Question

Investors are risk neutral and we have the following binomial tree: A. Calculate the probability of every state in the next two years when rf

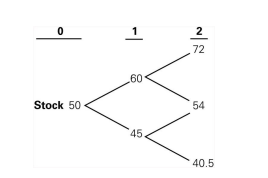

Investors are risk neutral and we have the following binomial tree:

A. Calculate the probability of every state in the next two years when rf = 3% B. Use these probabilities to calculate the price of a two-year call option on this stock with a strike price $60. C. Then, price a two-year European put option with the same strike price.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Fiscal Impact Handbook

Authors: David Listokin

1st Edition

1138535672, 978-1138535671