ $ $ $ $ $ $ $ $ $ Note: All monetary values are represented in U.S. dollars. Budget 0 0 0 0 14,568 1,200 1,000 16,768 600 21,868 6,000 1,800 9,900 8,100 6,000 2,400 4,800 1,600 4,320 3,300 3,600 900 46,720 42,000 16,800 33,000 91,800 3,720 18,900 2,100 12,000 15,000 900 52,620 550,824 663,144 $ $ $ $ $ $ $ $ $ $ Actual 350 113 27 619 14,376 540 1,887 17,912 722 23,696 4,807 1,913 10,524 8,460 2,713 5,610 3,219 2,447 5,852 5,243 4,160 2,411 52,552 36,144 13,428 21,919 71,491 3,494 16,160 1,740 10,524 13,413 802 $ 46,133 $ 550,713 $ 596,590 Table 3: Employee Information by Job Type Employee ID General Manager 44215 Front Desk Employees 251256 488442 (front desk supervisor) 743796 766468 871219 980511 Head Housekeeper 134076 Housekeepers 172931 215403 219100 264365 306002 322777 352605 586120 693453 696487 724731 729577 748933 772040 805364 828589 863038 882112 885651 901105 911934 Maintenance Staff 289183 166365 (regional support) Hours Worked 2,040.0 2,077.1 2,087.5 1,610.1 1,520.0 1,425.1 517.1 2,291.3 1,462.2 1,627.8 1,249.2 1,117.2 1,188.0 1,151.5 423.6 43.7 245.7 155.5 73.4 511.1 111.6 121.4 282.4 125.4 63.6 21.9 235.4 124.2 320.0 1,966.3 367.4 Hourly Wage Rate $13.45 $8.98 $9.72 $8.45 $8.55 $8.60 $8.30 $9.70 $8.15 $8.10 $8.10 $7.60 $7.65 $7.55 $7.40 $7.30 $7.35 $7.25 $7.25 $7.60 $7.25 $7.30 $7.30 $7.25 $7.25 $7.25 $7.30 $7.25 $7.35 $11.99 $17.56 Note: Due to the rounding, the total cost is different from income statement amounts. All monetary values are represented in U.S. dollars. IMA EDUCATIONAL CASE JOURNAL You 12 NO 3 ART 3 SEPTEMBER 2019 Table 4: Jack Smith's Monthly Budget Worksheet Item Rooms Available Rooms Rented Occupancy ADR RevPAR Internet Access Vouchers Laundry Vending Total Other Jan Revenues Room Rentals $94,374 80 Revenue Allowance Total Room Revenue $94,294 3,906 2,247 Total Revenue 57.5% $42.00 $24.14 $402 410 50 150 $1,013 Feb 3,528 2,100 59.5% $40.00 $23.79 $84,000 80 $83,920 $376 384 50 150 $959 Mar 3,906 2,210 Apr 3,780 2,484 56.6% 65.7% $40.00 $44.00 $22.61 $28.89 $88,400 $109,296 80 100 $88,320 $109,196 $396 404 50 150 $999 $445 454 80 240 $1,218 May 3,906 2,195 Jun 3,780 2,390 Aug 3,906 3,906 2,297 2,730 Jul 56.2% 63.2% $42.00 $48.00 $48.00 $23.58 $30.31 $28.19 Sep 3,780 2,303 $411 $489 420 200 600 Oct 3,906 1,890 $393 $428 $412 401 437 499 421 80 200 200 200 300 600 600 500 $1,174 $1,664 $1,631 $1,787 $1,533 Nov 58.7% 58.8% 69.9% 60.9% 48.4% 59.2% $50.00 $46.00 $44.00 $38.00 $42.00 $34.91 $27.99 $21.26 $22.49 $24.62 3,780 2,239 $338 345 100 300 $1,083 Dec 3,906 2,291 $401 409 50 160 $1,020 $92,190 $114,720 $110,256 $136,500 $105,938 $83,160 $85,082 $96,222 $1,200,138 70 100 140 160 160 130 $92,090 $114,580 $110,096 $136,340 $105,808 100 $83,060 80 $85,002 $96,152 Total $410 418 50 150 $1,028 45,990 27,376 59.5% $43.79 $26.07 1,280 $1,198,858 $4,900 5,000 1,310 3,900 $15,110 $95,307 $84,879 $89,319 $110,414 $93,264 $116,244 $111,727 $138,127 $107,341 $84,143 $86,022 $97,180 $1,213,968 Note: All monetary values are represented in U.S. dollars. Table 4: Jack Smith's