Answered step by step

Verified Expert Solution

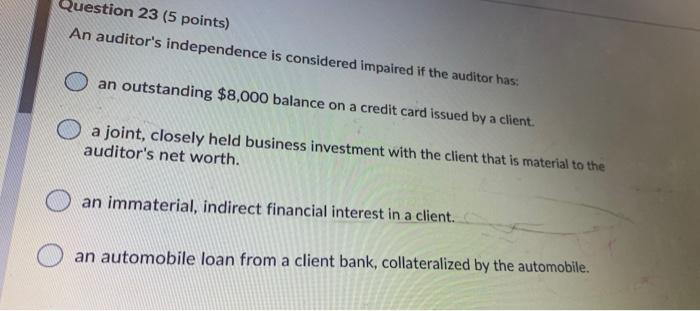

Question

1 Approved Answer

In compliance audits the auditor Determine whether a client is following a specific regulation set by some higher authority. Evaluates efficiency and the effectiveness of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Statement Fraud Strategies For Detection And Investigation

Authors: Gerard M. Zack

1st Edition

1118301552, 9781118301555