Question: Is the current performance measurement system for production personnel appropriate? If so, why? If not, what would you recommend for an alternative performance measurement system?

Is the current performance measurement system for production personnel appropriate? If so, why? If not, what would you recommend for an alternative performance measurement system?

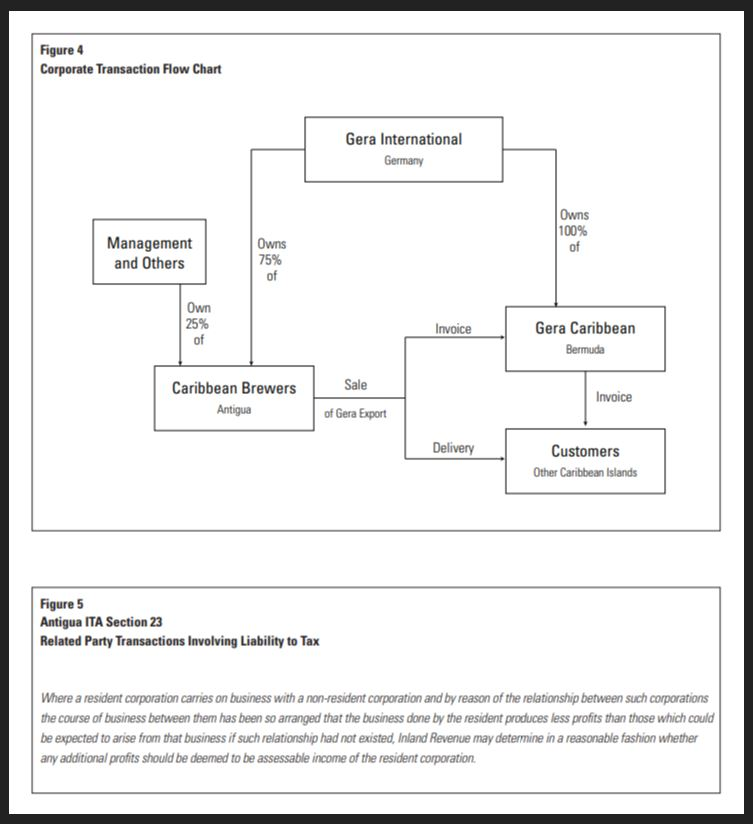

Given the wording in Figure 5 with respect to the taxation of related party transactions, to what extent is Caribbean Brewers vulnerable to tax reassessment??

