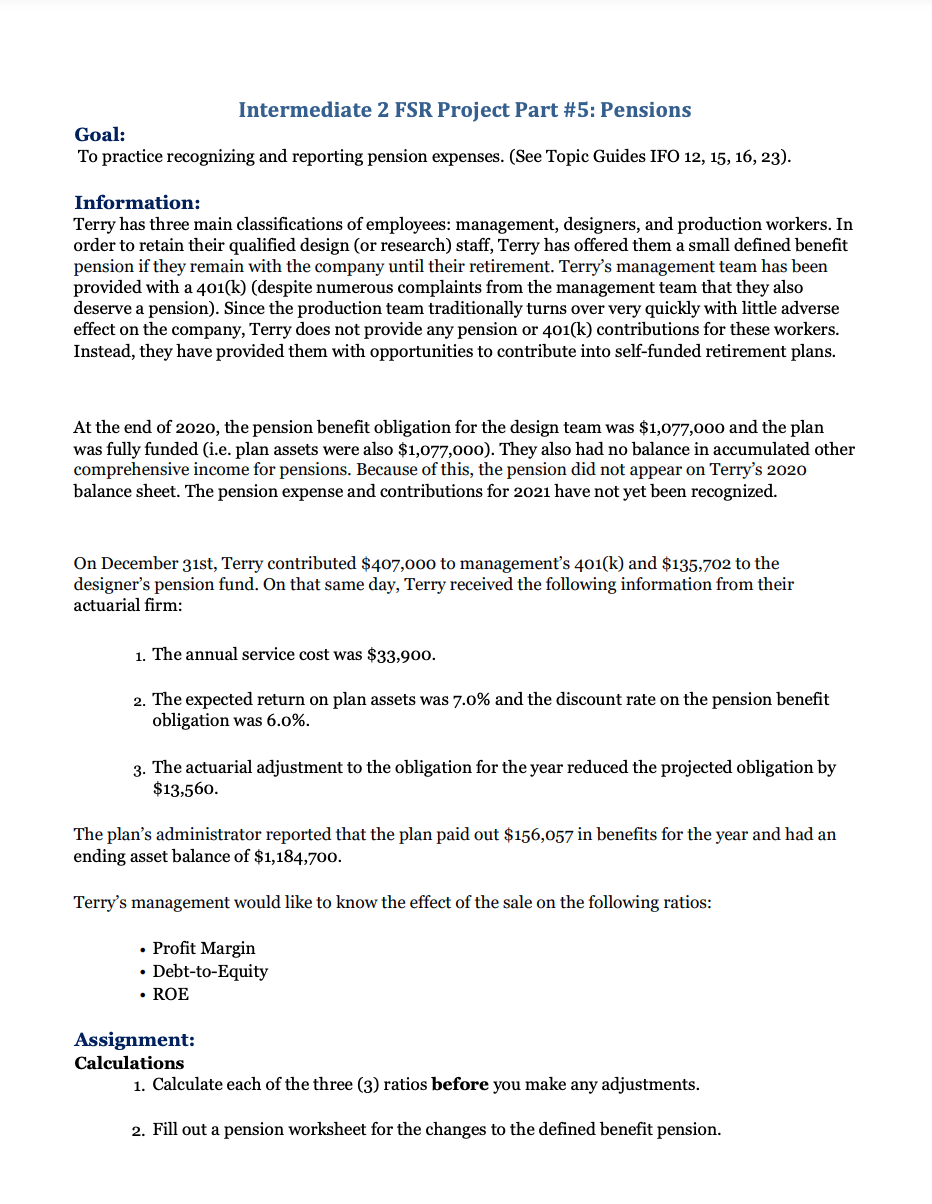

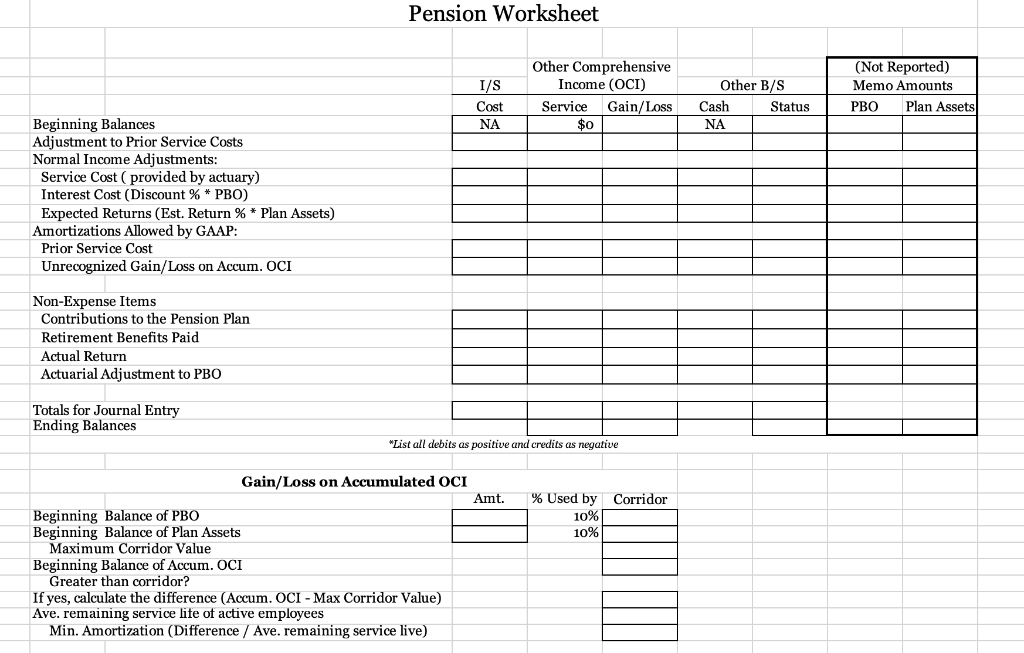

Intermediate 2 FSR Project Part #5: Pensions Goal: To practice recognizing and reporting pension expenses. (See Topic Guides IFO 12, 15, 16, 23). Information: Terry has three main classifications of employees: management, designers, and production workers. In order to retain their qualified design (or research) staff, Terry has offered them a small defined benefit pension if they remain with the company until their retirement. Terry's management team has been provided with a 401(k) (despite numerous complaints from the management team that they also deserve a pension). Since the production team traditionally turns over very quickly with little adverse effect on the company, Terry does not provide any pension or 401(k) contributions for these workers. Instead, they have provided them with opportunities to contribute into self-funded retirement plans. At the end of 2020, the pension benefit obligation for the design team was $1,077,000 and the plan was fully funded (i.e. plan assets were also $1,077,000). They also had no balance in accumulated other comprehensive income for pensions. Because of this, the pension did not appear on Terry's 2020 balance sheet. The pension expense and contributions for 2021 have not yet been recognized. On December 31st, Terry contributed $407,000 to management's 401(k) and $135,702 to the designer's pension fund. On that same day, Terry received the following information from their actuarial firm: 1. The annual service cost was $33,900. 2. The expected return on plan assets was 7.0% and the discount rate on the pension benefit obligation was 6.0%. 3. The actuarial adjustment to the obligation for the year reduced the projected obligation by $13,560. The plan's administrator reported that the plan paid out $156,057 in benefits for the year and had an ending asset balance of $1,184,700. Terry's management would like to know the effect of the sale on the following ratios: . Profit Margin Debt-to-Equity ROE Assignment: Calculations 1. Calculate each of the three (3) ratios before you make any adjustments. 2. Fill out a pension worksheet for the changes to the defined benefit pension. 3. Make the appropriate journal entries, if any, to account for the pension costs (including any necessary changes to income tax expense). Assume that compensation for the design team is recorded as part of R&D Expense. 4. Make any necessary changes to the financial statements. Please see the hints about the special adjustment to the Statement of Cash Flows. 5. Calculate the three (3) ratios after you make any adjustments. Critical Thinking 6. What do you think Terry's creditors' (i.e. bank and bond holder) reaction will be to the exchange? In other words, based on your changes to the financial statements and the change in the ratios, do you think the creditors will be happy with the exchange? Why or why not? 7. How do you think Terry's board should respond to management's insistence that they also deserve a defined benefit pension? Write your answer in the form of a short email that the board could send to the management team. Hints: 1. A pension worksheet similar to the one we used in class is available on our class website. 