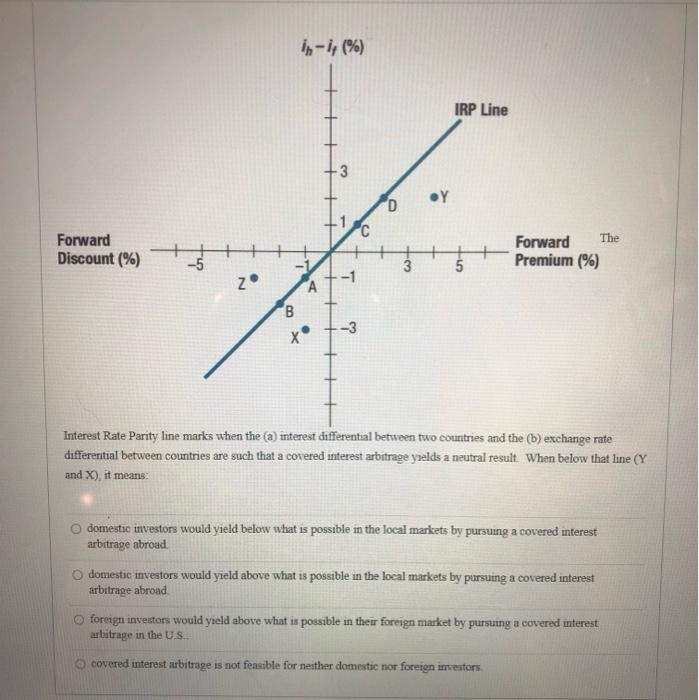

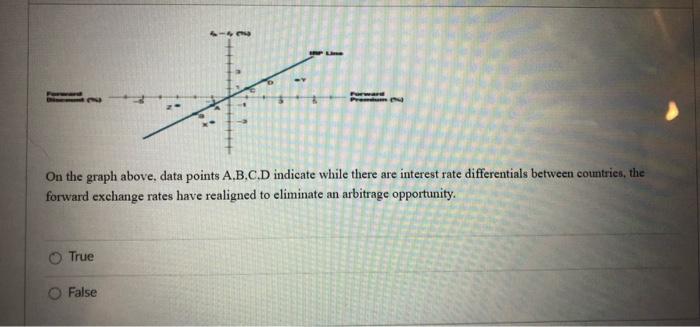

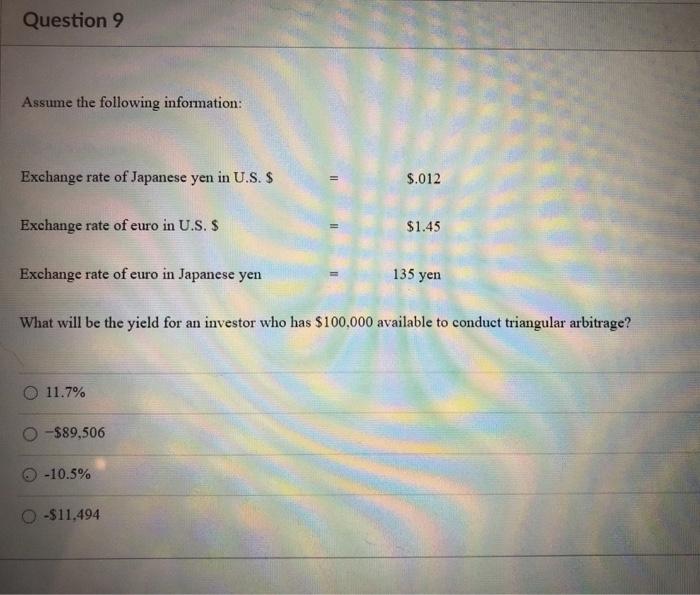

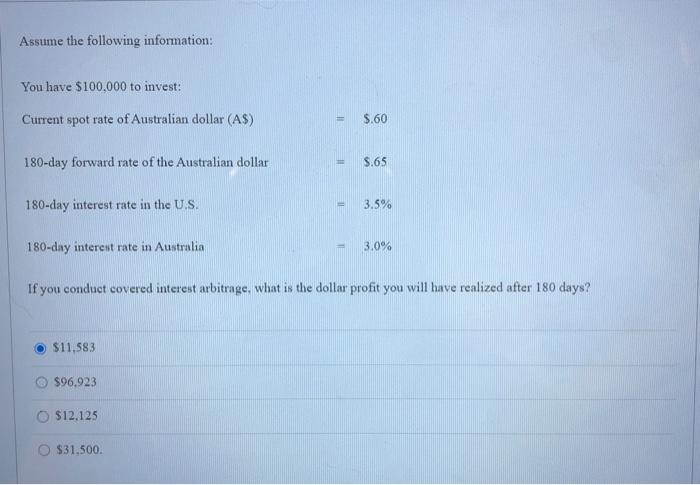

In - 14 %) IRP Line 3 3 .Y D C The Forward Discount (%) + Forward Premium (%) -5 3 -1 N A B -3 X Interest Rate Parity line marks when the (a) interest differential between two countries and the (b) exchange rate differential between countries are such that a covered interest arbitrage yields a neutral result. When below that line (Y and X), it means domestic investors would yield below what is possible in the local markets by pursuing a covered interest arbitrage abroad domestic investors would yield above what is possible in the local markets by pursuing a covered interest arbitrage abroad foreign investors would yield above what is possible in their foreign market by pursuing a covered interest arbitrage in the U.S. covered interest arbitrage is not feasible for neither domestic nor foreign investors - On the graph above, data points A.B.C.D indicate while there are interest rate differentials between countries, the forward exchange rates have realigned to eliminate an arbitrage opportunity True False Question 9 Assume the following information: Exchange rate of Japanese yen in U.S. $ $.012 Exchange rate of euro in U.S. $ $1.45 Exchange rate of euro in Japanese yen 135 yen What will be the yield for an investor who has $100.000 available to conduct triangular arbitrage? 11.7% -$89,506 -10.5% -$11.494 Assume the following information: You have $100,000 to invest: Current spot rate of Australian dollar (A$) $.60 180-day forward rate of the Australian dollar 5.65 180-day interest rate in the U.S. 3.5% 180-day interest rate in Australia 3.0% If you conduct covered interest arbitrage. what is the