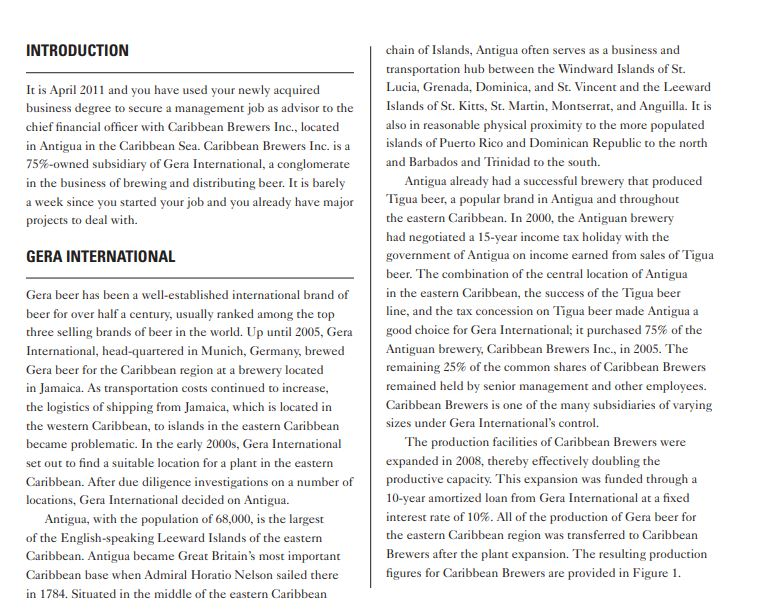

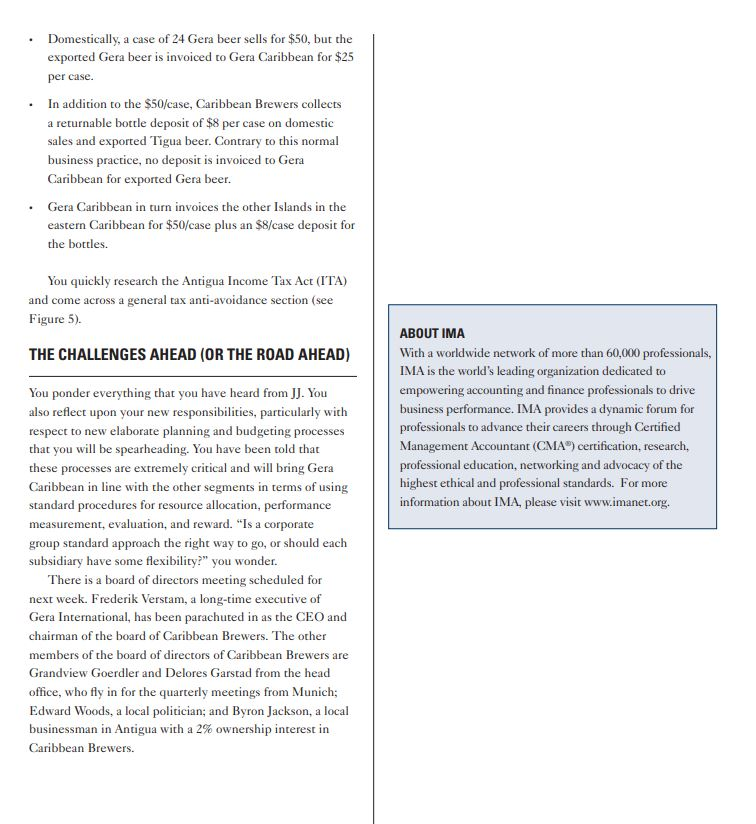

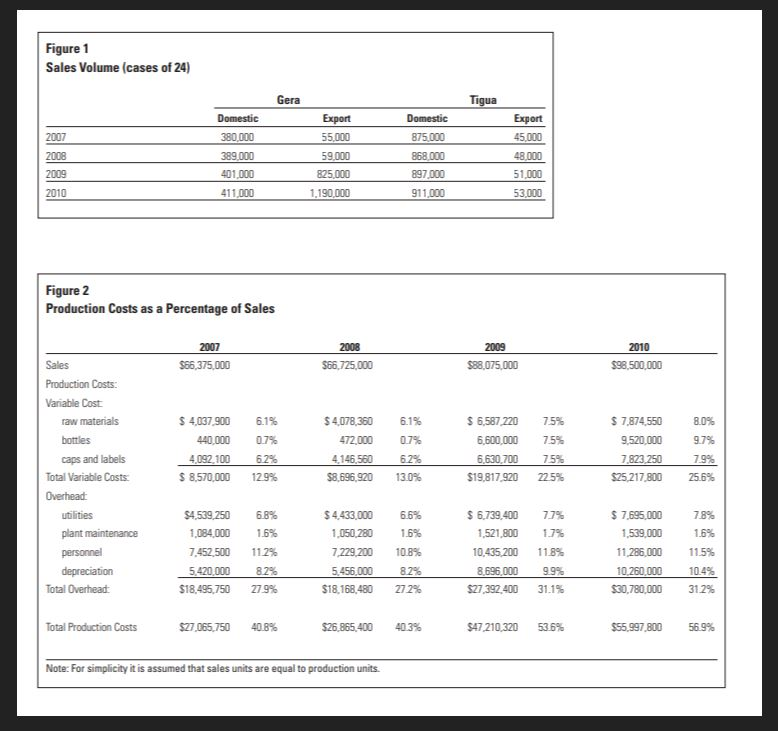

INTRODUCTION It is April 2011 and you have used your newly acquired business degree to secure a management job as advisor to the chief financial officer with Caribbean Brewers Inc., located in Antigua in the Caribbean Sea. Caribbean Brewers Inc. is a 75%-owned subsidiary of Gera International, a conglomerate in the business of brewing and distributing beer. It is barely a week since you started your job and you already have major projects to deal with. GERA INTERNATIONAL Gera beer has been a well-established international brand of beer for over half a century, usually ranked among the top three selling brands of beer in the world. Up until 2005, Gera International, head-quartered in Munich, Germany, brewed Gera beer for the Caribbean region at a brewery located in Jamaica. As transportation costs continued to increase, the logistics of shipping from Jamaica, which is located in the western Caribbean, to islands in the eastern Caribbean became problematic. In the early 2000s, Gera International set out to find a suitable location for a plant in the eastern Caribbean. After due diligence investigations on a number of locations, Gera International decided on Antigua. Antigua, with the population of 68,000, is the largest of the English-speaking Leeward Islands of the eastern Caribbean. Antigua became Great Britain's most important Caribbean base when Admiral Horatio Nelson sailed there in 1784. Situated in the middle of the eastern Caribbean chain of Islands, Antigua often serves as a business and transportation hub between the Windward Islands of St. Lucia, Grenada, Dominica, and St. Vincent and the Leeward Islands of St. Kitts, St. Martin, Montserrat, and Anguilla. It is also in reasonable physical proximity to the more populated islands of Puerto Rico and Dominican Republic to the north and Barbados and Trinidad to the south. Antigua already had a successful brewery that produced Tigua beer, a popular brand in Antigua and throughout the eastern Caribbean. In 2000, the Antiguan brewery had negotiated a 15-year income tax holiday with the government of Antigua on income earned from sales of Tigua beer. The combination of the central location of Antigua in the eastern Caribbean, the success of the Tigua beer line, and the tax concession on Tigua beer made Antigua a good choice for Gera International; it purchased 75% of the Antiguan brewery, Caribbean Brewers Inc., in 2005. The remaining 25% of the common shares of Caribbean Brewers remained held by senior management and other employees. Caribbean Brewers is one of the many subsidiaries of varying sizes under Gera International's control. The production facilities of Caribbean Brewers were expanded in 2008, thereby effectively doubling the productive capacity. This expansion was funded through a 10-year amortized loan from Gera International at a fixed interest rate of 10%. All of the production of Gera beer for the eastern Caribbean region was transferred to Caribbean Brewers after the plant expansion. The resulting production figures for Caribbean Brewers are provided in Figure 1. RECENT ISSUES Upon arrival in your new position, you discover that all is not rosy at Caribbean Brewers. On only your second day in the office, the production manager, Jason Joseph, affectionately known as JJ, comes into your office and shuts the door. JJ has been production manager for decades and has been heralded as a master brewer, having won multiple awards for Tigua beer in the late 1990s and early 2000s. It is clear during the meeting that JJ is unhappy and distressed. He explains