2. Under the new GAAP rules, you will need to add one line to your I/S (below Income from Operations). You will also need to add one line to your B/S. Please note that a net pension liability is classified as a long-term liability and a net pension asset is classified as a long- term investment. Also, companies typically combine all of their accumulated other comprehensive income accounts into one line item at the bottom of the B/S. 3. The Statement of Cash Flows treatment is also a little different for pensions. Because we don't use the change in other comprehensive income accounts on the Statement of Cash Flows, you have to make a manual adjustment. If the cash contribution is different from the pension cost recognized, then we add a line called Pension Plan Contributions. This value is calculated as the total pension cost minus the cash contributed to the pension. Pension Worksheet I/S Cost NA Other Comprehensive Income (OCI) Service Gain/Loss $0 Other B/S Cash Status NA (Not Reported) Memo Amounts PBO Plan Assets Beginning Balances Adjustment to Prior Service Costs Normal Income Adjustments: Service Cost (provided by actuary) Interest Cost (Discount % * PBO) Expected Returns (Est. Return % * Plan Assets) Amortizations Allowed by GAAP: Prior Service Cost Unrecognized Gain/Loss on Accum. OCI Non-Expense Items Contributions to the Pension Plan Retirement Benefits Paid Actual Return Actuarial Adjustment to PBO Totals for Journal Entry Ending Balances "List all debits as positive and credits as negative % Used by Corridor 10% 10% Gain/Loss on Accumulated OCI Amt. Beginning Balance of PBO Beginning Balance of Plan Assets Maximum Corridor Value Beginning Balance of Accum. OCI Greater than corridor? If yes, calculate the difference (Accum. OCI - Max Corridor Value) Ave. remaining service life of active employees Min. Amortization (Difference / Ave. remaining service live) Multi-Step Income Statement For the Year Ended December 31, 2021 Sales Revenue Sales Revenue Less: Sales Discounts $248,600 Sales Returns $1,977,500 Net Sales Revenue $23,257,200 $2,226, 100 $21,031,100 Cost of Goods Sold Cost of Goods Sold Gross Profit 12,991,428 $8,039,672 $444,950 $192,100 $110,175 $310,750 $1,130,000 $185,038 $2,373,013 Operating Activities Selling Expenses Advertising Expense Bad Debt Expense Miscellaneous Selling Expenses Sales Force Salaries Expense Selling Commissions Expense Shipping Expense Total Selling Expenses Administrative Expenses Executive Salaries Expense Depreciation & Amortization Expense Insurance Expense Miscellaneous Admin. Expenses Office Supplies Expense R&D Expense Utilities Expense Total Administrative Expenses Income from Operations $988,750 $678,000 $81,925 $11,159 $87,575 $339,000 $169,500 $2,355,909 $4,728,922 $3,310,750 Other Gains and Losses Rent Revenue Unrealized Loss on Expansion Fund Interest Expense Income from Continuing Operations before Taxes Income Tax Expense Net Income $70,625 ($10,400) ($156,726) ($96,501) $3,214,249 ($803,562) $2,410,687 Statement of Cash Flows $2,410,687 For the Year Ended December 31, 2021 Cash Flow from Operations Net Income Adjustments: Change in A/R ($565,000) Change in Inventory $1,046,000 Change in Prepaid Insurance $169,500 Change in Prepaid Utllities ($56,500) Depreciation & Amortization $678,000 Amoritization of Bond Premium ($870) Unrealized Loss on Expansion Fund $10,400 Change in A/P ($63,375) Change in Coupon Liability $21,200 Change in Income Tax Payable $572,337 Change in Interest Payable $13,521 Change in Unearned Revenue $71,000 Change in Wages Payable ($33,900) Net Cash Flow from Operations $1,862,313 $4,273,000 Cash Flow from Investments Purchase of Land Purchase of Equipment Net Cash Flow from Investments ($904,000) ($3,390,000) ($4,294,000) Cash Flow from Financing Repayment of Loans Purchase of Treasury Stock Issuance of Bonds Payable Issuance of Notes Payable Payments of Dividends Net Cash Flow from Financing ($113,000) (640,000) $607,244 $1,356,000 ($200,000) $1,010,244 Net Increase (Decrease) in Cash Cash, January 1, Year 3 Cash, December 31, Year 3 $989,244 $1,130,000 $2,119,244 Assets Current Assets Cash $2,119,244 $1,130,000 AIR $2,034,000 $1,921,000 Allowance for Bad Debts ($113,000) ($565,000) Inventory $2,118,000 $3,164,000 Prepaid Insurance $169,500 $339,000 Prepaid Utilities $282,500 $226,000 Total Current Assets $6,610,244 $6,215,000 Long-term Investments Loans to other businesses $904,000 $904,000 Expansion Fund $532,000 $542,400 Total Long-term Investments $1,436,000 $1,446,400 PPE Land $2,486,000 $1,582,000 Building $1,808,000 $1,808,000 Equipment $6,328,000 $2,938,000 Accumulated Depreciation ($2,938,000) ($2,260,000) Total PPE $7,684,000 $4,068,000 Intangible Assets Patents, net $339,000 $339,000 Total Assets $16,069,244 $12,068,400 $ 14,068,822 Liabilities and Stockholders' Equity Current Liabilities Dividends Payable $ 148,500 Accounts Payable $1,292,625 $1,356,000 Coupon Liability $21,200 $0 Income Tax Payable $798,337 $226,000 Interest Payable $13,521 Unearned Revenue $410,000 $339,000 Wages Payable $248,600 $282,500 Current Portion of Loan Payable $113,000 $113,000 Total Current Liabilities $ 3,045,783 $2,316,500 Long-term Debt Loan Payable $1,243,000 $1,356,000 Bonds Payable, Net $606,374 $0 Notes Payable $3,164,000 $1,808,000 Total Long-term Debt $5,013,374 $3,164,000 Total Liabilities $8,059,157 $5,480,500 Stockholders' Equity Common stock $900,000 $900,000 ($1 par, 1,600,000 authorized, 900,000 issued, and 820,000 outstanding) Additional Paid-In capital $678,000 $678,000 Treasury Stock (640,000) Retained Earnings $7,483,747 $5,421,560 Accumulated OCI ($411,660) ($411,660) Total Stockholders' Equity $8,010,087 $6,587,900 Total Liabilities and