Answered step by step

Verified Expert Solution

Question

1 Approved Answer

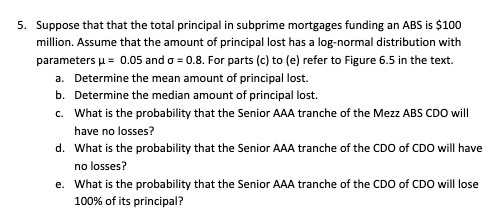

5. Suppose that that the total principal in subprime mortgages funding an ABS is $100 million. Assume that the amount of principal lost has

5. Suppose that that the total principal in subprime mortgages funding an ABS is $100 million. Assume that the amount of principal lost has a log-normal distribution with parameters = 0.05 and = 0.8. For parts (c) to (e) refer to Figure 6.5 in the text. a. Determine the mean amount of principal lost. b. Determine the median amount of principal lost. c. What is the probability that the Senior AAA tranche of the Mezz ABS CDO will have no losses? d. What is the probability that the Senior AAA tranche of the CDO of CDO will have no losses? e. What is the probability that the Senior AAA tranche of the CDO of CDO will lose 100% of its principal?

Step by Step Solution

★★★★★

3.46 Rating (146 Votes )

There are 3 Steps involved in it

Step: 1

a To determine the mean amount of principal lost we use the formula for the mean of a lognormal dist...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Engineers And Scientists

Authors: William Navidi

4th Edition

73401331, 978-0073401331