that prior to Gera International's involvement in the brewery, things were better; JJ previously had a 25% ownership in Caribbean Brewers, which is now reduced to 8%. He had always received a salary of about $100,000 as the production manager, but had also benefited by a bonus and an annual dividend. Since Gera International became the majority shareholder, there have been no dividends. In addition, JJ's bonus, which is based on a combination of controlling average total production costs and quality control, has all but been eliminated since the plant expansion. With respect to production costs, JJ and other production personnel are eligible for a bonus provided that total production costs do not exceed 43% of sales. Figure 2 contains the format of the report that is used to assess production efficiency and bonus calculations. JJ explains that the production process for brewing beer has been fundamentally the same for decades, as outlined in Appendix 1. The first two steps, i.e., milling and mash tun, account for 50% of the total production overhead costs. Tigua beer has a longer and more time-intensive production process up to the stage where the wort is created; this results in the Tigua beer consuming 100% more overhead resources up to this stage compared to Gera beer. After the creation of the wort, the process and cost are the same regardless of the brand. The direct costs of the beer are not all that significant; 98% of the beer is water and the cost of the raw materials is only about $3 per case of 24. The costs of the bottle cap and label are as much as raw materials, about $3 per case. The cost of the bottles is $8 per case of 24; however, this is not normally treated as a cost because a deposit of $8 per case of 24 is collected for all returnable markets, which include all domestic markets and export of Tigua. Contrary to this normal business practice, no deposit is collected on the export market for Gera beer; as a result, the cost of the bottles pertaining to Gera beer exports are expensed. As a result of the decline in production efficiencies, as measured in Figure 2, JJ's bonus has suffered. JJ is adamant that the production facility is operating as efficiently as, if not more efficiently than, before the expansion, and is concerned that the cost allocations used in Figure 2 for production costs are penalizing his bonus. "Prior to the expansion, I focused on production cost per case. Gera International now holds us accountable for production cost as a percentage of sales - this has taken away control from the production people. I also don't understand why the exported Gera beer bottle costs are charged to our plant," JJ exclaimed in sheer frustration. He also explained that Gera International has on occasion complained about the quality of Gera beer exported to other Caribbean countries, thereby refusing to pay Caribbean Brewers for some shipments. JJ is adamant that the quality of the beer is consistent and desperately wants to be able to prove the allegations of poor quality as groundless. He is concerned that Gera International is making false allegations about the quality to justify not paying for some of the shipments. "I do not understand how head office can say that our quality is poor; I have not heard any complaints from our local customers of Gera beer. I have been in the business long enough to know when quality is bad; I am able to and usually do take corrective actions during the process itself before things go out of hand." Before leaving your office, JJ explains that he is very frustrated and is seriously considering leaving the company to be the master brewer and production manager of a brewery in