Answered step by step

Verified Expert Solution

Question

1 Approved Answer

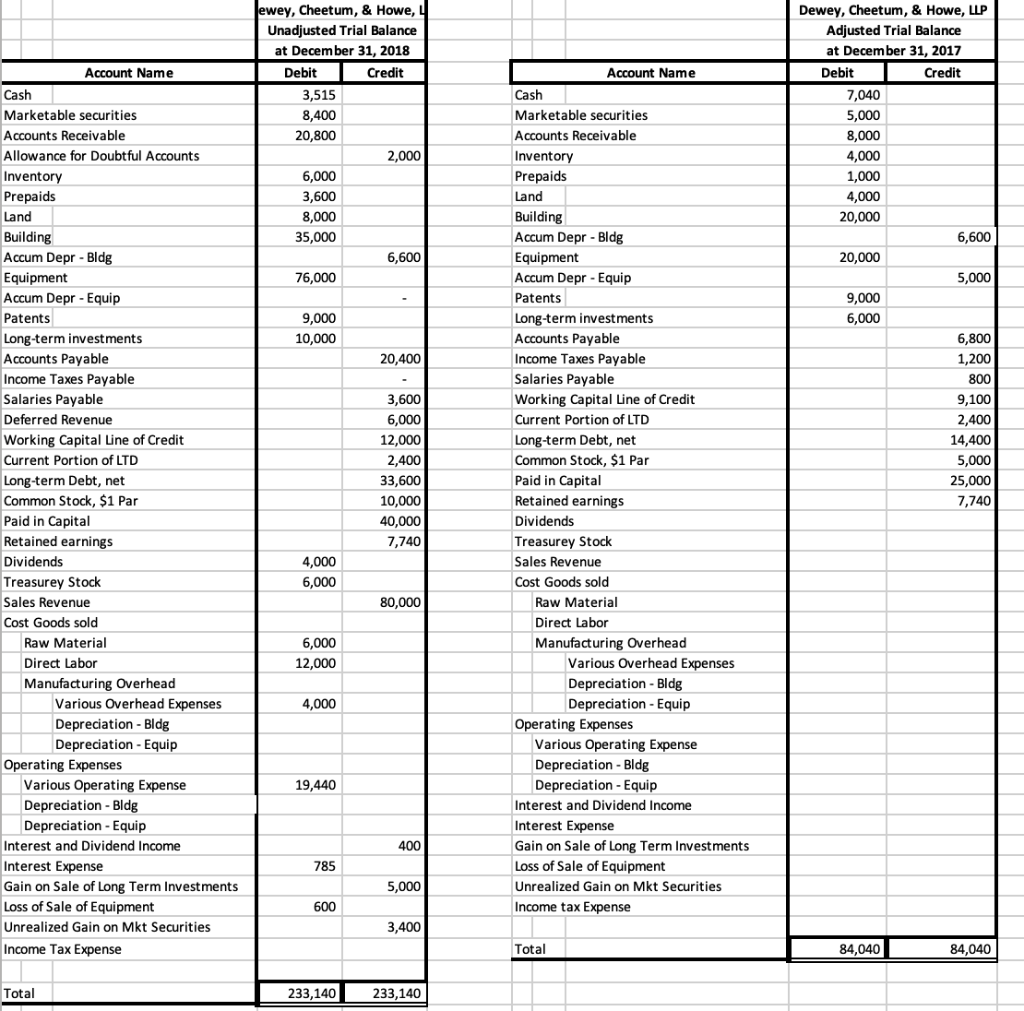

Information for the problem: 1) The only change in marketable securities is a Fair market value adjustment at year end 2) The Company set up

| Information for the problem: | ||

| 1) The only change in marketable securities is a Fair market value adjustment at year end | ||

| 2) The Company set up an allowance for doubtful accounts in 2018 and the change is the bad debt expense recorded in operating expenses | ||

| 3) Prepaids at the beginning and ending of the year represent a three year policy that was renewed in 2018 | ||

| the balance at 12/31/18 represents the new three year policy and hasnt been adjusted for use during 2018 | ||

| the beginning balance represents what was left to be used during 2018 on the old three year policy which also cost $3600 originally | ||

| 4) the change in land and building was a aquistioin that was purchased in 2018 with stock of the corporation | ||

| No Deprecation for the year has been recorded | ||

| The new building will be depreciated over 30 years using the straight line method and was purchased on August 1st | ||

| The old building is depreciated on the straighline basis over 30 years also | ||

| Also the building is split 80% factory, 20% administrative | ||

| 5) On January 1st the company totally renovated their equipment and added new machinery to their production lines | ||

| All the equipment at 12-31-17 was sold for $14,400 on 1/1/18 | ||

| and the new equipment was purchased the same day and will be depreciated over 7 yrs | ||

| no depreciation was recorded during the year | ||

| also the equipment is split 90% factory, 10% administrative | ||

| 6) Patents were acquired in 2017 and amortized on the straightline basis over 10 yrs | ||

| No amortization has been recorded in 2018 | ||

| 7) Longterm investments with an original cost of $4000 was sold for $9000 | ||

| 8) the corporate tax rate is 25% | ||

| 9) Revenue shipped of $6,000 on 12/31/18 was not recorded till 1/3/19. Completed by 12/31 | ||

| 10) Operating expenses of $4,000 at 12/31/18 were not recorded til 1/10/19. Wasnt Paid | ||

| 11) on 10/31/18 a customer gave us an advance of $6000 and as of 12/31/18 we only shipped $2000 of the product | ||

| 12) Interest on Working Capital Line of Credit is accrued at 6% on the average balance for the year and no interest has been accrued or paid on this line | ||

| 13) The long term debt at the beginning of the year is a fixed principle loan with the principle payment fixed at $200 a month | ||

| 12 payments have been made with interest and (have been recorded) | ||

| Interest is calculated at 5% of the outstanding balance at the beginning of the month | ||

| 14) Any increase in long-term debt is a new loan taken out on 8/1/18 payable in 3 yrs, interest rate is 6% on this loan | ||

| and no accrual has been made for the interest that is due | ||

The information and trial balances were as given. Could you do my adjusted entries? Thank you!