Monthly Budget Worksheet (continued) Item Expenses General Manager Front Desk Staff Total Front Office Maintenance Wages Regional Maintenance Jan Incentive Pay (staff) Bonus Expense, GM Payroll Taxes Total Other Personnel Gross Payroll Vacation Expense Holiday Expense Staff Incentives $2,400 6,000 $8,400 Head Housekeeper Housekeepers Total Housekeeping $7,865 $1,725 265 0 $1,583 6,698 6,183 $7,350 210 1,605 $3,805 $20,486 $475 135 35 0 Feb Employee Relocation Employee Training 720 Workers Compensation 1,500 Health Insurance 2,400 Retirement Plan Contr. 60 56 $2,400 $2,400 6,000 6,000 $8,400 $8,400 $1,583 $1,584 6,568 $7,735 Mar $1,725 265 0 210 1,561 $3,761 $19,927 $475 135 35 0 140 1,500 2,400 60 56 $4,801 $24,728 $1,725 265 0 210 1,594 $3,794 $20,346 $475 135 35 0 140 1,500 2,400 60 56 $4,801 $25,147 Group Life Insurance Total Benefits Expense $5,381 Total Personnel Costs $25,867 Total Supplies $2,135 $1,995 $2,100 Note: All monetary values are represented in U.S. dollars. Apr $2,400 6,000 $8,400 $1,583 7,527 $8,694 $475 135 35 0 140 1,500 2,400 May 60 56 $4,801 $26,186 $2,400 $2,400 6,000 $8,400 6,000 $8,400 $1,725 265 0 210 1,675 1,647 $3,875 $3,847 $21,385 $20,288 $21,029 $1,583 $1,584 6,516 7,198 $7,683 $8,365 $1,725 265 0 210 1,589 $3,789 Jun $475 135 90 0 140 1,500 2,400 60 56 $4,856 $25,144 $1,725 265 0 210 $475 135 90 0 140 1,500 2,400 Jul $1,583 6,873 $8,040 $2,400 $2,400 $2,400 6,000 6,000 6,000 $8,400 $8,400 $8,400 Aug 140 1,500 2,400 60 56 $4,856 $25,885 $2,360 $2,085 $2,271 $2,182 $1,583 8,388 $9,555 Sep $2,594 Oct $1,584 $1,583 6,894 5,448 $8,061 $6,615 $1,725 265 $2,400 $2,400 6,000 6,000 $8,400 $8,400 Nov $475 135 35 0 140 1,500 2,400 $1,583 6,670 $7,837 $1,725 $1,725 $1,725 $1,725 $1,725 $20,700 3,180 265 265 265 265 265 0 0 0 0 0 0 0 210 210 210 210 210 210 2,520 1,620 1,749 1,622 1,499 1,603 1,618 19,381 $3,820 $3,949 $3,822 $3,699 $3,803 $3,818 $45,781 $20,676 $22,320 $20,700 $19,130 $20,456 $20,655 $247,397 $475 $475 $475 $475 $5,700 135 135 135 135 1,620 90 90 35 35 640 0 0 0 0 0 140 140 1,500 1,500 2,400 2,400 Dec 140 1,500 2,400 $2,400 6,000 $8,400 $1,584 6,853 $8,019 $475 135 35 0 Total 140 1,500 2,400 $28,800 72,000 $100,800 $19,000 81,816 $100,816 60 60 60 60 60 60 720 56 56 56 56 56 56 672 $4,856 $4,856 $4,801 $4,801 $4,801 $4,801 $58,412 $25,532 $27,176 $25,501 $23,931 $25,257 $25,456 $305,809 $2,188 $1,796 $2,127 $2,176 $26,007 2,260 18,000 28,800 IMA EDUCATIONAL CASE JOURNAL 8 VOL. 12. NO. 3. ART. 3. SEPTEMBER 2019 Table 4: Jack Smith's Monthly Budget Worksheet (continued) Item Expenses (continued) Membership & Subs. Travel Meals Total Travel & Meals Bad Debt Expense Cash Shortage/Excess Bank Deposit Short/Exc. Credit Card Chargeback Credit Cards (40% cc) Guest Vouchers Refunded Rentals Total Other Expense Jan $0 280 70 $350 $0 0 0 0 1,144 98 82 $1,324 Feb **** ***** & 29088330873 Other External Services $50 Total Misc. Operating $1,724 $1,587 Property Marketing $500 $150 825 675 500 Building Landscaping Contracts Laundry Rooms HVAC Pool Electrical & Fire 200 400 0 360 275 Plumbing Supplies 300 Unclassified (petty cash) 75 Total R&M $3,760 $3,760 Mar Apr $0 280 70 $350 $0 0 0 0 1,072 97 81 $1,249 $500 $150 825 675 500 200 400 $50 $50 $1,649 $1,925 0 360 275 $0 280 70 $350 $0 0 0 0 Note: All monetary values are represented in U.S. dollars. 