Trinidad, a major competitor of Caribbean Brewers. This would be a major loss to the company. Later the same day, the head accountant provides you with a letter from the Inland Revenue Department (IRD) of Antigua (equivalent to IRS in the United States of America) explaining that tax auditors will be coming out next month to review the tax filings for the years ending December 31, 2008, 2009, and 2010. You investigate and find that in order to benefit from the tax exemption of Tigua beer, Caribbean Brewers prepares profitability statements along taxable and nontaxable product lines when filing the annual tax return. This allocation between the two product lines is provided in Figure 3. Caribbean Brewers is a tax resident of Antigua and thus subject to taxes of 30% of profits. As you begin preparing for the tax audit you find out the following: All export sales of Gera beer are made to Gera Caribbean, a wholly-owned subsidiary of Gera International, which is located in Bermuda, a tax-free jurisdiction. (See Figure 4 for a chart of the transactions.) For cost and logistical reasons, the exports are shipped directly to the Island where the beer will be sold in the eastern Caribbean while only the invoice is sent to Bermuda (see Figure 4). Domestically, a case of 24 Gera beer sells for $50, but the exported Gera beer is invoiced to Gera Caribbean for $25 per case. In addition to the $50/case, Caribbean Brewers collects a returnable bottle deposit of $8 per case on domestic sales and exported Tigua beer. Contrary to this normal business practice, no deposit is invoiced to Gera Caribbean for exported Gera beer. Gera Caribbean in turn invoices the other Islands in the eastern Caribbean for $50/case plus an $8/case deposit for the bottles. You quickly research the Antigua Income Tax Act (ITA) and come across a general tax anti-avoidance section (see Figure 5). THE CHALLENGES AHEAD (OR THE ROAD AHEAD) You ponder everything that you have heard from JJ. You also reflect upon your new responsibilities, particularly with respect to new elaborate planning and budgeting processes that you will be spearheading. You have been told that these processes are extremely critical and will bring Gera Caribbean in line with the other segments in terms of using standard procedures for resource allocation, performance measurement, evaluation, and reward. "Is a corporate group standard approach the right way to go, or should each subsidiary have some flexibility?" you wonder. There is a board of directors meeting scheduled for next week. Frederik Verstam, a long-time executive of Gera International, has been parachuted in as the CEO and chairman of the board of Caribbean Brewers. The other members of the board of directors of Caribbean Brewers are Grandview Goerdler and Delores Garstad from the head office, who fly in for the quarterly meetings from Munich; Edward Woods, a local politician; and Byron Jackson, a local businessman in Antigua with a 2% ownership interest in Caribbean Brewers. ABOUT IMA With a worldwide network of more than 60,000 professionals, IMA is the world's leading organization dedicated to empowering accounting and finance professionals to drive business performance. IMA provides a dynamic forum for professionals to advance their careers through Certified Management Accountant (CMA) certification, research, professional education, networking and advocacy of the highest ethical and professional standards. For more information about IMA, please visit www.imanet.org. Figure 1 Sales Volume (cases of 24) 2007 2008 2009 2010 Sales Production Costs: Variable Cost: Figure 2 Production Costs as a Percentage of Sales raw materials bottles caps and labels