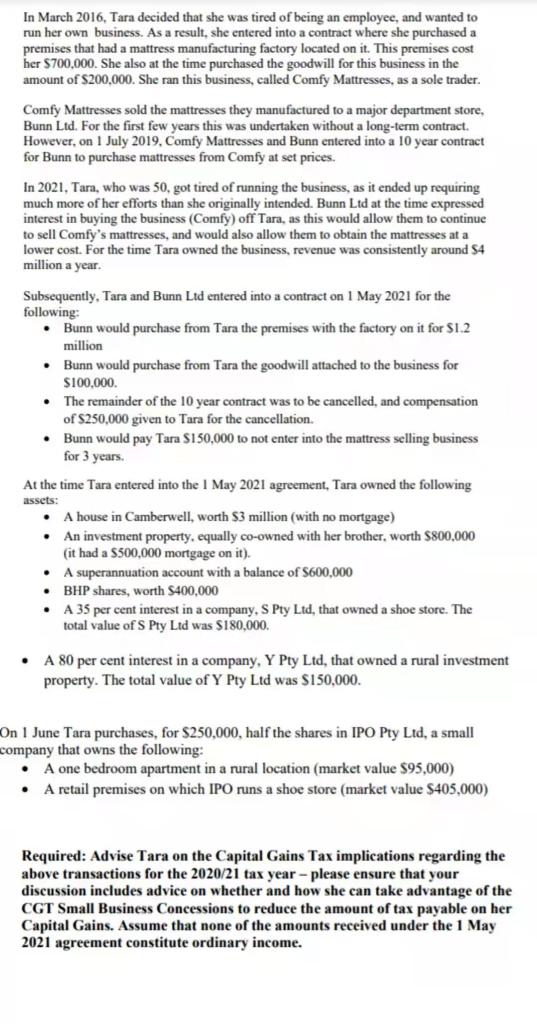

In March 2016, Tara decided that she was tired of being an employee, and wanted to run her own business. As a result, she entered into a contract where she purchased a premises that had a mattress manufacturing factory located on it. This premises cost her $700,000. She also at the time purchased the goodwill for this business in the amount of S200,000. She ran this business, called Comfy Mattresses, as a sole trader. . Comfy Mattresses sold the mattresses they manufactured to a major department store, Bunn Ltd. For the first few years this was undertaken without a long-term contract. However, on 1 July 2019, Comfy Mattresses and Bunn entered into a 10 year contract for Bunn to purchase mattresses from Comfy at set prices. In 2021, Tara, who was 50, got tired of running the business, as it ended up requiring much more of her efforts than she originally intended. Bunn Ltd at the time expressed interest in buying the business (Comfy) off Tara, as this would allow them to continue to sell Comfy's mattresses, and would also allow them to obtain the mattresses at a lower cost. For the time Tara owned the business, revenue was consistently around $4 million a year. Subsequently, Tara and Bunn Ltd entered into a contract on 1 May 2021 for the following: Bunn would purchase from Tara the premises with the factory on it for $1.2 million Bunn would purchase from Tara the goodwill attached to the business for $100.000 The remainder of the 10 year contract was to be cancelled, and compensation of $250,000 given to Tara for the cancellation. Bunn would pay Tara $150,000 to not enter into the mattress selling business for 3 years. At the time Tara entered into the I May 2021 agreement, Tara owned the following assets: A house in Camberwell, worth 53 million (with no mortgage) An investment property, equally co-owned with her brother, worth $800,000 (it had a $500,000 mortgage on it). A superannuation account with a balance of $600,000 BHP shares, worth $400,000 A 35 per cent interest in a company. S Pty Ltd, that owned a shoe store. The total value of S Pty Ltd was $180,000. . . . . A 80 per cent interest in a company, Y Pty Ltd, that owned a rural investment property. The total value of Y Pty Ltd was $150,000. On 1 June Tara purchases, for $250,000, half the shares in IPO Pty Ltd, a small company that owns the following: A one bedroom apartment in a rural location (market value $95,000) A retail premises on which IPO runs a shoe store market value $405.000) Required: Advise Tara on the Capital Gains Tax implications regarding the above transactions for the 2020/21 tax year - please ensure that your discussion includes advice on whether and how she can take advantage of the CGT Small Business Concessions to reduce the amount of tax payable on her Capital Gains. Assume that none of the amounts received under the 1 May 2021 agreement constitute ordinary income. In March 2016, Tara decided that she was tired of being an employee, and wanted to run her own business. As a result, she entered into a contract where she purchased a premises that had a mattress manufacturing factory located on it. This premises cost her $700,000. She also at the time purchased the goodwill for this business in the amount of S200,000. She ran this business, called Comfy Mattresses, as a sole trader. . Comfy Mattresses sold the mattresses they manufactured to a major department store, Bunn Ltd. For the first few years this was undertaken without a long-term contract. However, on 1 July 2019, Comfy Mattresses and Bunn entered into a 10 year contract for Bunn to purchase mattresses from Comfy at set prices. In 2021, Tara, who was 50, got tired of running the business, as it ended up requiring much more of her efforts than she originally intended. Bunn Ltd at the time expressed interest in buying the business (Comfy) off Tara, as this would allow them to continue to sell Comfy's mattresses, and would also allow them to obtain the mattresses at a lower cost. For the time Tara owned the business, revenue was consistently around $4 million a year. Subsequently, Tara and Bunn Ltd entered into a contract on 1 May 2021 for the following: Bunn would purchase from Tara the premises with the factory on it for $1.2 million Bunn would purchase from Tara the goodwill attached to the business for $100.000 The remainder of the 10 year contract was to be cancelled, and compensation of $250,000 given to Tara for the cancellation. Bunn would pay Tara $150,000 to not enter into the mattress selling business for 3 years. At the time Tara entered into the I May 2021 agreement, Tara owned the following assets: A house in Camberwell, worth 53 million (with no mortgage) An investment property, equally co-owned with her brother, worth $800,000 (it had a $500,000 mortgage on it). A superannuation account with a balance of $600,000 BHP shares, worth $400,000 A 35 per cent interest in a company. S Pty Ltd, that owned a shoe store. The total value of S Pty Ltd was $180,000. . . . . A 80 per cent interest in a company, Y Pty Ltd, that owned a rural investment property. The total value of Y Pty Ltd was $150,000. On 1 June Tara purchases, for $250,000, half the shares in IPO Pty Ltd, a small company that owns the following: A one bedroom apartment in a rural location (market value $95,000) A retail premises on which IPO runs a shoe store market value $405.000) Required: Advise Tara on the Capital Gains Tax implications regarding the above transactions for the 2020/21 tax year - please ensure that your discussion includes advice on whether and how she can take advantage of the CGT Small Business Concessions to reduce the amount of tax payable on her Capital Gains. Assume that none of the amounts received under the 1 May 2021 agreement constitute ordinary income