Answered step by step

Verified Expert Solution

Question

1 Approved Answer

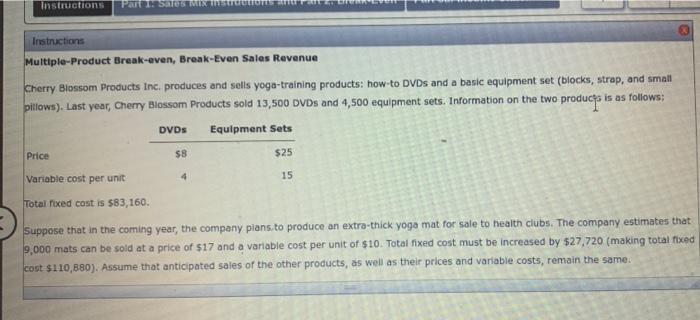

Instructions Par STMIX SI Instructions Multiple-Product Break-even, Break-Even Sales Revenue Cherry Blossom Products Inc. produces and sells yoga-training products: how to DVDs and a basic

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

De Gruyter Handbook Of Entrepreneurial Finance

Authors: David Lingelbach

1st Edition

3110726750,3110726351