Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Imagine that you have 10,000 to invest. What would be the combination of Asset A and Asset B that would yield you an expected

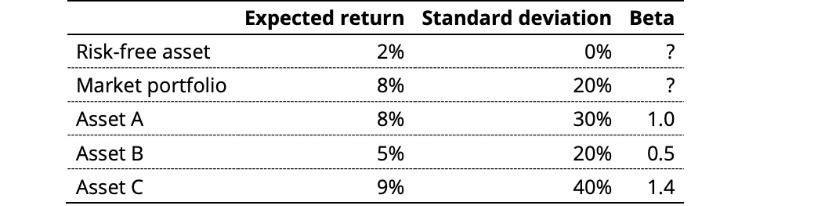

Imagine that you have 10,000 to invest. What would be the combination of Asset A and Asset B that would yield you an expected return of 4%? What is the standard deviation of the portfolio described in the previous question, knowing that the correlation coefficient between Asset A and Asset B is 0.2? Given the set of possible portfolios by combining Asset A and Asset B, would the portfolio in the previous questions be mean-variance efficient? Justify. Is asset C in equilibrium? Explain what will happen to the value of the asset, including your detailed rationale, assuming that the market is efficient. Risk-free asset Market portfolio Asset A Asset B Asset C Expected return Standard deviation Beta 2% 0% ? 8% 20% ? 8% 30% 1.0 5% 20% 0.5 9% 40% 1.4

Step by Step Solution

★★★★★

3.40 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the expected return and standard deviation of a portfolio we need the weights of the assets in the portfolio the expected returns of the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

11th edition

324422870, 324422873, 978-0324302691