Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Items 1 through 5 present various independent factual situations an auditor might encounter in conducting an audit of a nonpublic company. For each situation, assume:

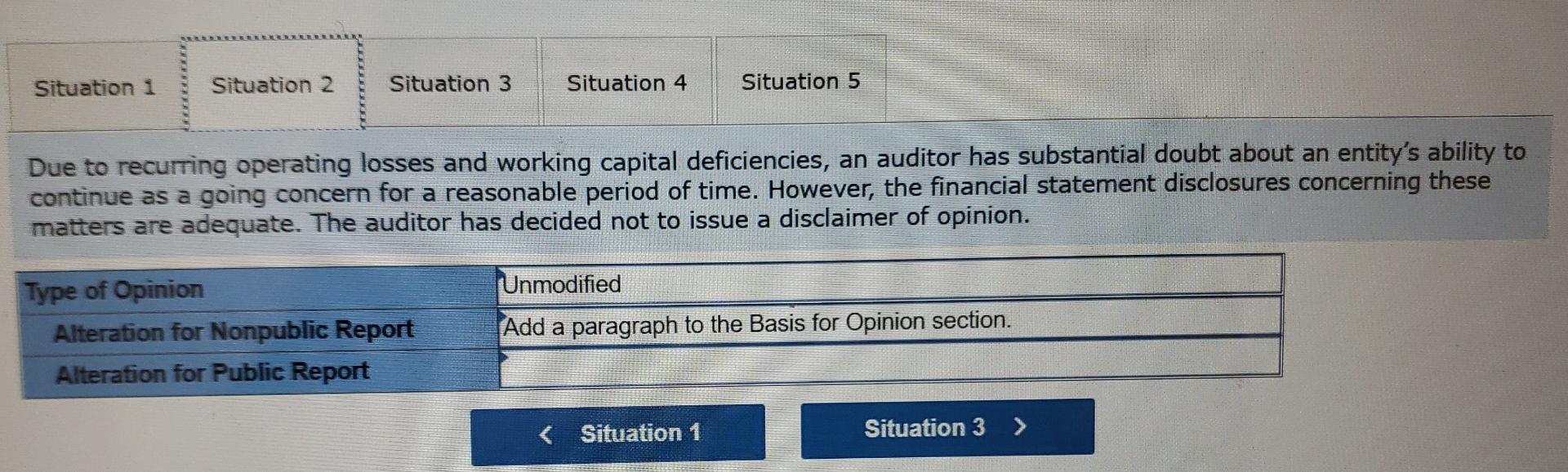

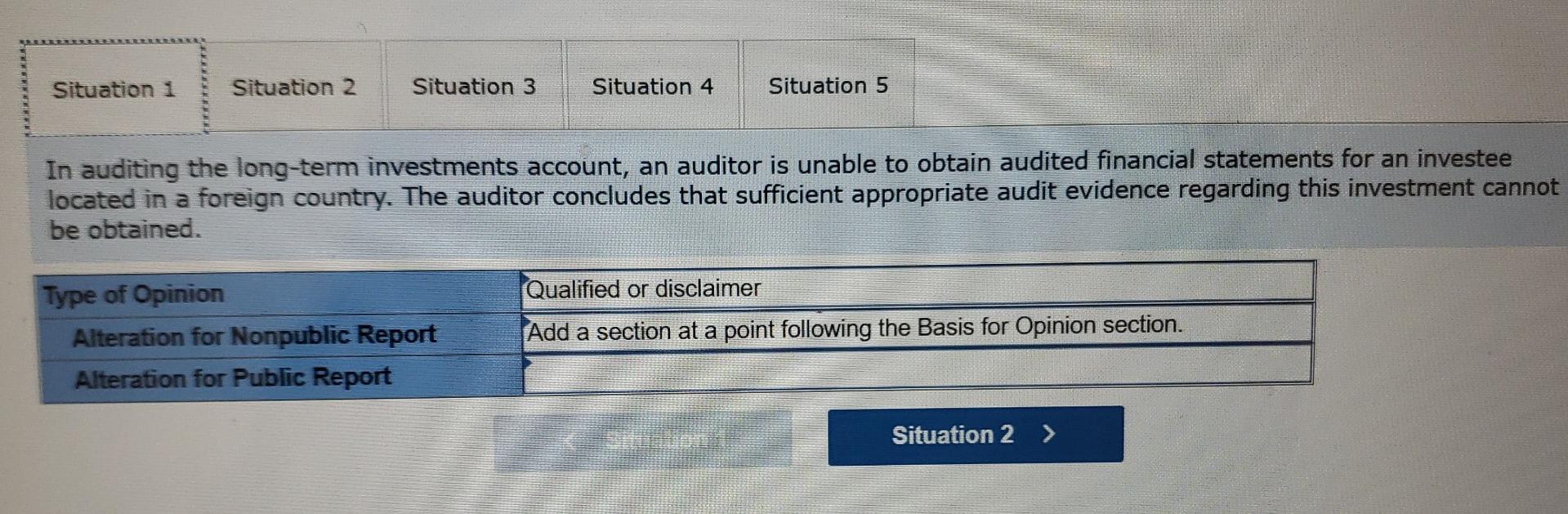

Items 1 through 5 present various independent factual situations an auditor might encounter in conducting an audit of a nonpublic company. For each situation, assume: The auditor is independent. The auditor previously expressed an unmodified opinion on the prior year's financial statements. The nonpublic audit client is presenting single-year (not comparative) financial statements. The conditions for an unmodified opinion exist unless contradicted in the factual situations. . The conditions stated in the factual situations are material. No report modifications are to be made except in response to the factual situation. The Report Alteration part of the problem only addresses the need to add an additional section or a paragraph to an existing section. Other parts of the audit report may be affected that are not examined in this question. Required: Below are the types of opinions the auditor ordinarily would issue and report modifications (if any) relating to an additional paragraph or section that would be necessary. Select as the best answer for each situation (items 1 through 5) the type of opinion and alterations, if any, the auditor would normally select. For each situation (items 1 through 5) also provide the report alteration under PCAOB standards for audits of public companies. Types of Opinions A. Unmodified B. Qualified Report Alteration H. Add a section preceding the Opinion section. I. Add a section immediately following the Opinion section. 3. Add a section at a point following the Basis for Opinion section. K. Add a paragraph to the Opinion section. L. Add a paragraph to the Basis for Opinion C. Adverse D. Disclaimer E. Qualified or adverse F. Qualified or disclaimer G. Disclaimer or adverse M. Issue unmodified report without alteration. Situation 1 Situation 2 Situation 3 Situation 4 Situation 