Question

In late 2007, Mr. X, a scientist, successfully acquired a patent for one of his inventions, a light bulb that was powered by oxygen from

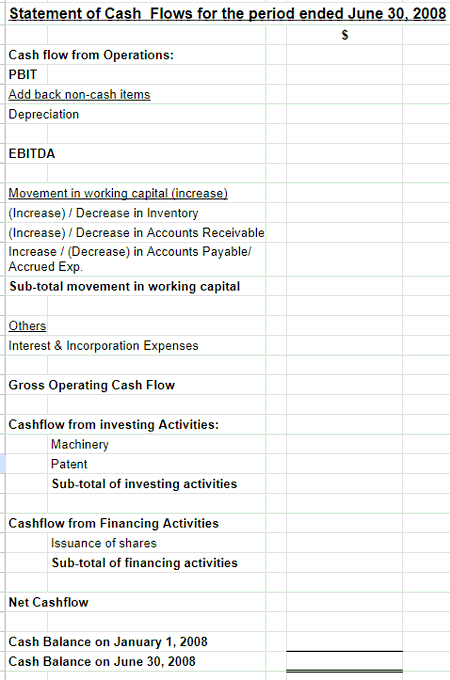

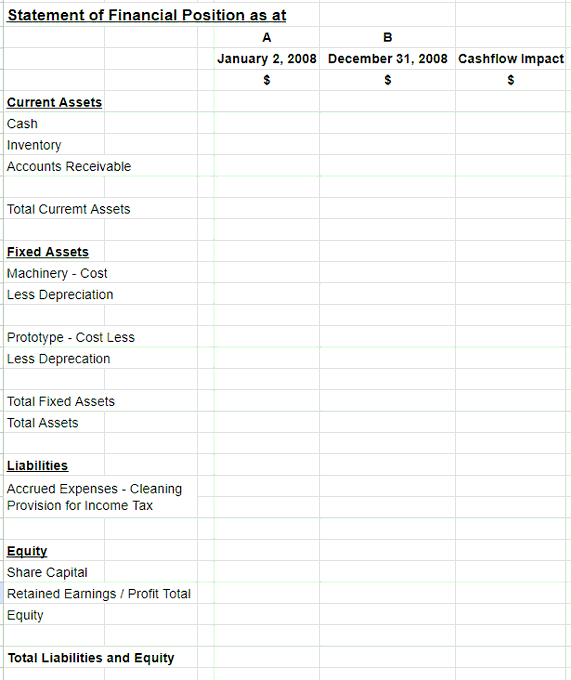

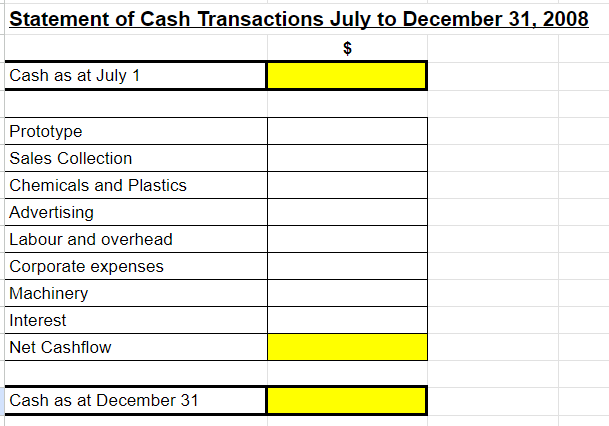

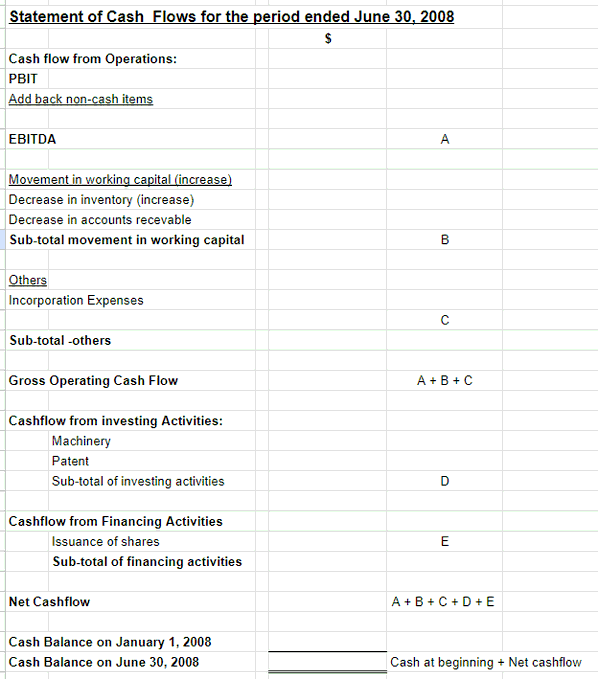

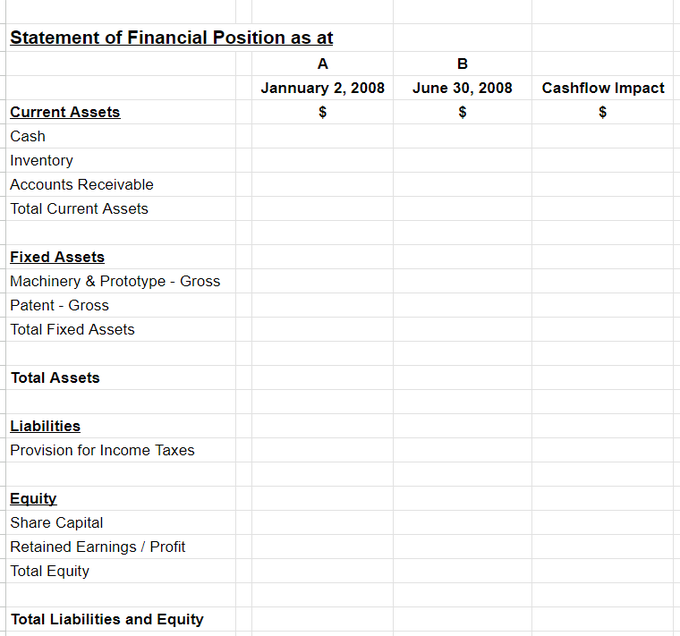

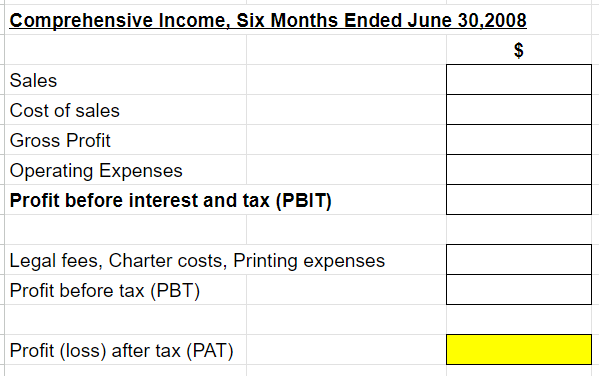

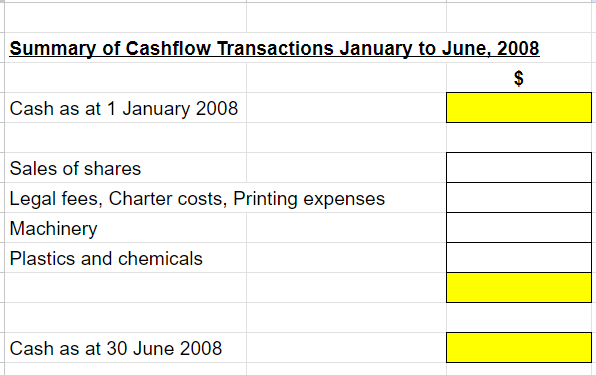

In late 2007, Mr. X, a scientist, successfully acquired a patent for one of his inventions, a light bulb that was powered by oxygen from the air. Mr. X anticipated a substantial market for his invention including demand from governments and third world countries. On January 2, 2008, Mr. X together with his friends, established Oxy-lit Company. The company issued 500,000 shares and Mr. X received 125,000 shares in exchange for his patent. Other investors bought in at $1 per share. During the period from January 2, 2008 through June 30 2008, Oxy-lit incurred the following expenditures: January 15 $7,500 paid for incorporation expenses (legal fees, charter costs and printing). June 15 Spent $62,500 to assemble the machinery for producing the first commercial model of the Oxy-lit lights. June 24 Purchased $75,000 worth of plastics and chemicals as raw materials for production of Oxy-lit lights. Towards the end of June, a stockholders meeting was held and Mr. X, who had assumed a very active management role reported on the companys status and marketing plans (which was targeted to begin by end August). However, during the meeting, Mr. Biggie, one stockholder who had little understanding of financial statements, interjected, All this discussion of our business plan is good, but how come six months ago, we had $375,000 and now we only have $230,000? Weve already lost $145,000 in six months without even starting yet. Some of the shareholders agreed with Mr. Biggie. Indeed, between January 2 and June 30, the companys bank balance had fallen from $375,000 to $230,000. Ms. Queen, a shareholder, explained that since Oxy-lits operations were not yet in full swing, these are actually