1,325 109 91 $1,525 $500 $150 825 675 500 200 400 0 360 275 300 75 300 75 $3,760 $3,760 May $0 280 70 $350 $0 0 0 0 1,119 96 80 $1,296 $50 $1,696 $500 $150 825 675 500 200 400 300 360 275 300 75 $4,060 Jun $0 280 70 $350 $0 0 0 0 $50 $1,987 $500 Jul 1,395 105 87 $1,587 $1,525 $150 825 675 500 200 400 $0 280 70 $350 $0 0 0 0 1,341 101 84 $50 $1,925 $500 $150 825 675 500 200 400 0 600 360 360 275 275 300 300 75 75 $3,760 $4,360 Aug $0 280 70 $350 $0 0 0 0 $50 $2,277 $500 $150 825 675 500 200 400 Sep 1,658 120 100 $1,877 $1,473 600 360 275 300 75 $4,360 $0 280 70 $350 $0 0 0 0 1,288 101 84 $50 $1,873 $500 $150 825 675 Oct $0 280 70 $350 $0 0 0 0 1,010 83 69 $1,162 $50 $1,562 $500 $150 825 675 500 200 400 500 200 400 100 0 360 360 275 275 300 300 75 75 $3,860 $3,760 Nov $0 280 70 $350 $0 0 0 0 1,032 98 82 $1,212 $50 $1,612 $500 $150 825 675 500 200 400 0 360 275 300 75 $3,760 Dec $300 280 70 $650 $0 0 0 0 1,166 100 84 $1,350 $50 $2,050 $500 $150 825 675 500 200 400 0 360 275 300 75 $3,760 Total $300 3,360 840 $4,500 $0 0 0 0 14,568 1,200 1,000 $16,768 $600 $21,868 $6,000 $1,800 9,900 8,100 6,000 2,400 4,800 1,600 4,320 3,300 3,600 900 $46,720 IMA EDUCATIONAL CASE JOURNAL VOL. 12, NO. 3, ART. 3, SEPTEMBER 2019 Table 4: Jack Smith's Monthly Budget Worksheet (continued) Item Expenses (continued) Electricity Natural Gas Water Total Energy Garbage Collection Sewer Salt (water softener) Telephone Satellite TV Fees Utility Fees Total Other Utilities Jan PROFIT $3,500 1,400 $3,500 1,400 2,750 2,750 $7,650 $310 1,575 0 1,000 1,250 75 $4,210 TOTAL EXPENSES $45,846 Feb Mar Apr $3,500 $3,500 $3,500 1,400 1,400 1,400 2,750 2,750 2,750 $7,650 $7,650 $7,650 $49,461 $40,099 $44,303 Note: All monetary values are represented in U.S. dollars. May Jun $3,500 1,400 2,750 $7,650 $7,650 $310 1,575 0 1,000 1,250 75 $4,210 $310 1,575 350 $310 $310 $310 1,575 1,575 1,575 350 0 350 1,000 1,000 1,000 1,000 1,250 1,250 1,000 1,250 1,250 1,250 75 75 75 $4,560 $4,210 $4,560 75 75 $4,560 $4,210 $44,780 $45,016 $46,941 $45,345 $46,613 $46,359 $63,474 $47,919 $69,631 Jul Aug Sep Oct $3,500 $3,500 $3,500 $3,500 $3,500 $3,500 1,400 1,400 1,400 1,400 1,400 1,400 2,750 2,750 2,750 2,750 2,750 2,750 $7,650 $7,650 $7,650 $7,650 $7,650 $7,650 $310 1,575 0 1,000 1,250 75 $4,210 Nov $310 $310 $310 $3,720 $310 1,575 1,575 1,575 1,575 18,900 0 350 0 350 2,100 1,000 1,000 1,000 12,000 1,250 15,000 900 75 1,250 1,250 75 75 $4,210 $4,560 $4,560 $52,620 $49,116 $45,782 $43,758 $45,116 $46,153 $550,824 $65,367 $89,011 $61,559 $40,386 $40,906 $51,028 $663,144 $310 1,575 350 Dec 1,000 1,250 75 $4,560 Total $42,000 16,800 33,000 $91,800

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance for Non Financial Managers

Authors: Pierre Bergeron

7th edition

176530835, 978-0176530839