5 An entity changes its depreciation method for production equipment from straight-line to a units-of-production method based on hours of utilization. The auditor concurs with the change, although it has a material effect on the comparability of the entity's financial statements. Unmodified Type of Opinion Alteration for Nonpublic Report Alteration for Public Report Add a section immediately following the Opinion section. Situation 1 Situation 2 Situation 3 Situation 4 Situation 5 An entity discloses certain lease obligations in the notes to the financial statements. The auditor believes that the failure to capitalize these leases is a departure from generally accepted accounting principles and, although the possible effects on the financial statements of the misstatements are material, they could not be pervasive. Qualified Type of Opinion Alteration for Nonpublic Report Alteration for Public Report Add a section immediately following the Opinion section. Situation 1 Situation 2 Situation 3 Situation 4 Situation 5 Due to recurring operating losses and working capital deficiencies, an auditor has substantial doubt about an entity's ability to continue as a going concern for a reasonable period of time. However, the financial statement disclosures concerning these matters are adequate. The auditor has decided not to issue a disclaimer of opinion. Unmodified Type of Opinion Alteration for Nonpublic Report Alteration for Public Report Add a paragraph to the Basis for Opinion section. Situation 1 Situation 2 Situation 3 Situation 4 Situation 5 In auditing the long-term investments account, an auditor is unable to obtain audited financial statements for an investee located in a foreign country. The auditor concludes that sufficient appropriate audit evidence regarding this investment cannot be obtained. Qualified or disclaimer Type of Opinion Alteration for Nonpublic Report Alteration for Public Report Add a section at a point following the Basis for Opinion section. Situation 2 >

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

MBA Accounting

Authors: Roger Hussey

1st Edition

0230303374, 9780230303379