Stockholder's Equity $16,069,244 $12,068,400 Intermediate 2 FSR Project Part #5: Pensions Goal: To practice recognizing and reporting pension expenses. (See Topic Guides IFO 12, 15, 16, 23). Information: Terry has three main classifications of employees: management, designers, and production workers. In order to retain their qualified design (or research) staff, Terry has offered them a small defined benefit pension if they remain with the company until their retirement. Terry's management team has been provided with a 401(k) (despite numerous complaints from the management team that they also deserve a pension). Since the production team traditionally turns over very quickly with little adverse effect on the company, Terry does not provide any pension or 401(k) contributions for these workers. Instead, they have provided them with opportunities to contribute into self-funded retirement plans. At the end of 2020, the pension benefit obligation for the design team was $1,077,000 and the plan was fully funded (i.e. plan assets were also $1,077,000). They also had no balance in accumulated other comprehensive income for pensions. Because of this, the pension did not appear on Terry's 2020 balance sheet. The pension expense and contributions for 2021 have not yet been recognized. On December 31st, Terry contributed $407,000 to management's 401(k) and $135,702 to the designer's pension fund. On that same day, Terry received the following information from their actuarial firm: 1. The annual service cost was $33,900. 2. The expected return on plan assets was 7.0% and the discount rate on the pension benefit obligation was 6.0%. 3. The actuarial adjustment to the obligation for the year reduced the projected obligation by $13,560. The plan's administrator reported that the plan paid out $156,057 in benefits for the year and had an ending asset balance of $1,184,700. Terry's management would like to know the effect of the sale on the following ratios: . Profit Margin Debt-to-Equity ROE Assignment: Calculations 1. Calculate each of the three (3) ratios before you make any adjustments. 2. Fill out a pension worksheet for the changes to the defined benefit pension. 3. Make the appropriate journal entries, if any, to account for the pension costs (including any necessary changes to income tax expense). Assume that compensation for the design team is recorded as part of R&D Expense. 4. Make any necessary changes to the financial statements. Please see the hints about the special adjustment to the Statement of Cash Flows. 5. Calculate the three (3) ratios after you make any adjustments. Critical Thinking 6. What do you think Terry's creditors' (i.e. bank and bond holder) reaction will be to the exchange? In other words, based on your changes to the financial statements and the change in the ratios, do you think the creditors will be happy with the exchange? Why or why not? 7. How do you think Terry's board should respond to management's insistence that they also deserve a defined benefit pension? Write your answer in the form of a short email that the board could send to the management team. Hints: 1. A pension worksheet similar to the one we used in class is available on our class website. 