Answered step by step

Verified Expert Solution

Question

1 Approved Answer

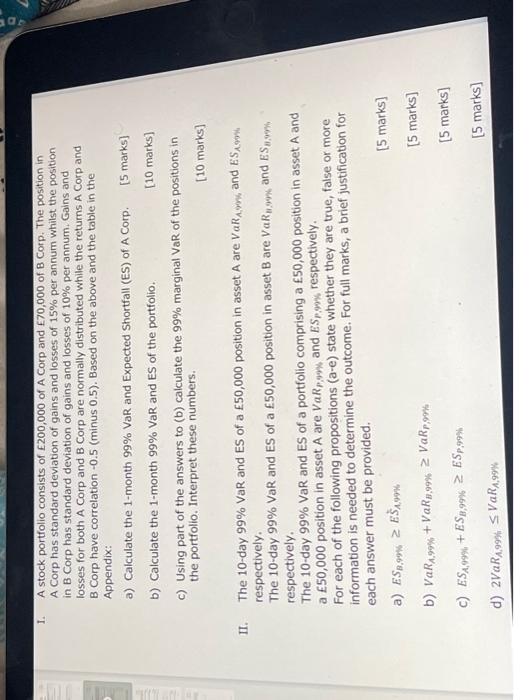

it is a risk management course 1. A stock portfolio consists of E200,000 of A Corp and E70,000 of B Corp. The position in A

it is a risk management course

1. A stock portfolio consists of E200,000 of A Corp and E70,000 of B Corp. The position in A Corp has standard deviation of gains and losses of 15% per annum whilst the position in B Corp has standard deviation of gains and losses of 10% per annum. Gains and losses for both A Corp and B Corp are normally distributed while the returns A Corp and B Corp have correlation -0.5 (minus 0.5 ). Based on the above and the table in the Appendix: a) Calculate the 1-month 99% VaR and Expected Shortfall (ES) of A Corp. [5 marks] b) Calculate the 1-month 99% VaR and ES of the portfolio. [10 marks] c) Using part of the answers to (b) calculate the 99% marginal VaR of the positions in the portfolio. Interpret these numbers. [10 marks] respectively. The 10-day 99%VaR and ES of a 50,000 position in asset B are VaRB,90% and ESB,9% respectively. The 10-day 99%VaR and ES of a portfolio comprising a 50,000 position in asset A and a E50,000 position in asset A are VaRp,9m and ESp,9% respectively. For each of the following propositions (a-e) state whether they are true, false or more information is needed to determine the outcome. For full marks, a brief justification for each answer must be provided. a) ESB,99%ESA,9% [5 marks] b) VaRA,99%+VaRB,99%VaRP,9m [5 marks] c) ESA,99%+ESB,99%ESP,99% [5 marks] d) 2VaRA,999%VaRA,99% [5 marks] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mergers And Acquisitions A Study Of Financial Performance Motives And Corporate Governance

Authors: Neelam Rani , Surendra Singh Yadav, Pramod Kumar Jain

1st Edition

981102202X,9811022038