Answered step by step

Verified Expert Solution

Question

1 Approved Answer

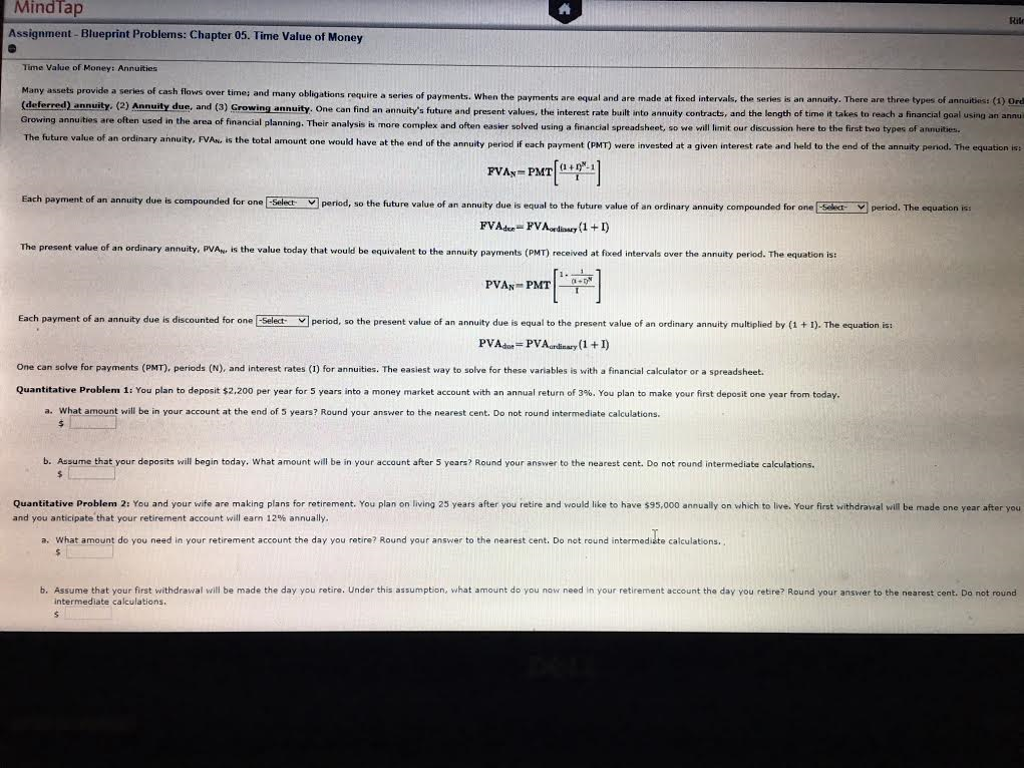

I've uploaded a different picture that is clearer. I can't make it any bigger without cropping out some of the text. Please no finance? This

I've uploaded a different picture that is clearer. I can't make it any bigger without cropping out some of the text. Please no finance? This is an Intro to Finance Class...and i've listed it in finance...

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding The Finance Of Welfare

Authors: Howard Glennerster

2nd Edition

1847421091, 978-1847421098