Answered step by step

Verified Expert Solution

Question

1 Approved Answer

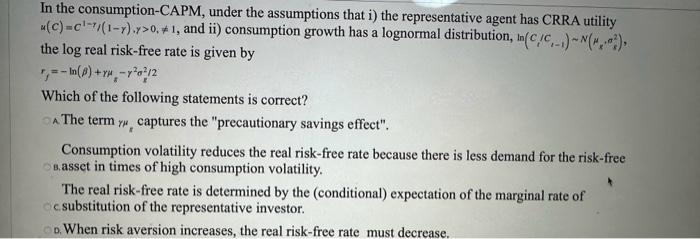

In the consumption-CAPM, under the assumptions that i) the representative agent has CRRA utility u(c)=C1/(1),>0,=1, and ii) consumption growth has a lognormal distribution, ln(c1/C11)N(s,s2), the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Adjusted Performance And Bank Governance Structures

Authors: Christoph Böhm

1st Edition

3631639163, 3653027306, 9783631639160, 9783653027303