Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Imagine that a portfolio manager possessed the following predictions based on securities and macro analyses: Portfolio Expected Return Risk-free Market P 5% 17% 20%

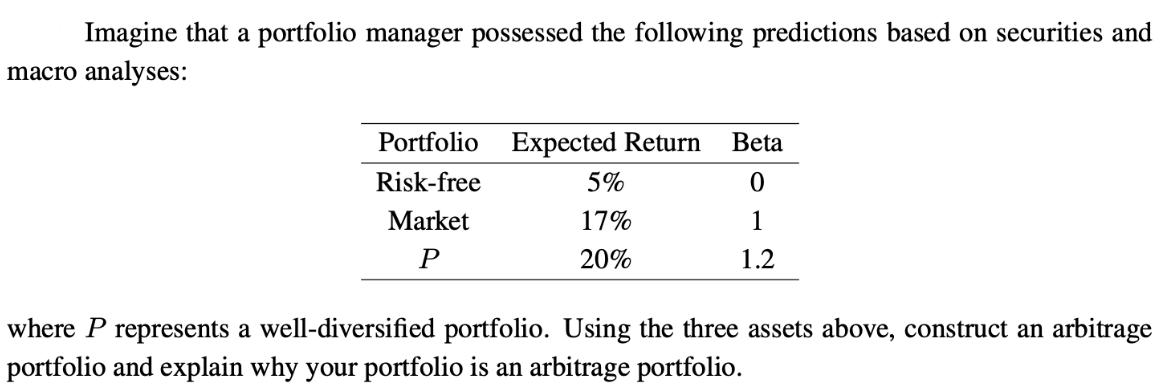

Imagine that a portfolio manager possessed the following predictions based on securities and macro analyses: Portfolio Expected Return Risk-free Market P 5% 17% 20% Beta 0 1 1.2 where P represents a well-diversified portfolio. Using the three assets above, construct an arbitrage portfolio and explain why your portfolio is an arbitrage portfolio.

Step by Step Solution

★★★★★

3.38 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

SOLUTION To construct an arbitrage portfolio we need to find a combination of the given assets that will generate riskfree profits regardless of the m...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516