Total Variable Costs: Overhead: utilities plant maintenance personnel depreciation Total Overhead: Domestic 380,000 389,000 401,000 411,000 Total Production Costs 2007 $66,375,000 Gera $ 4,037,900 6.1% 440,000 0.7% 4,092,100 6.2% $ 8,570,000 12.9% $4,539,250 6.8% 1,084,000 1.6% 7,452,500 11.2% 5,420,000 8.2% $18,495,750 27.9% $27,065,750 40.8% Export 55,000 59,000 825,000 1,190,000 2008 $66,725,000 $4,078,360 6.1% 0.7% 472,000 4,146,560 6.2% $8,696,920 13.0% Domestic 875,000 868,000 897,000 911,000 $4,433,000 6.6% 1,050,280 1.6% 7,229,200 10.8% 5,456,000 8.2% $18,168,480 27.2% $26,865,400 Note: For simplicity it is assumed that sales units are equal to production units. 40.3% Tigua Export 45,000 48,000 51,000 53,000 2009 $88,075,000 $ 6,587,220 7.5% 6,600,000 7.5% 6,630,700 7.5% $19,817,920 22.5% $ 6,739,400 7.7% 1,521,800 1.7% 10,435,200 11.8% 8,696,000 9.9% $27,392,400 31.1% $47,210,320 53.6% 2010 $98,500,000 $ 7,874,550 9,520,000 7,823,250 $25,217,800 $ 7,695,000 1,539,000 11,286,000 10,260,000 $30,780,000 $55,997,800 8.0% 9.7% 7.9% 25.6% 7.8% 1.6% 11.5% 10.4% 31.2% 56.9% Figure 3 Allocation of Taxable and Non-taxable Streams 2008 Volume in cases of 24 Sales Production Costs Sales Costs Administrative Costs Interest Costs Net profit 2009 Volume in cases of 24 Sales Production Costs Sales Costs Administrative Costs Interest Net profit 2010 Volume in cases of 24 Sales Production Costs Sales Costs Administrative Costs Interest Net profit Total 1,364,000 $66,725,000 $26,865,400 4,670,750 4,003,500 543,000 $30,642,350 Total 2,174,000 $88,075,000 $47,210,320 5,284,500 4,844,125 3,257,000 $27,479,055 Total 2,565,000 $98,500,000 $55,997,800 5,614,500 5,220,500 2,932,000 $28,735,200 Notes: Sales price of Gera Exported beer is $25 while all others are $50 Total production costs allocated on the basis of volume (# of cases). Sales and Administrative and Interest expense allocated on the basis of sales dollars. Non-taxable Tigua 916,000 $45,800,000 $18,041,574 3,206,000 2,748,000 372,715 $21,431,712 Non-taxable Tigua 948,000 $47,400,000 $20,586,653 2,844,000 2,607,000 1,752,845 $19,609,502 Non-taxable Tigua 964,000 $48,200,000 $21,045,567 2,747,400 2,554,600 1,434,745 $20,417,688 Taxable - Gera 448,000 $20,925,000 $ 8,823,826 1,464,750 1,255,500 170,285 $ 9,210,638 Taxable - Gera 1,226,000 $40,675,000 $26,623,667 2,440,500 2,237,125 1,504,155 $7,869,553 Taxable - Gera 1,601,000 $50,300,000 $34,952,233 2,867,100 2,665,900 1,497,255 $ 8,317,512 Figure 4 Corporate Transaction Flow Chart Management and Others Own 25% of Owns 75% of Caribbean Brewers Antigua Figure 5 Antigua ITA Section 23 Related Party Transactions Involving Liability to Tax Gera International Germany Sale of Gera Export Invoice Delivery Owns 100% of Gera Caribbean Bermuda Invoice Customers Other Caribbean Islands Where a resident corporation carries on business with a non-resident corporation and by reason of the relationship between such corporations the course of business between them has been so arranged that the business done by the resident produces less profits than those which could be expected to arise from that business if such relationship had not existed, Inland Revenue may determine in a reasonable fashion whether any additional profits should be deemed to be assessable income of the resident corporation.

Step by Step Solution

3.37 Rating (169 Votes )

There are 3 Steps involved in it

1 The current production measurement system is inappropriate because it is not based on events that the production personnel have any control over For instance instead of looking at the production cos... View full answer

Get step-by-step solutions from verified subject matter experts