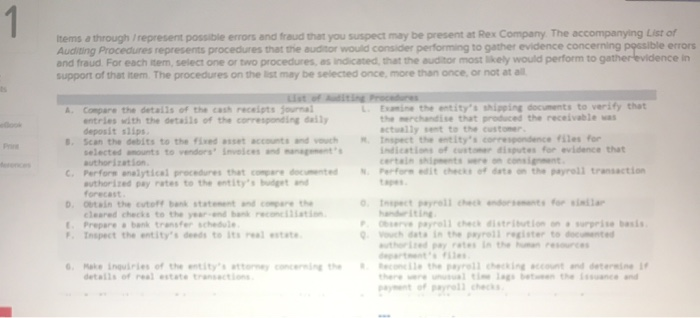

Items a through represent possible errors and fraud that you suspect may be present at Rex Company. The accompanying List of Auditing Procedures represents procedures that the auditor would consider performing to gather evidence concerning possible errors and fraud. For each item, select one or two procedures, as indicated that the auditor most kely would perform to gather evidence in support of that item. The procedures on the list may be selected once more than once, or not at all L Ult i A compare the details of the cash receipts journal entries with the details of the corresponding daily deposit slips 3Scan the debits to the fixed asset a ut o th selected amounts to vendors invoices authorization, C.Perfors alytical procedures that connec ted authorized pay rates to the entity's budget forecast D otain the cutoff bank statement compare the cleared checks to the year and bank reconciliati Preparebank transfer Schedule Tnspect the entity's deeds to its real estate Procedures i ne the entity's s ing documents to verify that the-chandise that produced the receivable was actually set to the customer . Inspect the entity's correspondence files for indications of custar disputes for evidence that o t that of data on the payroll transaction N v yroll the distribution data in the payroll resterto surprise basis n 0. Make inquiries of the entity's rec h e Items a through represent possible errors and fraud that you suspect may be present at Rex Company. The accompanying List of Auditing Procedures represents procedures that the auditor would consider performing to gather evidence concerning possible errors and fraud. For each item, select one or two procedures, as indicated that the auditor most kely would perform to gather evidence in support of that item. The procedures on the list may be selected once more than once, or not at all L Ult i A compare the details of the cash receipts journal entries with the details of the corresponding daily deposit slips 3Scan the debits to the fixed asset a ut o th selected amounts to vendors invoices authorization, C.Perfors alytical procedures that connec ted authorized pay rates to the entity's budget forecast D otain the cutoff bank statement compare the cleared checks to the year and bank reconciliati Preparebank transfer Schedule Tnspect the entity's deeds to its real estate Procedures i ne the entity's s ing documents to verify that the-chandise that produced the receivable was actually set to the customer . Inspect the entity's correspondence files for indications of custar disputes for evidence that o t that of data on the payroll transaction N v yroll the distribution data in the payroll resterto surprise basis n 0. Make inquiries of the entity's rec h e