Answered step by step

Verified Expert Solution

Question

1 Approved Answer

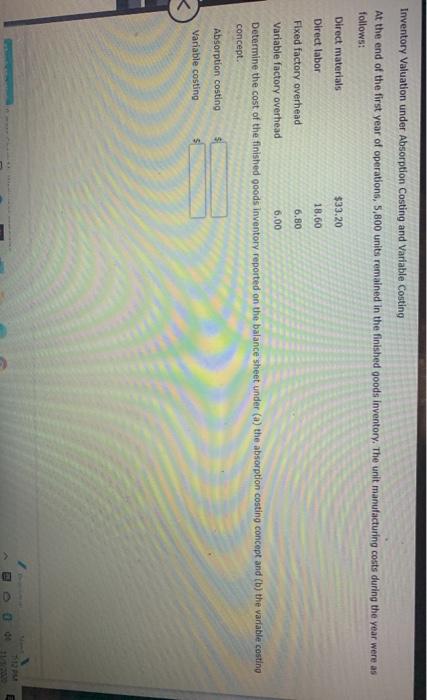

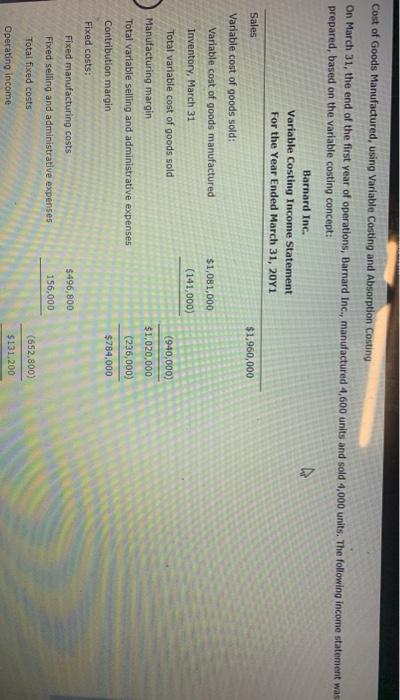

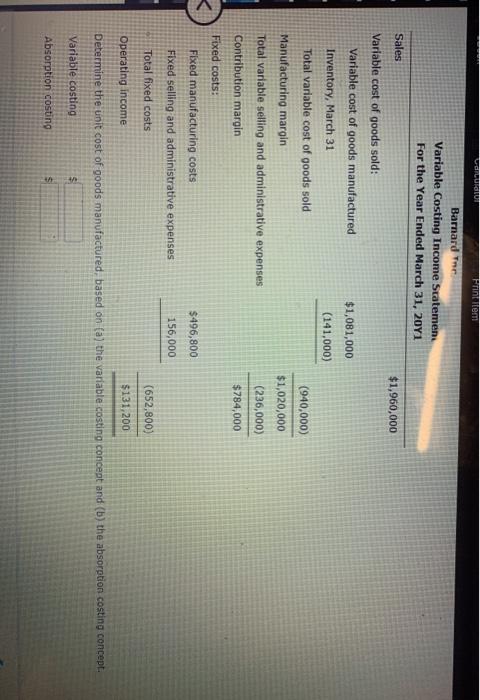

Inventory Valuation under Absorption Costing and Variable Costing At the end of the first year of operations, 5,800 units remained in the finished goods inventory.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sound Investing, Chapter 24 - The Auditors??? Opinion

Authors: Kate Mooney

2nd Edition

0071719466, 9780071719469