It will be very helpful and easy to understand if you follow just like attached Excel screenshot.

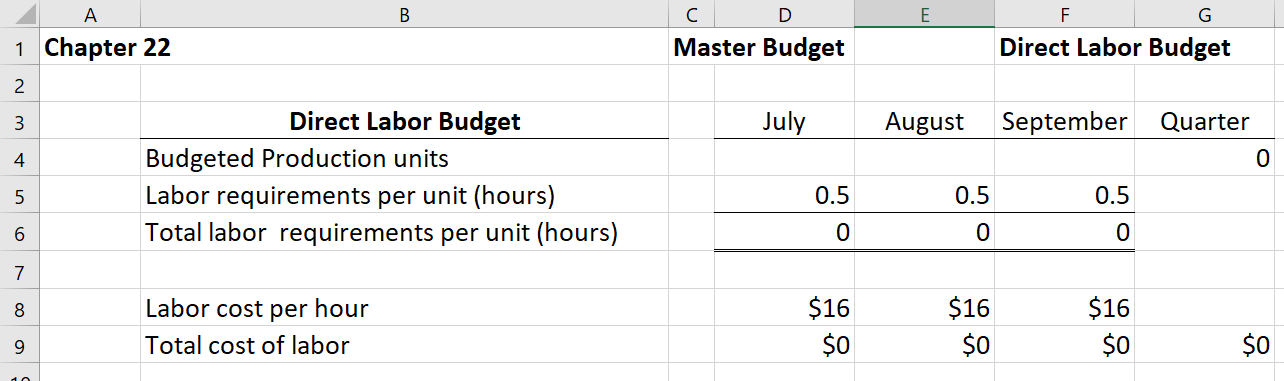

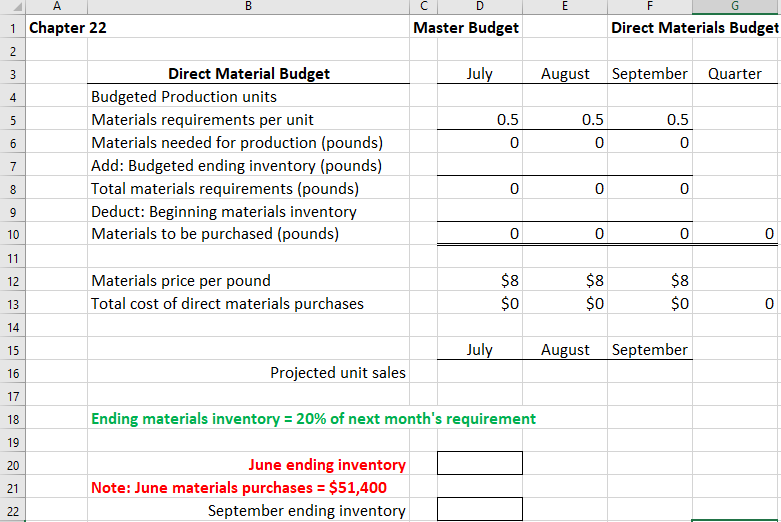

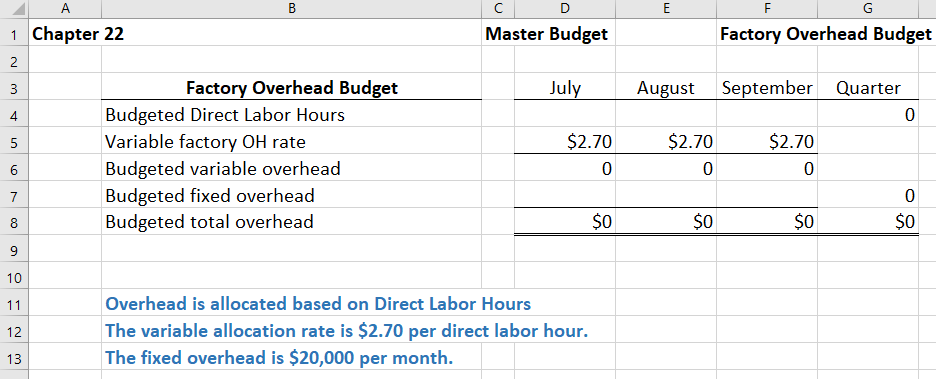

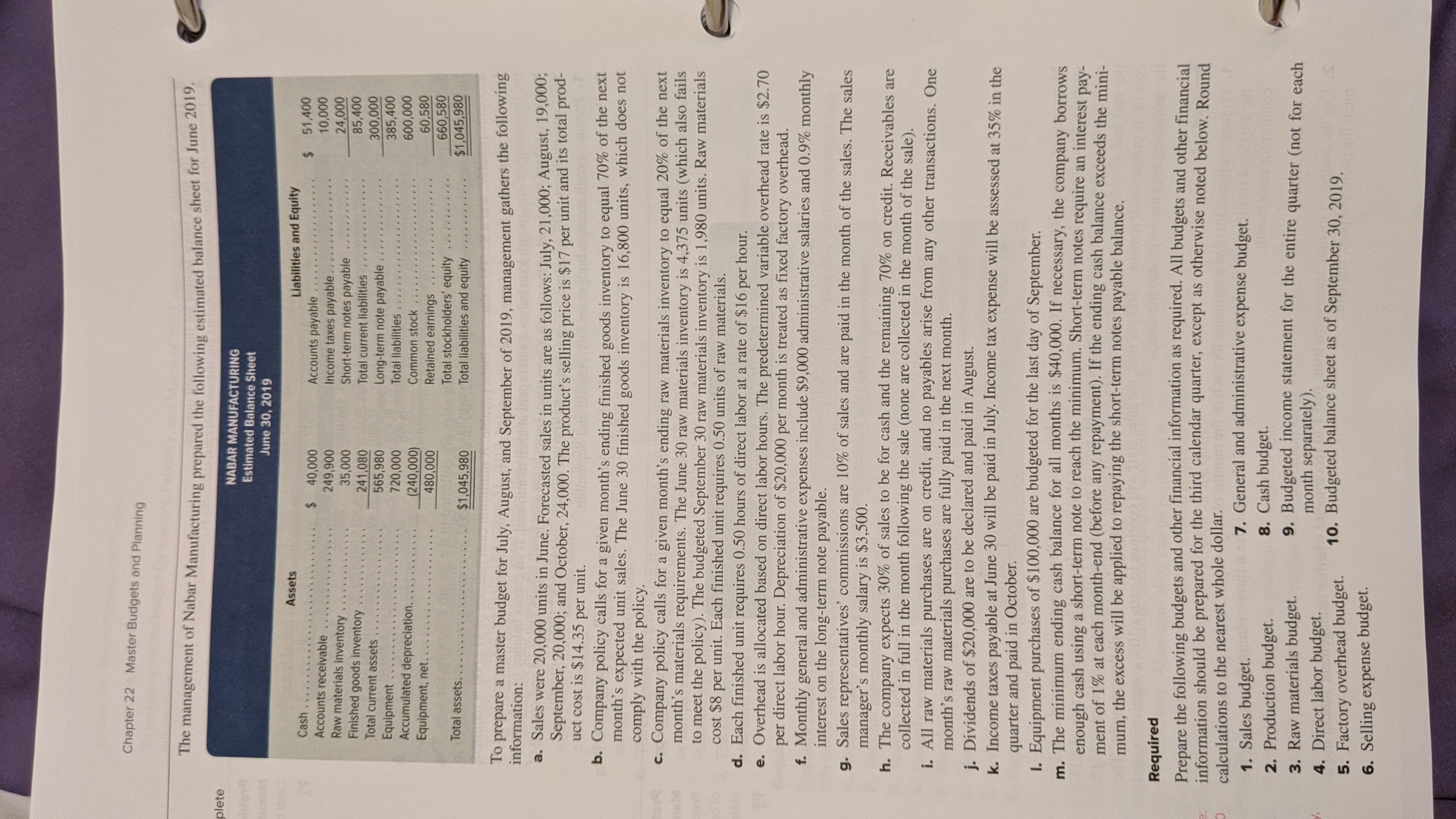

L ) A A l B | c | D E I F | G l 1_ Chapter 22 Master Budget Direct Labor Budget 2_ 1 Direct Labor Budget July August September Quarter 4_ Budgeted Production units 0 5_ Labor requirements per unit (hours) 0.5 0 5 0.5 6_ Total labor requirements per unit (hours) 0 0 0 7_ 8 Labor cost per hour 516 $16 $16 9_ Total cost of labor $0 S0 $0 $0 4 A | B | c | D | E | F | G | 1_ Chapter 22 Master Budget Direct Materials Budget 2_ 3 Direct Material Budget July August September Quarter 4 Budgeted Production units 5_ Materials requirements per unit 0.5 0.5 0.5 6_ Materials needed for production {pounds} 0 0 0 7 Add: Budgeted ending inventory {pounds} 8_ Total materials requirements {pounds} 0 0 0 9_ Deduct: Beginning materials inventory B Materials to be purchased {pounds} 0 0 0 1 3 Materials price per pound $8 $8 $8 3 Total cost of direct materials purchases 50 $0 $0 1 3 July August September E Projected unit sales 1 E Ending materials inventory = 20% of next month's requirement 3 21 June ending inventory 1 Note: June materials purchases = 551,400 g September ending inventory .- N UJ A A | B | c | D | E | F | G l 1_ Chapter 22 Master Budget Factory Overhead Budget 2_ 3_ Factory Overhead Budget July August September Quarter 4 Budgeted Direct Labor Hours 0 5_ Variable factory 0H rate $2.70 $2.70 $2.70 5_ Budgeted variable overhead 0 0 0 ?_ Budgeted fixed overhead 0 8 Budgeted total overhead $0 $0 $0 $0 9_ 3 Overhead is allocated based on Direct Labor Hours The variable allocation rate is $2.70 per direct labor hour. The fixed overhead is $20,000 per month. Chapter 22 Master Budgets and Planning The management of Nabar Manufacturing prepared the following estimated balance sheet for June 2019. plete NABAR MANUFACTURING Estimated Balance Sheet June 30, 2019 Assets Liabilities and Equity Cash ......... ................ .. $ 40,000 Accounts payable . ..... .. .. .. . . . . ... $ 51,400 Accounts receivable ...... . . .. .. .. .. 249,900 10,000 Raw materials inventory ......... ... . . Income taxes payable ................ Finished goods inventory ..... ... . . .. . 35,000 Short-term notes payable ............ 24,000 Total current assets . .. 241,080 Total current liabilities .......... . . . .. 85,400 565,980 300,000 Equipment .... . Long-term note payable ............ .. 720,000 Total liabilities ........ . . . . . . . . . .. . .. 385,400 Accumulated depreciation. Equipment, net. ....... . .. . (240,000) Common stock ..... .... . . . . . . . . . ... 600,000 . . . . 480,000 Retained earnings............ ...... 60,580 Total assets. .......... Total stockholders' equity............ 660,580 $1,045,980 Total liabilities and equity............ $1,045,980 information: To prepare a master budget for July, August, and September of 2019, management gathers the following a. Sales were 20,000 units in June. Forecasted sales in units are as follows: July, 21,000; August, 19,000; September, 20,000; and October, 24,000. The product's selling price is $17 per unit and its total prod- uct cost is $14.35 per unit. b. Company policy calls for a given month's ending finished goods inventory to equal 70% of the next month's expected unit sales. The June 30 finished goods inventory is 16,800 units, which does not comply with the policy. c. Company policy calls for a given month's ending raw materials inventory to equal 20% of the next month's materials requirements. The June 30 raw materials inventory is 4,375 units (which also fails to meet the policy). The budgeted September 30 raw materials inventory is 1,980 units. Raw materials cost $8 per unit. Each finished unit requires 0.50 units of raw materials. d. Each finished unit requires 0.50 hours of direct labor at a rate of $16 per hour. e. Overhead is allocated based on direct labor hours. The predetermined variable overhead rate is $2.70 per direct labor hour. Depreciation of $20,000 per month is treated as fixed factory overhead. f. Monthly general and administrative expenses include $9,000 administrative salaries and 0.9% monthly interest on the long-term note payable. g. Sales representatives' commissions are 10% of sales and are paid in the month of the sales. The sales manager's monthly salary is $3,500. h. The company expects 30% of sales to be for cash and the remaining 70% on credit. Receivables are collected in full in the month following the sale (none are collected