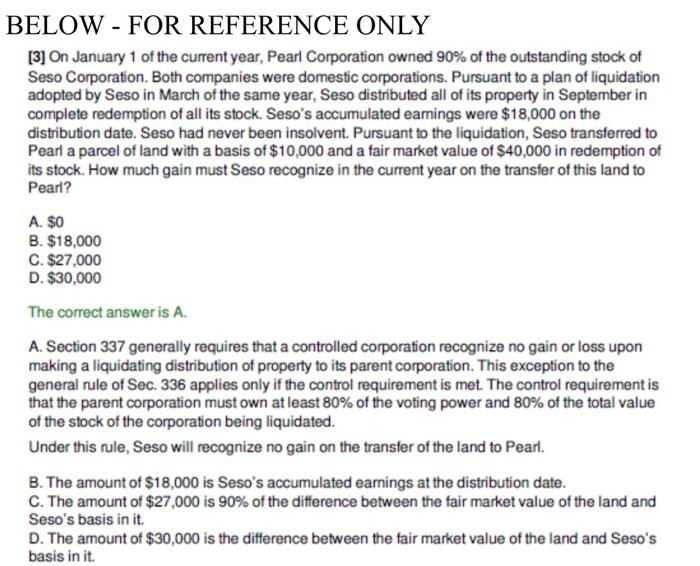

In MC17 you learned about consolidated tax returns. The facts of this assignment are based on question 3 (posted below; also linked here.) Please read the instructions for Item A. Identifying Information Consolidated Return (page 8). In addition to Form 1120, there are two additional forms that must be submitted based on the instructions. Please attach a partially completed: Form 1120 (Focus on the top of page 1) Form 851 (Name and Part II) Form 1122 Ignore the transaction described, but please just focus on the boxes that must be checked and information that must be provided to file a consolidated return. The purpose of this assignment is to make the abstract lesson in the MC tangible. Please also comment on what you have learned. BELOW FOR REFERENCE ONLY [3] On January 1 of the current year, Pearl Corporation owned 90% of the outstanding stock of Seso Corporation. Both companies were domestic corporations. Pursuant to a plan of liquidation adopted by Seso in March of the same year, Seso distributed all of its property in September in complete redemption of all its stock. Seso's accumulated eamings were $18,000 on the distribution date. Seso had never been insolvent. Pursuant to the liquidation, Seso transferred to Pearl a parcel of land with a basis of $10,000 and a fair market value of $40,000 in redemption of its stock. How much gain must Seso recognize in the current year on the transfer of this land to Pearl? A. $0 B. $18,000 C. $27,000 D. $30,000 The correct answer is A. A. Section 337 generally requires that a controlled corporation recognize no gain or loss upon making a liquidating distribution of property to its parent corporation. This exception to the general rule of Sec. 336 applies only if the control requirement is met. The control requirement is that the parent corporation must own at least 80% of the voting power and 80% of the total value of the stock of the corporation being liquidated. Under this rule, Seso will recognize no gain on the transfer of the land to Pearl. B. The amount of $18,000 is Seso's accumulated earnings at the distribution date. C. The amount of $27,000 is 90% of the difference between the fair market value of the land and Seso's basis in it. D. The amount of $30,000 is the difference between the fair market value of the land and Seso's basis in it. In MC17 you learned about consolidated tax returns. The facts of this assignment are based on question 3 (posted below; also linked here.) Please read the instructions for Item A. Identifying Information Consolidated Return (page 8). In addition to Form 1120, there are two additional forms that must be submitted based on the instructions. Please attach a partially completed: Form 1120 (Focus on the top of page 1) Form 851 (Name and Part II) Form 1122 Ignore the transaction described, but please just focus on the boxes that must be checked and information that must be provided to file a consolidated return. The purpose of this assignment is to make the abstract lesson in the MC tangible. Please also comment on what you have learned. BELOW FOR REFERENCE ONLY BELOW - FOR REFERENCE ONLY [3] On January 1 of the current year, Pearl Corporation owned 90% of the outstanding stock of Seso Corporation. Both companies were domestic corporations. Pursuant to a plan of liquidation adopted by Seso in March of the same year, Seso distributed all of its property in September in complete redemption of all its stock. Seso's accumulated earnings were $18,000 on the distribution date. Seso had never been insolvent. Pursuant to the liquidation, Seso transferred to Pearl a parcel of land with a basis of $10,000 and a fair market value of $40,000 in redemption of its stock. How much gain must Seso recognize in the current year on the transfer of this land to Pearl? A. $0 B. $18,000 C. $27,000 D. $30,000 The correct answer is A. A. Section 337 generally requires that a controlled corporation recognize no gain or loss upon making a liquidating distribution of property to its parent corporation. This exception to the general rule of Sec. 336 applies only if the control requirement is met. The control requirement is that the parent corporation must own at least 80% of the voting power and 80% of the total value of the stock of the corporation being liquidated. Under this rule, Seso will recognize no gain on the transfer of the land to Pearl. B. The amount of $18,000 is Seso's accumulated earnings at the distribution date. C. The amount of $27,000 is 90% of the difference between the fair market value of the land and Seso's basis in it. D. The amount of $30,000 is the difference between the fair market value of the land and Seso's basis in it