Question

In this code i need to change the variables for calculating Delta and Vega using the likelihood ratio method for Asian option, because the current

In this code i need to change the variables for calculating Delta and Vega using the likelihood ratio method for Asian option, because the current formulas in the code below are not correct and gives dimensional error. Note: Please don't use AI to solve this problem.

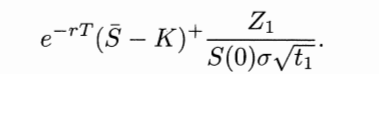

The formulas that should be used are:

Delta:

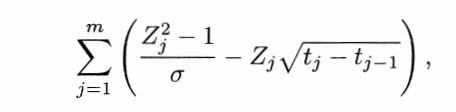

Vega:

Vega:

The code provided is the following:

import numpy as np import pandas as pd from IPython.display import Markdown, display

S0 = 100 K = np.array([80, 100, 120]).reshape(1, 3) r = 0.03 sigma = 0.2 T = 1 m = np.array([12, 52]) number_of_sim = 20000 h = np.array([1, 0.01]) dt = 1 / m

time_step = {0: np.arange(dt[0], T + dt[0], dt[0]).reshape(1, m[0])} S = {0: np.zeros((number_of_sim, m[0]))} Z = {0: np.random.standard_normal((number_of_sim, m[0]))} delta = {0: np.zeros((1, 3))} vega = {0: np.zeros((1, 3))}

for i in range(1, 2): time_step[i] = np.arange(dt[i], T + dt[i], dt[i]).reshape(1, m[1]) Z[i] = np.random.standard_normal((number_of_sim, m[i])) S[i] = np.zeros((number_of_sim, m[i])) delta[i] = np.zeros((1, 3)) vega[i] = np.zeros((1, 3))

for i in range(2): S[i][:, 0] = S0 * np.exp((r - 0.5 * sigma**2) * dt[i] + np.sqrt(dt[i]) * sigma * Z[i][:, 0])

for i in range(2): for j in range(m[i] - 1): S[i][:, j + 1] = S[i][:, j] * np.exp((r - 0.5 * sigma**2) * dt[i] + np.sqrt(dt[i]) * sigma * Z[i][:, j + 1])

# Calculate mean_S for each case (m=12 and m=52) mean_S = {0: np.mean(S[0], axis=1).reshape(number_of_sim, 1), 1: np.mean(S[1], axis=1).reshape(number_of_sim, 1)}

# Initialize Delta and Vega dictionaries for both cases delta = {0: np.zeros((1, 3)), 1: np.zeros((1, 3)} vega = {0: np.zeros((1, 3)), 1: np.zeros((1, 3)}

for i in range(2): # Calculate Delta using the likelihood ratio method delta[i] = np.exp(-r * T) * (mean_S[i] > K) * (Z[i][:, -1] / (S0 * sigma * np.sqrt(T / m[i]))) # Calculate Vega using the likelihood ratio method vega[i] = np.exp(-r * T) * (mean_S[i] > K) * np.sum((Z[i]**2 - 1) / sigma - Z[i] * np.sqrt(time_step[i][0, 1:]), axis=1) / S0

strikes = ['K = 80', 'K = 100', 'K = 120']

df = pd.DataFrame(index=['Delta (LRM)', 'Vega (LRM)'], columns=strikes)

for i in range(3): df.loc['Delta (LRM)', strikes[i]] = round(delta[0][i], 3) df.loc['Vega (LRM)', strikes[i]] = round(vega[0][i], 3)

display(Markdown("#### Asian call m = 12")) display(df)

df2 = pd.DataFrame(index=['Delta (LRM)', 'Vega (LRM)'], columns=strikes)

for i in range(3): df2.loc['Delta (LRM)', strikes[i]] = round(delta[1][i], 3) df2.loc('Vega (LRM)', strikes[i]] = round(vega[1][i], 3)

display(Markdown("#### Asian call m = 52")) display(df2)

erT(SK)+S(0)t1Z1 j=1m(Zj21Zjtjtj1) erT(SK)+S(0)t1Z1 j=1m(Zj21Zjtjtj1)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Stanley Eakins Frederic Mishkin

9th Global Edition

1292215003, 978-1292215006