pre-operating outlays that should be considered as business investments rather than losses. The shareholders agreed to meet again in early January 2009 to review the state of the corporation. They expected the company to be in full operation by then and the birth pains of the pre-operating period overcome by year-end. During the last half of 2008, Oxy-lit did go into full operation. To prepare for the shareholders meeting in early January 2009, Mr. Cal, the companys accountant, produced the following data: In early July 2008, the engineer who delivered the prototypes of the Oxy-lit lights was paid a total of $23,750. During the six months from July to December 2008, Oxy-lit had $754,500 in sales. The largest single customer, a factory, still owed Oxy-lit $69,500. All other customers accounts were fully paid by the end of the year. Additional raw materials (chemicals and plastics) were purchased for a total of $175,000 - paid in cash. Oxy-lit spent $22,500 on TV and other advertising to market its lights. During the six months ended December 31, 2008, the company spent $350,000 on manufacturing direct labor and overhead (rent, utilities, supervisory labor). An additional $80,000 was spent on corporate salaries and expenses. In early July, a further $150,000 was spent on production machinery. During the period, the company borrowed $50,000 via short-term loan and repaid it by year end. The interest paid on the loan was $750. The company called in cleaning and pest control services on 1 December 2008 to get rid of vermin chewing on cables. The $2,100 bill was paid on 3 January 2009. In preparing his report, Mr. X was anxious about how the companys bank balance had fallen even more by $117,000 from Junes $230,000 to only $113,000. It puzzled him because he supposed the company was faring well and he couldnt understand why the bank balance did not seem to reflect this condition. Upon reviewing the cash outflow for the entire year, Mr. X noted the following: There was still $55,000 in raw materials inventory as of December 31; while there were no finished or partially finished Oxy-lit lights by year end. Although the patent