Question

Instructions Determine the cost of the inventory on December 31, 20Y7, by the first-in, first-out method. Present data in columnar form, using the following headings:

Instructions

Determine the cost of the inventory on December 31, 20Y7, by the first-in, first-out method. Present data in columnar form, using the following headings:

| Model | Quantity | Unit Cost | Total Cost |

If the inventory of a particular model comprises one entire purchase plus a portion of another purchase acquired at a different unit cost, use a separate line for each purchase.

1. Determine the cost of the inventory on December 31, 20Y7, by the last-in (LIFO), first-out (FIFO) method, following the procedures indicated in (1).

2. Determine the cost of the inventory on December 31, 20Y7, by the average cost method, using the columnar headings indicated in (1).

3. Discuss which method (FIFO or LIFO) would be preferred for income tax purposes in periods of (a) rising prices and (b) declining prices.

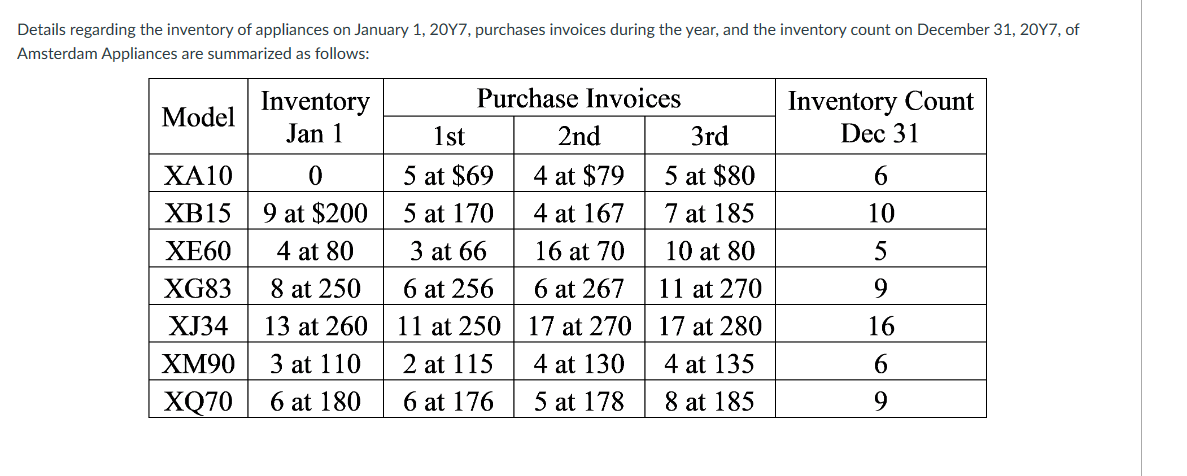

Details regarding the inventory of appliances on January 1, 20Y7, purchases invoices during the year, and the inventory count on December 31,20Y7, of Amsterdam Appliances are summarized as follows: Details regarding the inventory of appliances on January 1, 20Y7, purchases invoices during the year, and the inventory count on December 31,20Y7, of Amsterdam Appliances are summarized as follows

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started