in the month of the sale). i. All raw materials purchases are on credit, and no payables arise from any other transactions. One month's raw materials purchases are fully paid in the next month. j. Dividends of $20,000 are to be declared and paid in August. k. Income taxes payable at June 30 will be paid in July. Income tax expense will be assessed at 35% in the quarter and paid in October. I. Equipment purchases of $100,000 are budgeted for the last day of September. m. The minimum ending cash balance for all months is $40,000. If necessary, the company borrows enough cash using a short-term note to reach the minimum. Short-term notes require an interest pay- ment of 1% at each month-end (before any repayment). If the ending cash balance exceeds the mini- mum, the excess will be applied to repaying the short-term notes payable balance. Required Prepare the following budgets and other financial information as required. All budgets and other financial information should be prepared for the third calendar quarter, except as otherwise noted below. Round calculations to the nearest whole dollar. 1. Sales budget. 7. General and administrative expense budget. 2. Production budget. 8. Cash budget. 3. Raw materials budget. 9. Budgeted income statement for the entire quarter (not for each 4. Direct labor budget. month separately). 5. Factory overhead budget. 10. Budgeted balance sheet as of September 30, 2019. 6. Selling expense budget.A B C D E F G H 1 J K L My N 0 Chapter 22 Master Budget Production Budget IN Production Budget July August September Quarter Next months' budgeted sales (units) from Sales Budget Ratio of inventory to future sales 70.0% 70.0% 70.0% 6 Budgeted ending inventory (units) 0 0 0 Operating plan - ending inventory = 70% of next month's predicted sales Add: Budgeted sales (units) 8 Required units of available production 0 0 0 Deduct: Beginning inventory (units) 10 Units to be produced 0 0 0 0 11 12 13 July August September 14 Projected unit sales 15 16 June ending inventoryA A l B lcl D l E I F G | 1_ Chapter 22 Master Budget 2_ 3_ Sales Budget July:r August September Quarter 4_ Projected unit sales 0 5_ Selling price per unit 5 Projected sales $0 SO SO SO 7 a 9_ 11 Previous Month June 11_ Actual unit sales 1i Selling price per unit 13 $0 1: H | I Sales Budget