Answered step by step

Verified Expert Solution

Question

1 Approved Answer

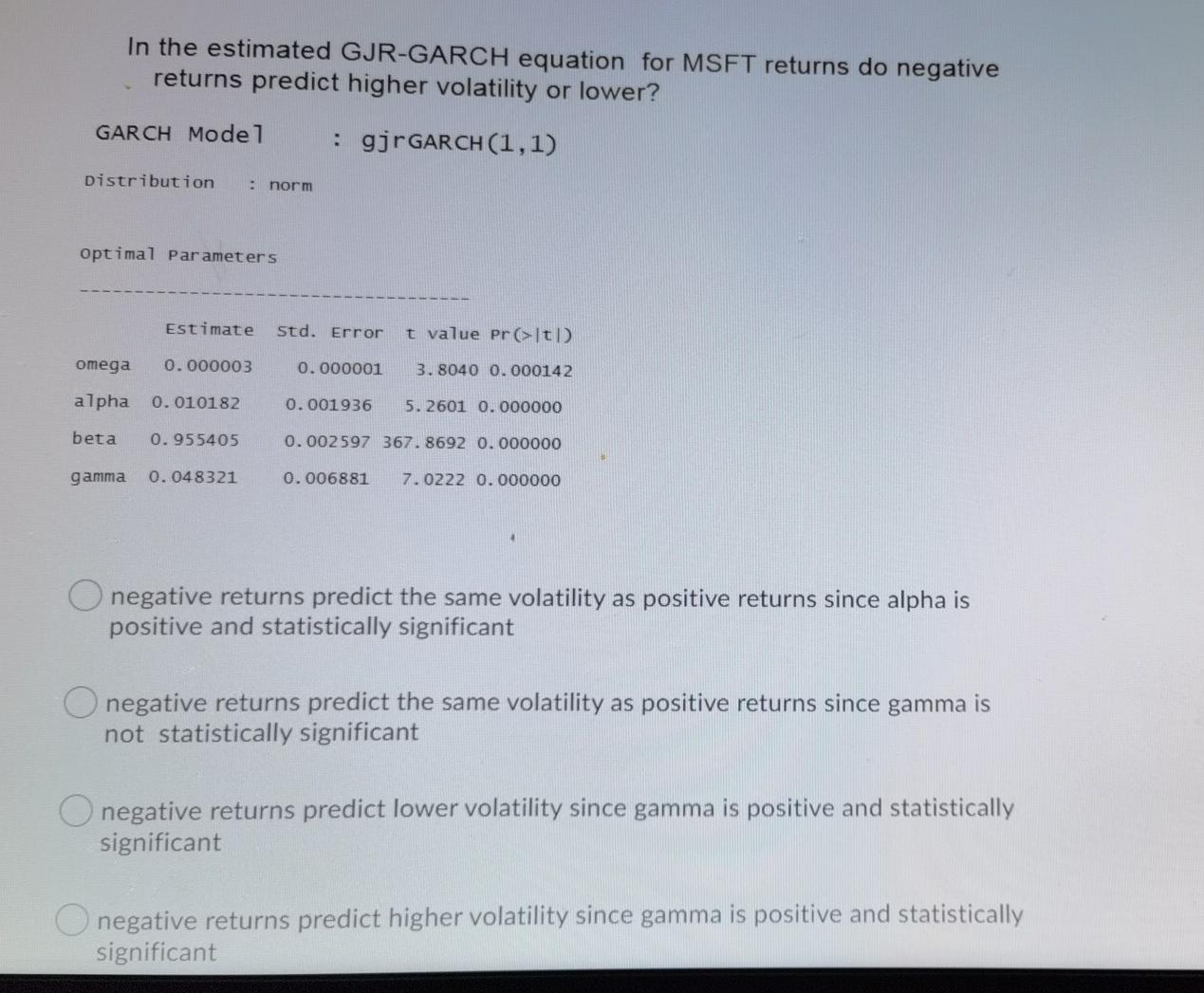

In the estimated GJR-GARCH equation for MSFT returns do negative returns predict higher volatility or lower? GARCH Model : gjrGARCH (1,1) distribution : norm optimal

In the estimated GJR-GARCH equation for MSFT returns do negative returns predict higher volatility or lower? GARCH Model : gjrGARCH (1,1) distribution : norm optimal parameters Estimate Std. Error t value pret omega 0.000003 0.000001 3.8040 0.000142 alpha 0.010182 0.001936 5. 2601 0.000000 beta 0.955405 0.002597 367.8692 0.000000 gamma 0.048321 0.006881 7.0222 0.000000 negative returns predict the same volatility as positive returns since alpha is positive and statistically significant negative returns predict the same volatility as positive returns since gamma is not statistically significant negative returns predict lower volatility since gamma is positive and statistically significant negative returns predict higher volatility since gamma is positive and statistically significant

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Grow The Pie How Great Companies Deliver Both Purpose And Profit

Authors: Alex Edmans

1st Edition

1108494854,1108849482