Answered step by step

Verified Expert Solution

Question

1 Approved Answer

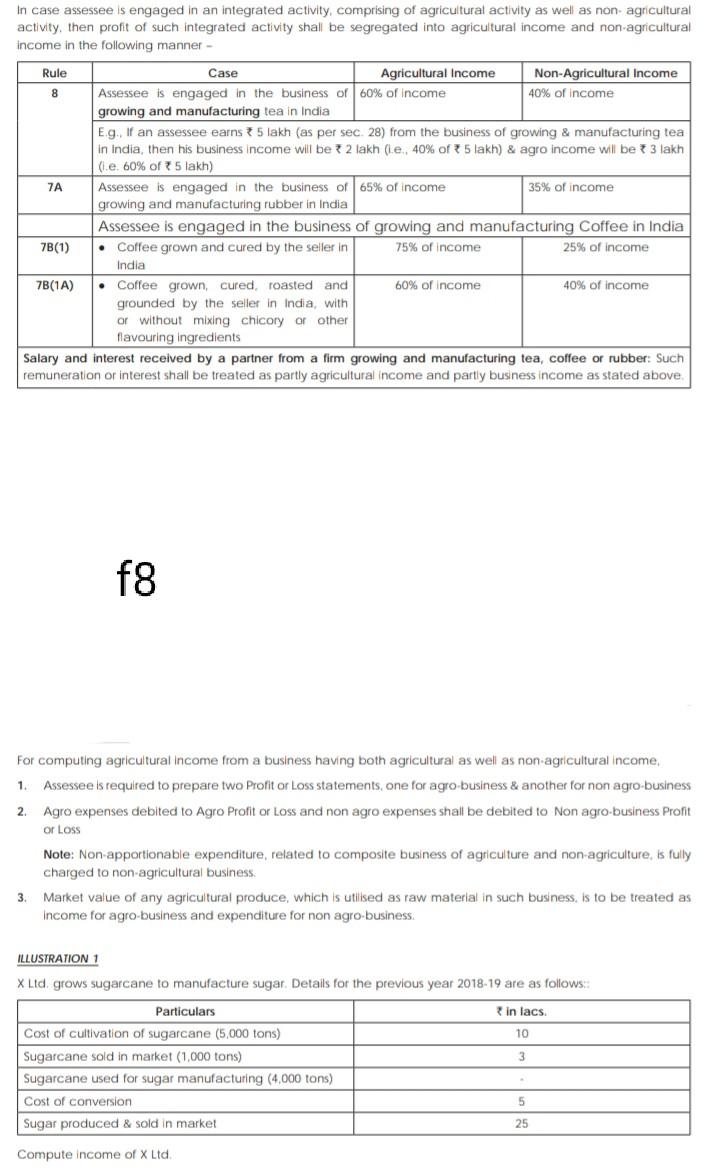

In case assessee is engaged in an integrated activity, comprising of agricultural activity as well as non agricultural activity, then profit of such integrated activity

In case assessee is engaged in an integrated activity, comprising of agricultural activity as well as non agricultural activity, then profit of such integrated activity shall be segregated into agricultural income and non-agricultural Income in the following manner Rule Case Agricultural Income Non-Agricultural Income 8 Assessee is engaged in the business of 60% of income 40% of income growing and manufacturing tea in India Eg. If an assessee earns 5 lakh (as per sec. 28) from the business of growing & manufacturing tea in India, then his business income will be 2 lakh (.e. 40% of 5 lakh) & agro income will be 3 lakh (.e. 60% of 5 lakh) 7A Assessee is engaged in the business of 65% of income 35% of income growing and manufacturing rubber in India Assessee is engaged in the business of growing and manufacturing Coffee in India 7B(1) Coffee grown and cured by the seller in 75% of income 25% of income India 7B(1A) Coffee grown, cured, roasted and 60% of income 40% of income grounded by the seller in India, with or without mixing chicory or other flavouring Ingredients Salary and interest received by a partner from a firm growing and manufacturing tea, coffee or rubber: Such remuneration or interest shall be treated as partly agricultural income and partly business income as stated above . f8 For computing agricultural income from business having both agricultural as well as non-agricultural income, 1. Assessee is required to prepare two Profit or Loss statements, one for agro-business & another for non agro-business 2. Agro expenses debited to Agro Profit or Loss and non agro expenses shall be debited to Non agro-business Profit or Loss Note: Non-apportionable expenditure, related to composite business of agriculture and non-agriculture, is fully ged to non-agricultural business Market value of any agricultural produce, which is utilised as raw material in such business, is to be treated as Income for agro-business and expenditure for non agro business. 3. ILLUSTRATION 1 X Ltd. grows sugarcane to manufacture sugar. Details for the previous year 2018-19 are as follows: in lacs. 10 3 Particulars Cost of cultivation of sugarcane (5,000 tons) Sugarcane sold in market (1.000 tons) Sugarcane used for sugar manufacturing (4,000 tons) Cost of conversion Sugar produced & sold in market . 5 25 Compute income of X Ltd

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

FINANCIAL & MANAGERIAL ACCOUNTING FOR DECISION MAKERS

Authors: Dyckman, Hanlon, Magee, Pfeiffer, Hartgraves, Morse

3rd Edition

1618532340, 9781618532343