2. Under the new GAAP rules, you will need to add one line to your I/S (below Income from Operations). You will also need to add one line to your B/S. Please note that a net pension liability is classified as a long-term liability and a net pension asset is classified as a long- term investment. Also, companies typically combine all of their accumulated other comprehensive income accounts into one line item at the bottom of the B/S. 3. The Statement of Cash Flows treatment is also a little different for pensions. Because we don't use the change in other comprehensive income accounts on the Statement of Cash Flows, you have to make a manual adjustment. If the cash contribution is different from the pension cost recognized, then we add a line called Pension Plan Contributions. This value is calculated as the total pension cost minus the cash contributed to the pension. Pension Worksheet I/S Cost NA Other Comprehensive Income (OCI) Service Gain/Loss $0 Other B/S Cash Status NA (Not Reported) Memo Amounts PBO Plan Assets Beginning Balances Adjustment to Prior Service Costs Normal Income Adjustments: Service Cost (provided by actuary) Interest Cost (Discount % * PBO) Expected Returns (Est. Return % * Plan Assets) Amortizations Allowed by GAAP: Prior Service Cost Unrecognized Gain/Loss on Accum. OCI Non-Expense Items Contributions to the Pension Plan Retirement Benefits Paid Actual Return Actuarial Adjustment to PBO Totals for Journal Entry Ending Balances "List all debits as positive and credits as negative % Used by Corridor 10% 10% Gain/Loss on Accumulated OCI Amt. Beginning Balance of PBO Beginning Balance of Plan Assets Maximum Corridor Value Beginning Balance of Accum. OCI Greater than corridor? If yes, calculate the difference (Accum. OCI - Max Corridor Value) Ave. remaining service life of active employees Min. Amortization (Difference / Ave. remaining service live) Multi-Step Income Statement For the Year Ended December 31, 2021 Sales Revenue Sales Revenue Less: Sales Discounts $248,600 Sales Returns $1,977,500 Net Sales Revenue $23,257,200 $2,226, 100 $21,031,100 Cost of Goods Sold Cost of Goods Sold Gross Profit 12,991,428 $8,039,672 $444,950 $192,100 $110,175 $310,750 $1,130,000 $185,038 $2,373,013 Operating Activities Selling Expenses Advertising Expense Bad Debt Expense Miscellaneous Selling Expenses Sales Force Salaries Expense Selling Commissions Expense Shipping Expense Total Selling Expenses Administrative Expenses Executive Salaries Expense Depreciation & Amortization Expense Insurance Expense Miscellaneous Admin. Expenses Office Supplies Expense R&D Expense Utilities Expense Total Administrative Expenses Income from Operations $988,750 $678,000 $81,925 $11,159 $87,575 $339,000 $169,500 $2,355,909 $4,728,922 $3,310,750 