Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Ive answered the first need help verifying and doing the rest can some please quickly respond. Due by 11:59 pm on Wednesday, Nov 23 submitted

Ive answered the first need help verifying and doing the rest can some please quickly respond.

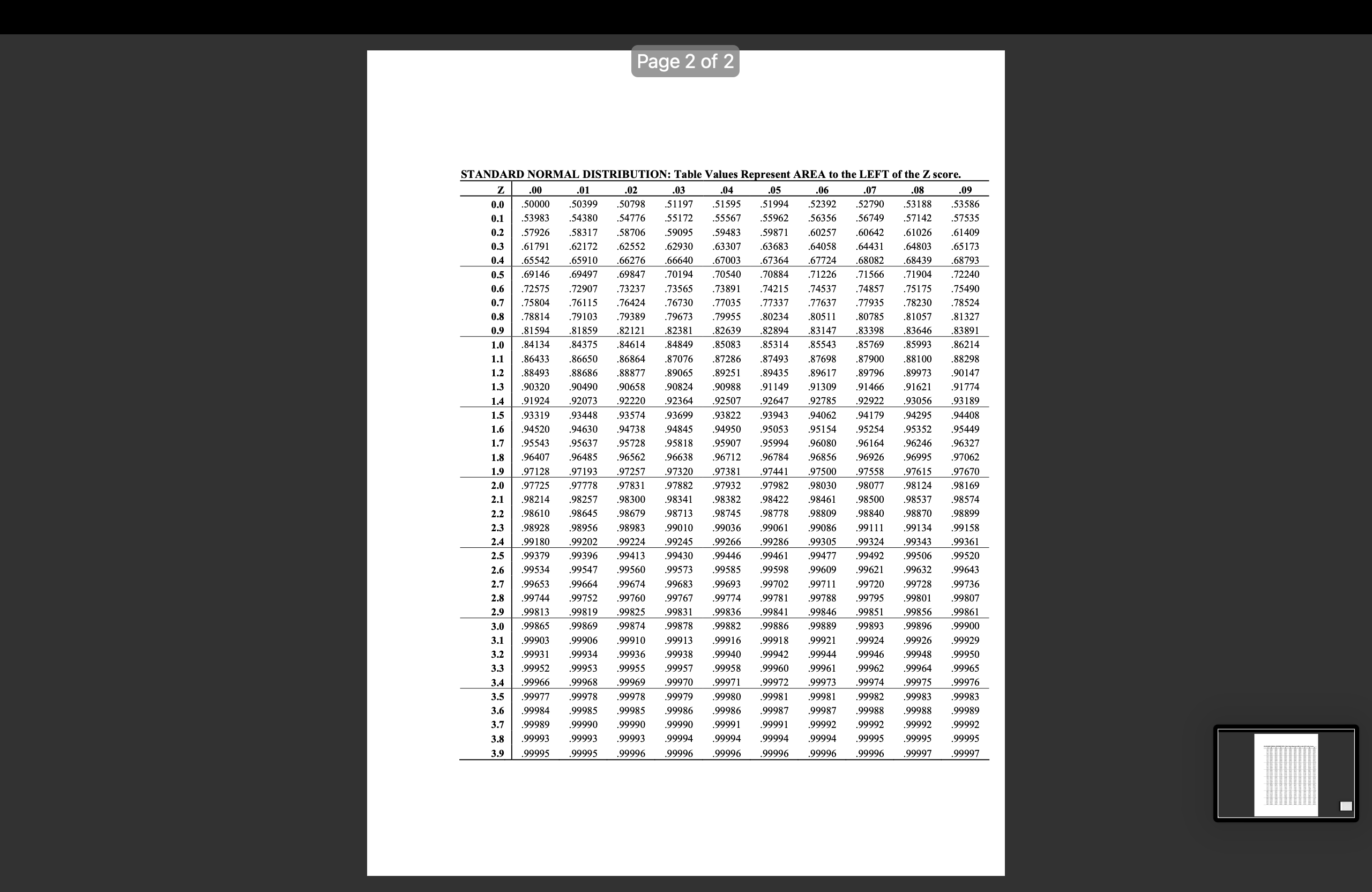

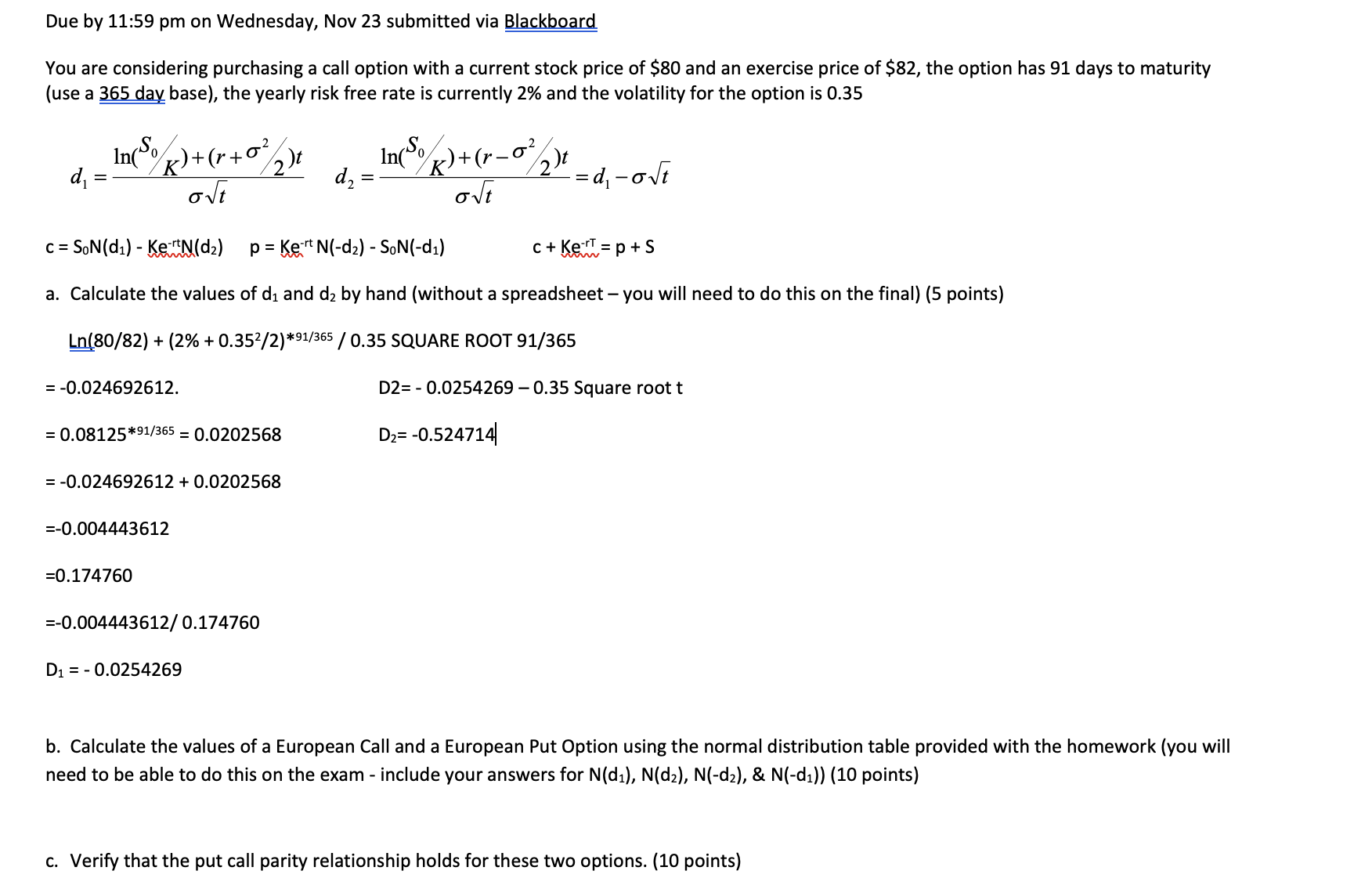

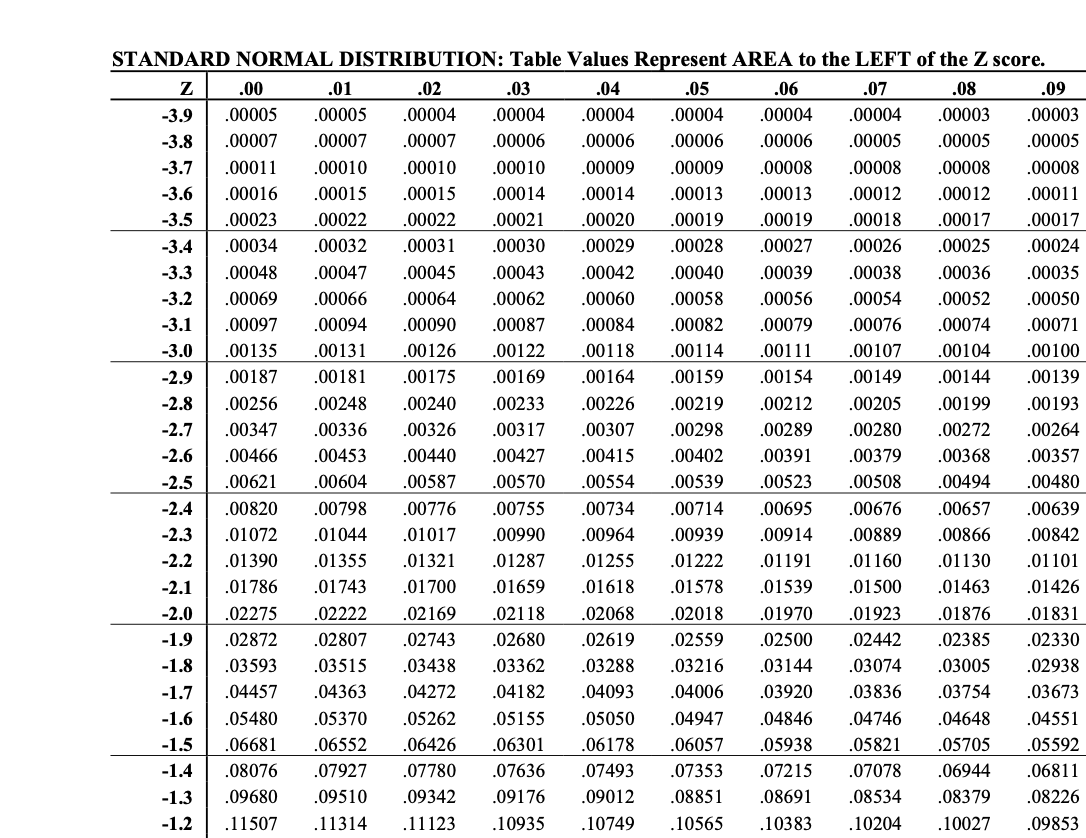

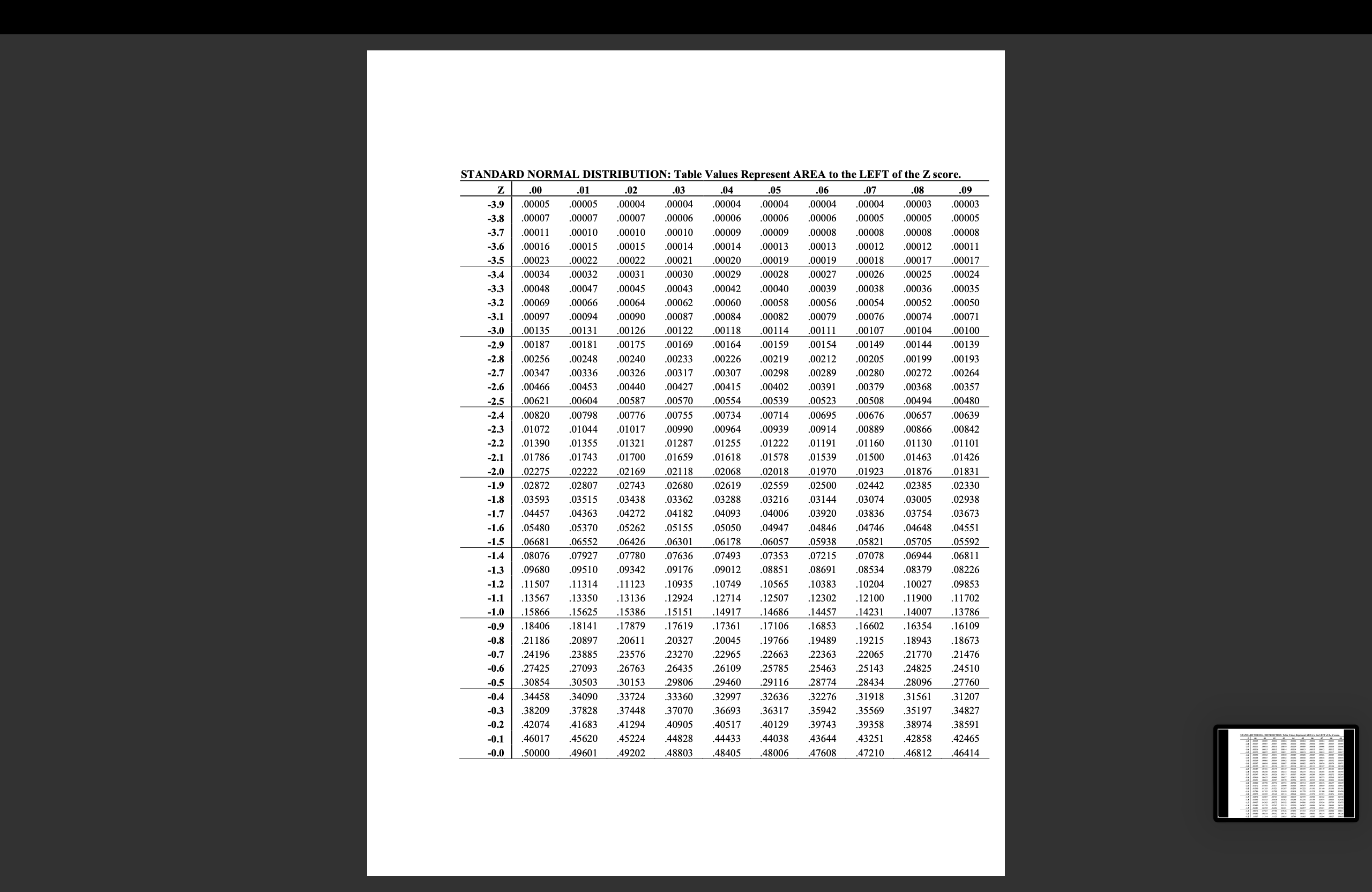

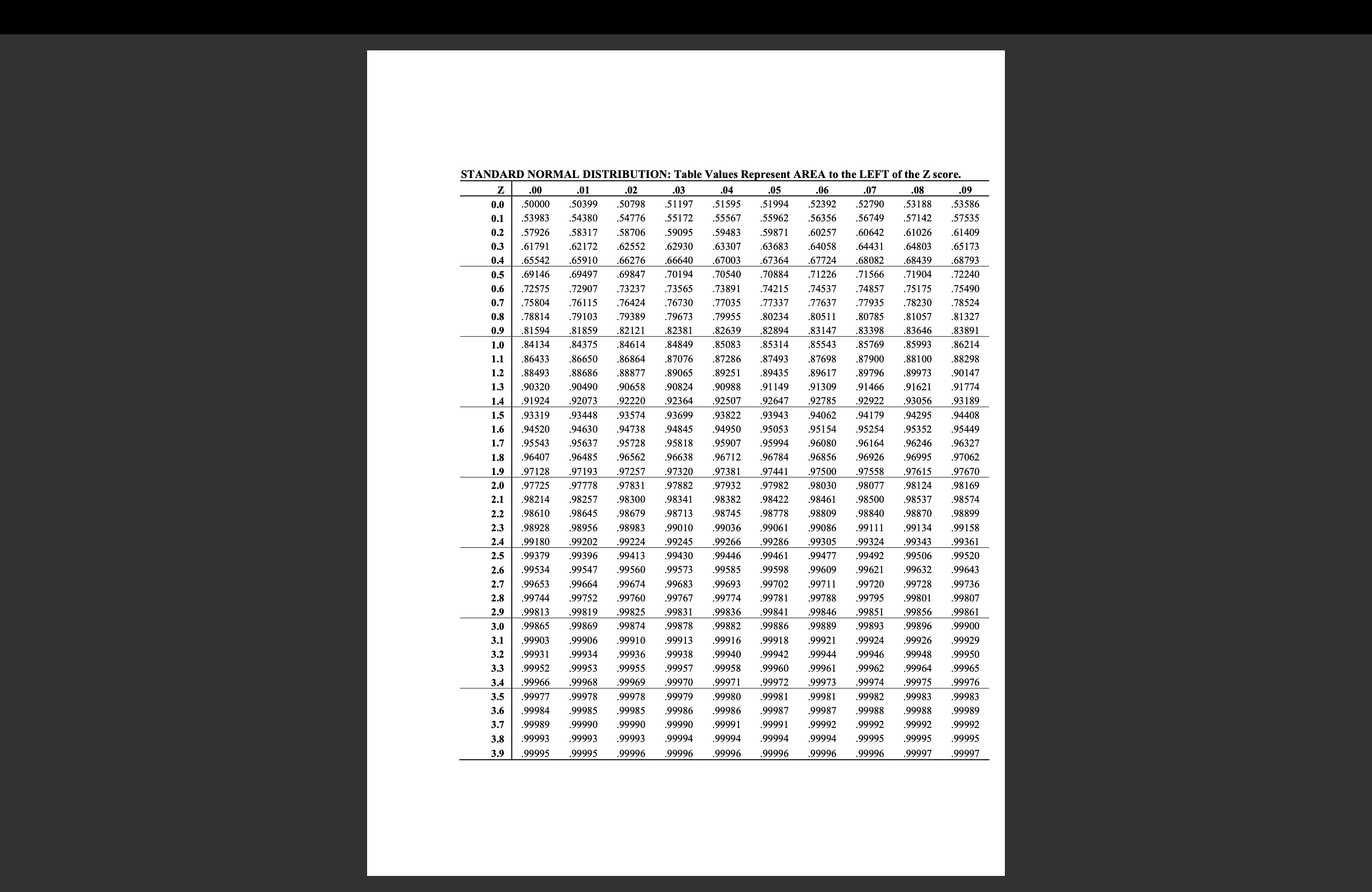

Due by 11:59 pm on Wednesday, Nov 23 submitted via Blackboard You are considering purchasing a call option with a current stock price of $80 and an exercise price of $82, the option has 91 days to maturity (use a 365dav base), the yearly risk free rate is currently 2% and the volatility for the option is 0.35 