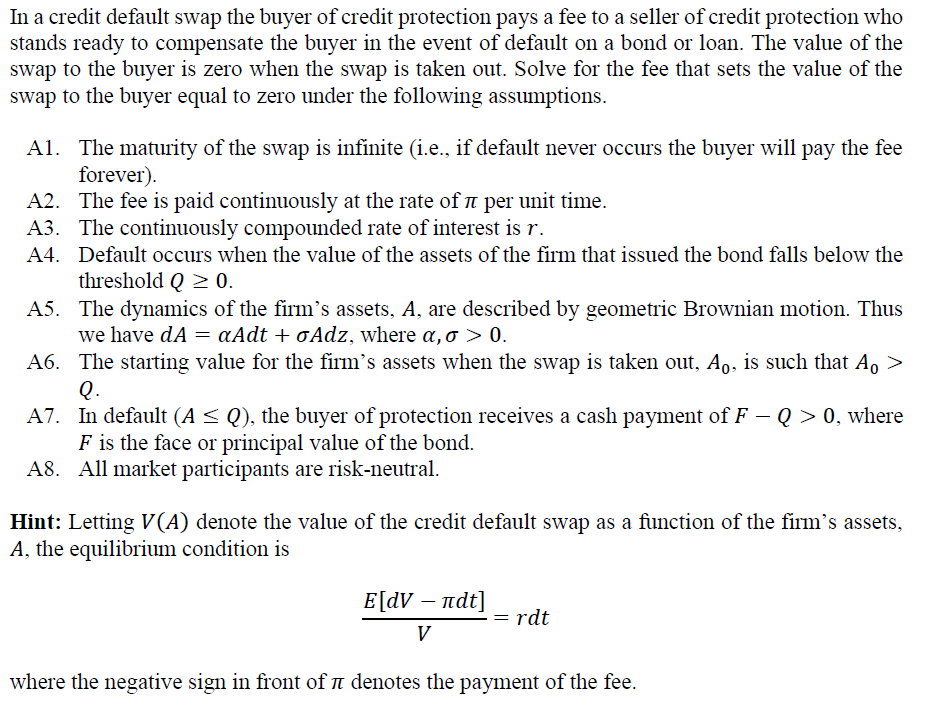

In a credit default swap the buyer of credit protection pays a fee to a seller of credit protection who stands ready to compensate the buyer in the event of default on a bond or loan. The value of the swap to the buyer is zero when the swap is taken out. Solve for the fee that sets the value of the swap to the buyer equal to zero under the following assumptions. Al. The maturity of the swap is infinite (.e., if default never occurs the buyer will pay the fee forever). A2. The fee is paid continuously at the rate of n per unit time. A3. The continuously compounded rate of interest is r. A4. Default occurs when the value of the assets of the firm that issued the bond falls below the threshold Q > 0. A5. The dynamics of the firm's assets, A, are described by geometric Brownian motion. Thus we have dA = a Adt + oAdz, where a,o > 0. A6. The starting value for the firm's assets when the swap is taken out, A., is such that A, > O A7. In default (ASQ), the buyer of protection receives a cash payment of F-Q > 0, where F is the face or principal value of the bond. A8. All market participants are risk-neutral. Hint: Letting V(A) denote the value of the credit default swap as a function of the firm's assets, A, the equilibrium condition is E[DV adt] -=rdt where the negative sign in front of a denotes the payment of the fee. In a credit default swap the buyer of credit protection pays a fee to a seller of credit protection who stands ready to compensate the buyer in the event of default on a bond or loan. The value of the swap to the buyer is zero when the swap is taken out. Solve for the fee that sets the value of the swap to the buyer equal to zero under the following assumptions. Al. The maturity of the swap is infinite (.e., if default never occurs the buyer will pay the fee forever). A2. The fee is paid continuously at the rate of n per unit time. A3. The continuously compounded rate of interest is r. A4. Default occurs when the value of the assets of the firm that issued the bond falls below the threshold Q > 0. A5. The dynamics of the firm's assets, A, are described by geometric Brownian motion. Thus we have dA = a Adt + oAdz, where a,o > 0. A6. The starting value for the firm's assets when the swap is taken out, A., is such that A, > O A7. In default (ASQ), the buyer of protection receives a cash payment of F-Q > 0, where F is the face or principal value of the bond. A8. All market participants are risk-neutral. Hint: Letting V(A) denote the value of the credit default swap as a function of the firm's assets, A, the equilibrium condition is E[DV adt] -=rdt where the negative sign in front of a denotes the payment of the fee