on Mr. Xs invention had a legal life of 17 years, he expected competitors to develop similar products in about five years. The machinery used in the production of Oxy-lit lights was general purpose machinery, with an expected useful life of 10 years, and their use not limited to Oxy-lit lights production. The machinery had already been in use for 6 months. Mr. X speculated on the worth of the prototypes. Since they directly resulted in the development of the product the company was selling, their value could have increased over the last six months of 2008. The Committee organizing the Olympics had placed an order with the company for 60,000 Oxy-lit lights at a price of $1.50 each to be delivered just before the start of the games. It is their intention to give an Oxy-lit light to each person at the opening ceremony. Assume corporate tax at 30%. Mr. X, being more of a scientist than a businessperson was at a loss on how to present the company developments to the shareholders. He believed that the company was performing well, but he did not know how to convey this to the other shareholders. Questions: 1. Prepare a summary of the cash transactions for the six months ended June 30, 2008. 2. Prepare a Statement of Comprehensive Income for the six months ended June 30, 2008. Did the company incur a loss as Mr. Biggie suggested? 3. Prepare a Statement of Financial Position at January 2, 2008; June 30, 2008 and cash flow statement for the six- month period. 4. Prepare a summary of the cash transactions for the six months from 1 July 2008 to 31 December 2009. 5. Prepare a set of financial statements for the shareholders for the year 2008; a Statement of Financial Position as at December 31, 2008; a P&L and Statement of Cash Flows for the year ended December 31, 2008. 6. How would you advise Mr. X on the performance of the company? Instructions: Fill up the values from the given tables in the pictures.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting Volume 2

Authors: Thomas H. Beechy, Joan E. Conrod, Elizabeth Farrell, Ingrid McLeod-Dick, Kayla Tomulka, Romi-Lee Sevel

8th Edition

1260881245, 9781260881240