Answered step by step

Verified Expert Solution

Question

1 Approved Answer

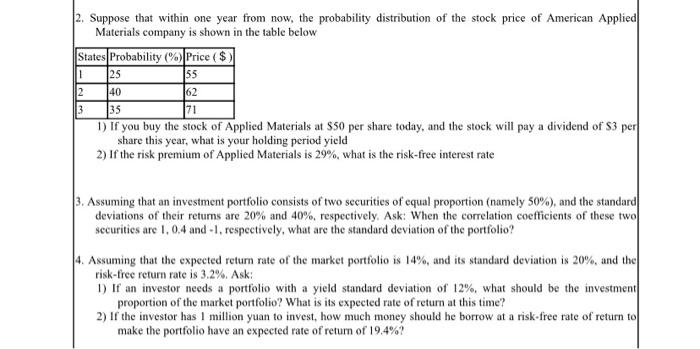

investments 2. Suppose that within one year from now, the probability distribution of the stock price of American Applied Materials company is shown in the

investments

2. Suppose that within one year from now, the probability distribution of the stock price of American Applied Materials company is shown in the table below 1) If you buy the stock of Applied Materials at $50 per share today, and the stock will pay a dividend of $3 per share this year, what is your holding period yield 2) If the risk premium of Applied Materials is 29%, what is the risk-free interest rate 3. Assuming that an investment portfolio consists of two securities of equal proportion (namely 50% ), and the standard deviations of their returns are 20% and 40%, respectively. Ask: When the correlation coefficients of these two securities are 1,0.4 and 1, respectively, what are the standard deviation of the portfolio? 4. Assuming that the expected return rate of the market portfolio is 14%, and its standard deviation is 20%, and the risk-free return rate is 3.2%. Ask: 1) If an investor needs a portfolio with a yield standard deviation of 12%, what should be the investment proportion of the market portfolio? What is its expected rate of return at this time? 2) If the investor has 1 million yuan to invest, how much money should he borrow at a risk-free rate of return to make the portfolio have an expected rate of return of 19.4% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Multinational Finance

Authors: Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman

1st Edition

0201844842, 978-0201844849