ewey, Cheetum, & Howe, Unadjusted Trial Balance at December 31, 2018 Debit Credit 3,515 8,400 20,800 2,000 6,000 3,600 8,000 35,000 6,600 76,000 Dewey, Cheetum, & Howe, LLP Adjusted Trial Balance at December 31, 2017 Debit Credit 7,040 5,000 8,000 4,000 1,000 4,000 20,000 6,600 20,000 5,000 9,000 6,000 6,800 1,200 800 9,100 2,400 14,400 5,000 25,000 7,740 9,000 10,000 20,400 Account Name Cash Marketable securities Accounts Receivable Allowance for Doubtful Accounts Inventory Prepaids Land Building Accum Depr - Bldg Equipment Accum Depr - Equip Patents Long-term investments Accounts Payable Income Taxes Payable Salaries Payable Deferred Revenue Working Capital Line of Credit Current Portion of LTD Long-term Debt, net Common Stock, $1 Par Paid in Capital Retained earnings Dividends Treasurey Stock Sales Revenue Cost Goods sold Raw Material Direct Labor Manufacturing Overhead Various Overhead Expenses Depreciation - Bldg Depreciation - Equip Operating Expenses Various Operating Expense Depreciation - Bldg Depreciation - Equip Interest and Dividend Income Interest Expense Gain on Sale of Long Term Investments Loss of Sale of Equipment Unrealized Gain on Mkt Securities Income Tax Expense Account Name Cash Marketable securities Accounts Receivable Inventory Prepaids Land Building Accum Depr - Bldg Equipment Accum Depr - Equip Patents Long-term investments Accounts Payable Income Taxes Payable Salaries Payable Working Capital Line of Credit Current Portion of LTD Long-term Debt, net Common Stock, $1 Par Paid in Capital Retained earnings Dividends Treasurey Stock Sales Revenue Cost Goods sold Raw Material Direct Labor Manufacturing Overhead Various Overhead Expenses Depreciation - Bldg Depreciation - Equip Operating Expenses Various Operating Expense Depreciation - Bldg Depreciation - Equip Interest and Dividend Income Interest Expense Gain on Sale of Long Term Investments Loss of Sale of Equipment Unrealized Gain on Mkt Securities Income tax Expense 3,600 6,000 12,000 2,400 33,600 10,000 40,000 7,740 4,000 6,000 80,000 6,000 12,000 4,000 19,440 400 785 5,000 600 3,400 Total 84,040 84,040 Total 233,140 233,140 ewey, Cheetum, & Howe, Unadjusted Trial Balance at December 31, 2018 Debit Credit 3,515 8,400 20,800 2,000 6,000 3,600 8,000 35,000 6,600 76,000 Dewey, Cheetum, & Howe, LLP Adjusted Trial Balance at December 31, 2017 Debit Credit 7,040 5,000 8,000 4,000 1,000 4,000 20,000 6,600 20,000 5,000 9,000 6,000 6,800 1,200 800 9,100 2,400 14,400 5,000 25,000 7,740 9,000 10,000 20,400 Account Name Cash Marketable securities Accounts Receivable Allowance for Doubtful Accounts Inventory Prepaids Land Building Accum Depr - Bldg Equipment Accum Depr - Equip Patents Long-term investments Accounts Payable Income Taxes Payable Salaries Payable Deferred Revenue Working Capital Line of Credit Current Portion of LTD Long-term Debt, net Common Stock, $1 Par Paid in Capital Retained earnings Dividends Treasurey Stock Sales Revenue Cost Goods sold Raw Material Direct Labor Manufacturing Overhead Various Overhead Expenses Depreciation - Bldg Depreciation - Equip Operating Expenses Various Operating Expense Depreciation - Bldg Depreciation - Equip Interest and Dividend Income Interest Expense Gain on Sale of Long Term Investments Loss of Sale of Equipment Unrealized Gain on Mkt Securities Income Tax Expense Account Name Cash Marketable securities Accounts Receivable Inventory Prepaids Land Building Accum Depr - Bldg Equipment Accum Depr - Equip Patents Long-term investments Accounts Payable Income Taxes Payable Salaries Payable Working Capital Line of Credit Current Portion of LTD Long-term Debt, net Common Stock, $1 Par Paid in Capital Retained earnings Dividends Treasurey Stock Sales Revenue Cost Goods sold Raw Material Direct Labor Manufacturing Overhead Various Overhead Expenses Depreciation - Bldg Depreciation - Equip Operating Expenses Various Operating Expense Depreciation - Bldg Depreciation - Equip Interest and Dividend Income Interest Expense Gain on Sale of Long Term Investments Loss of Sale of Equipment Unrealized Gain on Mkt Securities Income tax Expense 3,600 6,000 12,000 2,400 33,600 10,000 40,000 7,740 4,000 6,000 80,000 6,000 12,000 4,000 19,440 400 785 5,000 600 3,400 Total 84,040 84,040 Total 233,140 233,140Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Issues In Management Accounting

Authors: Trevor Hopper, Robert W. Scapens, Deryl Northcott

3rd Edition

0273702572, 978-0273702573