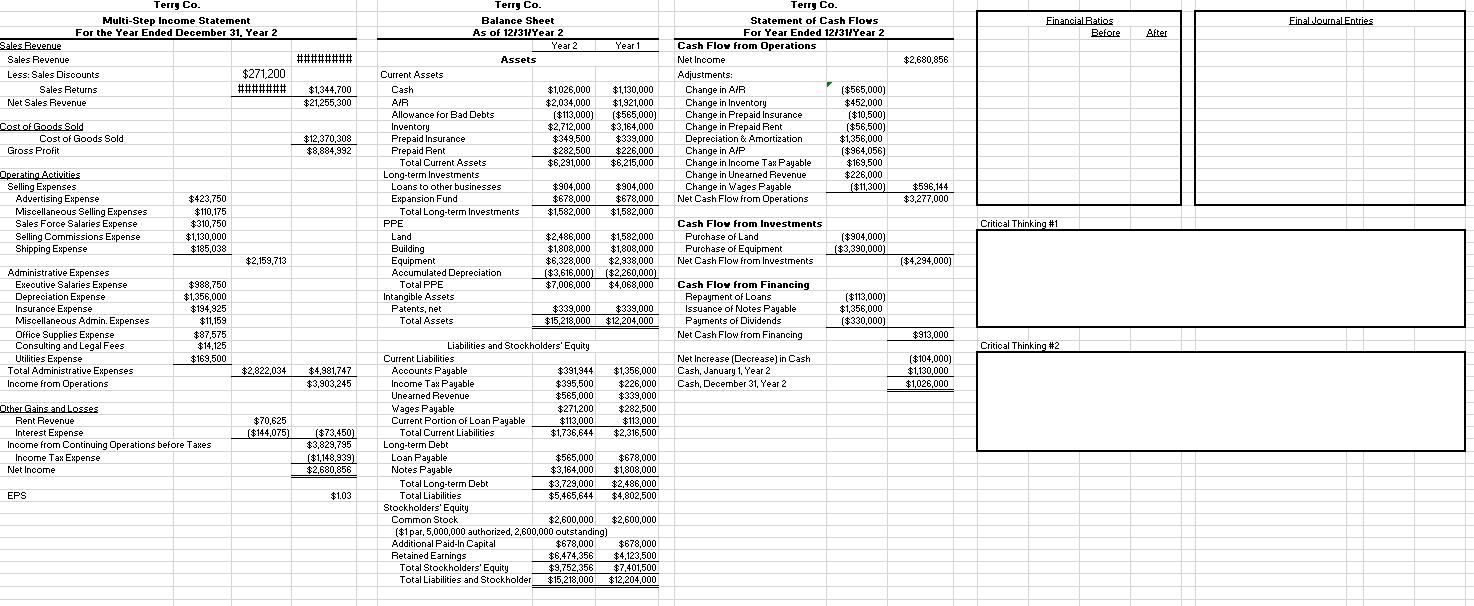

Intermediate 1 FSR Project Part #1: Inventory Basics Goal: To practice correcting the financial statements for an inventory calculation error. (See Topic Guides A 13, 14, 37, 38). Information: Burkett's management is afraid that an error was made when calculating COGS. Most of the calculations have already been checked by the auditors, but management still thinks that one inventory item has not been correctly recorded. They would like you to go back through the inventory calculations for that item to correct any possible mistakes. Currently they show that 9,600 units of item TC178, purchased for $9 each, were on hand at the beginning of the year, that $817,000 worth of TC178 was purchased during the year, that discounts of $7,600 were earned by making early payments on these purchases, and that $6,800 worth of returns were made during the year. The records show that only 8,600 units of the beginning TC178 inventory remained at the end of the year. Burkett uses the perpetual LIFO system for calculating inventory. Their inventory transactions for item TC178 for the period are as follows: (NOTE that the vendor provides free shipping on all units of TC178) At the beginning of the period, 9,600 units of TC178, purchased for $9.00 each, were on hand. . On Jan 15, an additional 29,000 units were purchased for $10.00 each. On February 28, 26,000 units were sold. . On March 14, an additional 15,000 units were purchased for $12.00 each. On March 20, a 3.0% cash discount was earned by paying for the March 14 purchase early. . On March 30, 17,000 units were sold. . On July 30,5,800 units were sold. . On August 20, an additional 26,000 units were purchased for $15.00 each. . On September 2, 12,000 units were sold. . On December 1, 10,400 units were sold. Burkett's management would like to know the effect of the sale on the following ratios: Inventory Turnover (COGS / average total inventory) . Current Ratio ROA Assignment: Calculations 1. Calculate each of the three (3) ratios before you make any adjustments. 2. Make the appropriate journal entries, if any, to correct the reported values of item TC178 (including any necessary changes to income tax expense). 3. Make any necessary changes to the financial statements, 4. Calculate the three (3) ratios after you make any adjustments. Critical Thinking 5. What do you think the investors' reaction will be to the adjustment of inventory? In other words, based on your changes to the financial statements and the change in the ratios, do you think investors will be happy with the restatement? Why or why not? 6. Who might be affected if the management team decided not to correct this error? Burkett's COO has repeatedly argued that no adjustment should be made to the current numbers. After all, she suggested, everything would be sold in the next period anyway. Why worry investors over something that is so unimportant? Defend your answer. Hints: 1. Start out by calculating Burkett's COGS on TC178 given the original information. The best way to do this is to set up a formal COGS calculation like the one we did in the Income Statement in Burkett #2. The formal calculation for one product would look just like the COGS section of the income statement, but it would only include the values for the one product 2. Use the perpetual inventory method to find out what purchases, purchase discounts, and COGS should be for TC178 using a formal perpetual inventory table. Once you have those numbers, set up another formal COGS calculation like the one you made for the original information using the new information. 3. Compare the new COGS calculation to the old one. The differences between the two sets of calculations are the changes that you need to record in your journal entry. 