dollar profit you will have realized after 180 days? $11,583 $96.923 $12.125 O $31.500. In - 14 %) IRP Line 3 3 .Y D C The Forward Discount (%) + Forward Premium (%) -5 3 -1 N A B -3 X Interest Rate Parity line marks when the (a) interest differential between two countries and the (b) exchange rate differential between countries are such that a covered interest arbitrage yields a neutral result. When below that line (Y and X), it means domestic investors would yield below what is possible in the local markets by pursuing a covered interest arbitrage abroad domestic investors would yield above what is possible in the local markets by pursuing a covered interest arbitrage abroad foreign investors would yield above what is possible in their foreign market by pursuing a covered interest arbitrage in the U.S. covered interest arbitrage is not feasible for neither domestic nor foreign investors - On the graph above, data points A.B.C.D indicate while there are interest rate differentials between countries, the forward exchange rates have realigned to eliminate an arbitrage opportunity True False Question 9 Assume the following information: Exchange rate of Japanese yen in U.S. $ $.012 Exchange rate of euro in U.S. $ $1.45 Exchange rate of euro in Japanese yen 135 yen What will be the yield for an investor who has $100.000 available to conduct triangular arbitrage? 11.7% -$89,506 -10.5% -$11.494 Assume the following information: You have $100,000 to invest: Current spot rate of Australian dollar (A$) $.60 180-day forward rate of the Australian dollar 5.65 180-day interest rate in the U.S. 3.5% 180-day interest rate in Australia 3.0% If you conduct covered interest arbitrage. what is the dollar profit you will have realized after 180 days? $11,583 $96.923 $12.125 O $31.500