d1=tln(S0/K)+(r+2/2)td2=tln(S0/K)+(r2/2)t=d1tc=S0N(d1)KertNN(d2)p=KertN(d2)S0N(d1)c+KerT=p+S a. Calculate the values of d1 and d2 by hand (without a spreadsheet - you will need to do this on the final) ( 5 points) Ln(80/82)+(2%+0.352/2)91/365/0.35SQUAREROOT91/365=0.024692612.D2=0.02542690.35Squareroott=0.0812591/365=0.0202568D2=0.524714=0.024692612+0.0202568=0.004443612=0.174760=0.004443612/0.174760D1=0.0254269 b. Calculate the values of a European Call and a European Put Option using the normal distribution table provided with the homework (you will need to be able to do this on the exam - include your answers for N(d1),N(d2),N(d2),&N(d1))(10 points) c. Verify that the put call parity relationship holds for these two options. (10 points) d. What initial investment is required for a delta hedged portfolio (assume one option)? (10 points) e. Calculate the overnight profit or loss on the delta hedged portfolio if the stock price increases to $84 and if it decreases to $76. (10 points) STANDARD NORMAL DISTRIBUTION: Table Values Represent AREA to the LEFT of the Z score. \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|} \hline Z & .00 & .01 & .02 & .03 & .04 & .05 & .06 & .07 & .08 & .09 \\ \hline-3.9 & .00005 & .00005 & .00004 & .00004 & .00004 & .00004 & .00004 & .00004 & .00003 & .00003 \\ \hline-3.8 & .00007 & .00007 & .00007 & .00006 & .00006 & .00006 & 00006 & .00005 & .00005 & .00005 \\ \hline-3.7 & .00011 & .00010 & .00010 & .00010 & .00009 & .00009 & .00008 & .00008 & .00008 & .00008 \\ \hline-3.6 & .00016 & .00015 & .00015 & .00014 & .00014 & .00013 & .00013 & .00012 & .00012 & .00011 \\ \hline-3.5 & .00023 & .00022 & .00022 & .00021 & .00020 & .00019 & .00019 & .00018 & .00017 & .00017 \\ \hline-3.4 & .00034 & .00032 & .00031 & .00030 & .00029 & .00028 & .00027 & .00026 & .00025 & .00024 \\ \hline-3.3 & .00048 & .00047 & .00045 & .00043 & .00042 & .00040 & .00039 & .00038 & .00036 & .00035 \\ \hline-3.2 & .00069 & .00066 & .00064 & .00062 & .00060 & .00058 & .00056 & .00054 & .00052 & .00050 \\ \hline-3.1 & .00097 & .00094 & .00090 & .00087 & .00084 & .00082 & .00079 & .00076 & .00074 & .00071 \\ \hline-3.0 & .00135 & .00131 & .00126 & .00122 & .00118 & .00114 & .00111 & .00107 & .00104 & .00100 \\ \hline-2.9 & .00187 & .00181 & .00175 & .00169 & .00164 & .00159 & .00154 & .00149 & .00144 & .00139 \\ \hline-2.8 & .00256 & .00248 & .00240 & .00233 & .00226 & .00219 & .00212 & .00205 & 00199 & .00193 \\ \hline-2.7 & .00347 & .00336 & .00326 & .00317 & .00307 & .00298 & .00289 & .00280 & .00272 & .00264 \\ \hline-2.6 & .00466 & .00453 & .00440 & .00427 & .00415 & .00402 & .00391 & .00379 & .00368 & .00357 \\ \hline-2.5 & .00621 & .00604 & .00587 & .00570 & .00554 & .00539 & .00523 & .00508 & .00494 & .00480 \\ \hline-2.4 & .00820 & .00798 & .00776 & .00755 & .00734 & .00714 & .00695 & .00676 & .00657 & .00639 \\ \hline-2.3 & .01072 & .01044 & .01017 & .00990 & .00964 & .00939 & .00914 & .00889 & .00866 & .00842 \\ \hline-2.2 & .01390 & .01355 & .01321 & .01287 & .01255 & .01222 & .01191 & .01160 & .01130 & .01101 \\ \hline-2.1 & .01786 & .01743 & .01700 & .01659 & .01618 & .01578 & .01539 & .01500 & .01463 & .01426 \\ \hline-2.0 & .02275 & .02222 & .02169 & .02118 & .02068 & .02018 & .01970 & .01923 & .01876 & .01831 \\ \hline-1.9 & .02872 & .02807 & .02743 & .02680 & .02619 & .02559 & .02500 & .02442 & .02385 & .02330 \\ \hline-1.8 & .03593 & .03515 & .03438 & .03362 & .03288 & .03216 & .03144 & .03074 & .03005 & .02938 \\ \hline-1.7 & .04457 & .04363 & .04272 & .04182 & .04093 & .04006 & 03920 & .03836 & .03754 & .03673 \\ \hline-1.6 & .05480 & .05370 & .05262 & .05155 & .05050 & .04947 & .04846 & .04746 & .04648 & .04551 \\ \hline-1.5 & .06681 & .06552 & .06426 & .06301 & .06178 & .06057 & .05938 & .05821 & .05705 & .05592 \\ \hline-1.4 & .08076 & .07927 & .07780 & .07636 & .07493 & .07353 & .07215 & .07078 & .06944 & .06811 \\ \hline-1.3 & .09680 & 09510 & .09342 & .09176 & .09012 & .08851 & .08691 & .08534 & 08379 & .08226 \\ \hline-1.2 & .11507 & .11314 & .11123 & .10935 & .10749 & .10565 & .10383 & .10204 & .10027 & .09853 \\ \hline \end{tabular}Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: R. Charles Moyer, James R. McGuigan, William J. Kretlow

11th Edition

0324653506, 978-0324653502