4. When making your journal entry, keep in mind that Burkett has a perpetual inventory system. This means the company doesn't have a 'purchase returns' or a 'purchase discount' account. Instead, everything will be done using the inventory account. Your final entry, then, should change only three accounts: COGS, Inventory, and A/P. You can get the changes to COGS and Inventory from the differences in your COGS equations (old vs. new). You will use A/P as the plug figure. Why? Well, to explain that, we have to go back to what the original journal entries look like for a company that uses the perpetual inventory system. When we buy inventory in a perpetual system, we debit inventory and credit A/P. When we pay for inventory, we debit A/P and credit cash. If we get a discount or make a return, we debit A/P and credit Inventory. That means that any mistake in recording purchases, returns, or discounts would cause a mistake in both the Inventory account AND the A/P account. When we sell inventory, we would debit COGS and credit Inventory, so mistakes in recording sales would cause a mistake in both Inventory AND COGS. So, in order to correct for all of Burkett's mistakes, we need to adjust all three of those accounts: Inventory, COGS, and A/P. Financial Ratios Before Final Journal Entries After Terry Co. Multi-Step Income Statement For the Year Ended December 31, Year 2 Sales Revenue Sales Revenue Less: Sales Discounts $271,200 Sales Returns ####### Net Sales Revenue ######## $2,680,856 $1,344,700 $21,255,300 Terry Co. Statement of Cash Flows For Year Ended 12/31/Year 2 Cash Flow from Operations Net Income Adjustments: Change in AIR ($565,000) Change in Inventory $452,000 Change in Prepaid Insurance ($10,500) Change in Prepaid Rent ($56,500) Depreciation & Amortization $1,356,000 Change in AIP ($964,056) Change in Income Tax Payable $169,500 Change in Unearned Revenue $226,000 Change in Wages Payable ($11,300) Net Cash Flow from Operations Cost of Goods Sold Cost of Goods Sold Gross Profit Terry Co. Balance Sheet As of 12/31/Year 2 Year 2 Year 1 Assets Current Assets Cash $1,026,000 $1,130,000 AIR $2,034,000 $1,921,000 Allowance for Bad Debts ($113,000) ($565,000) Inventory $2.712,000 $3,164,000 Prepaid Insurance $349,500 $339,000 Prepaid Rent $282,500 $226,000 Total Current Assets $6,291,000 $6,215,000 Long-term Investments Loans to other businesses $904,000 $904,000 Expansion Fund $678,000 $678,000 Total Long-term Investments $1,582,000 $1,582,000 PPE Land $2,486,000 $1,582,000 Building $1,808,000 $1,808,000 Equipment $6,328,000 $2,938,000 Accumulated Depreciation ($3,616,000) ($2,260,000) Total PPE $7,006,000 $4,068,000 Intangible Assets Patents, net $339,000 $339,000 Total Assets $15,218,000 $12,204,000 $12,370,308 $8,884,992 $596,144 $3,277,000 Operating Activities Selling Expenses Advertising Expense Miscellaneous Selling Expenses Sales Force Salaries Expense Selling Commissions Expense Shipping Expense $423.750 $110,175 $310.750 $1,130,000 $185,038 Critical Thinking #1 Cash Flow from Investments Purchase of Land Purchase of Equipment Net Cash Flow from Investments ($904,000) ($3,390,000) $2,159,713 ($4,294,000) Administrative Expenses Executive Salaries Expense Depreciation Expense Insurance Expense Miscellaneous Admin. Expenses Office Supplies Expense Consulting and Legal Fees Utilities Expense Total Administrative Expenses Income from Operations $988,750 $1,356,000 $194.925 $11,159 $87,575 $14,125 $169,500 Cash Flow from Financing Repayment of Loans Issuance of Notes Payable Payments of Dividends Net Cash Flow from Financing ($113,000) $1,356,000 ($330,000) $913,000 Critical Thinking #2 $2,822,034 $4,981,747 $3,903,245 Net Increase (Decrease) in Cash Cash, January 1, Year 2 Cash, December 31, Year 2 ($104,000) $1,130,000 $1,026,000 $70,625 ($144,075) Other Gains and Losses Rent Revenue Interest Expense Income from Continuing Operations before Taxes Income Tax Expense Net Income ($73,450) $3,829,795 ($1,148,939) $2,680,856 Liabilities and Stockholders' Equity Current Liabilities Accounts Payable $391,944 $1,356,000 Income Tax Payable $395,500 $226,000 Unearned Revenue $565,000 $339,000 $ Wages Payable $271,200 $282,500 Current Portion of Loan Payable $113,000 $113,000 Total Current Liabilities $1,736,644 $2,316,500 Long-term Debt Loan Payable $565,000 $678,000 Notes Payable $3,164,000 $1,808,000 Total Long-term Debt $3,729,000 $2,486,000 Total Liabilities $5,465,644 $4,802,500 Stockholders' Equity Common Stock $2,600,000 $2,600,000 ($1 par, 5,000,000 authorized, 2,600,000 outstanding) Additional Paid-In Capital $678,000 $678,000 Retained Earnings $6,474,356 $4,123,500 Total Stockholders' Equity $9,752,356 $7,401,500 Total Liabilities and Stockholder $15,218,000 $12,204,000 EPS $1.03