Other Gains and Losses Rent Revenue Unrealized Loss on Expansion Fund Interest Expense Income from Continuing Operations before Taxes Income Tax Expense Net Income $70,625 ($10,400) ($156,726) ($96,501) $3,214,249 ($803,562) $2,410,687 Statement of Cash Flows $2,410,687 For the Year Ended December 31, 2021 Cash Flow from Operations Net Income Adjustments: Change in A/R ($565,000) Change in Inventory $1,046,000 Change in Prepaid Insurance $169,500 Change in Prepaid Utllities ($56,500) Depreciation & Amortization $678,000 Amoritization of Bond Premium ($870) Unrealized Loss on Expansion Fund $10,400 Change in A/P ($63,375) Change in Coupon Liability $21,200 Change in Income Tax Payable $572,337 Change in Interest Payable $13,521 Change in Unearned Revenue $71,000 Change in Wages Payable ($33,900) Net Cash Flow from Operations $1,862,313 $4,273,000 Cash Flow from Investments Purchase of Land Purchase of Equipment Net Cash Flow from Investments ($904,000) ($3,390,000) ($4,294,000) Cash Flow from Financing Repayment of Loans Purchase of Treasury Stock Issuance of Bonds Payable Issuance of Notes Payable Payments of Dividends Net Cash Flow from Financing ($113,000) (640,000) $607,244 $1,356,000 ($200,000) $1,010,244 Net Increase (Decrease) in Cash Cash, January 1, Year 3 Cash, December 31, Year 3 $989,244 $1,130,000 $2,119,244 Assets Current Assets Cash $2,119,244 $1,130,000 AIR $2,034,000 $1,921,000 Allowance for Bad Debts ($113,000) ($565,000) Inventory $2,118,000 $3,164,000 Prepaid Insurance $169,500 $339,000 Prepaid Utilities $282,500 $226,000 Total Current Assets $6,610,244 $6,215,000 Long-term Investments Loans to other businesses $904,000 $904,000 Expansion Fund $532,000 $542,400 Total Long-term Investments $1,436,000 $1,446,400 PPE Land $2,486,000 $1,582,000 Building $1,808,000 $1,808,000 Equipment $6,328,000 $2,938,000 Accumulated Depreciation ($2,938,000) ($2,260,000) Total PPE $7,684,000 $4,068,000 Intangible Assets Patents, net $339,000 $339,000 Total Assets $16,069,244 $12,068,400 $ 14,068,822 Liabilities and Stockholders' Equity Current Liabilities Dividends Payable $ 148,500 Accounts Payable $1,292,625 $1,356,000 Coupon Liability $21,200 $0 Income Tax Payable $798,337 $226,000 Interest Payable $13,521 Unearned Revenue $410,000 $339,000 Wages Payable $248,600 $282,500 Current Portion of Loan Payable $113,000 $113,000 Total Current Liabilities $ 3,045,783 $2,316,500 Long-term Debt Loan Payable $1,243,000 $1,356,000 Bonds Payable, Net $606,374 $0 Notes Payable $3,164,000 $1,808,000 Total Long-term Debt $5,013,374 $3,164,000 Total Liabilities $8,059,157 $5,480,500 Stockholders' Equity Common stock $900,000 $900,000 ($1 par, 1,600,000 authorized, 900,000 issued, and 820,000 outstanding) Additional Paid-In capital $678,000 $678,000 Treasury Stock (640,000) Retained Earnings $7,483,747 $5,421,560 Accumulated OCI ($411,660) ($411,660) Total Stockholders' Equity $8,010,087 $6,587,900 Total Liabilities and Stockholder's Equity $16,069,244 $12,068,400