IVEY Publishing 9A87 JO06 LAWSONS Peter Farrell wrote this case under the supervision of Richard H. Mimick solely to provide material for class discussion. The

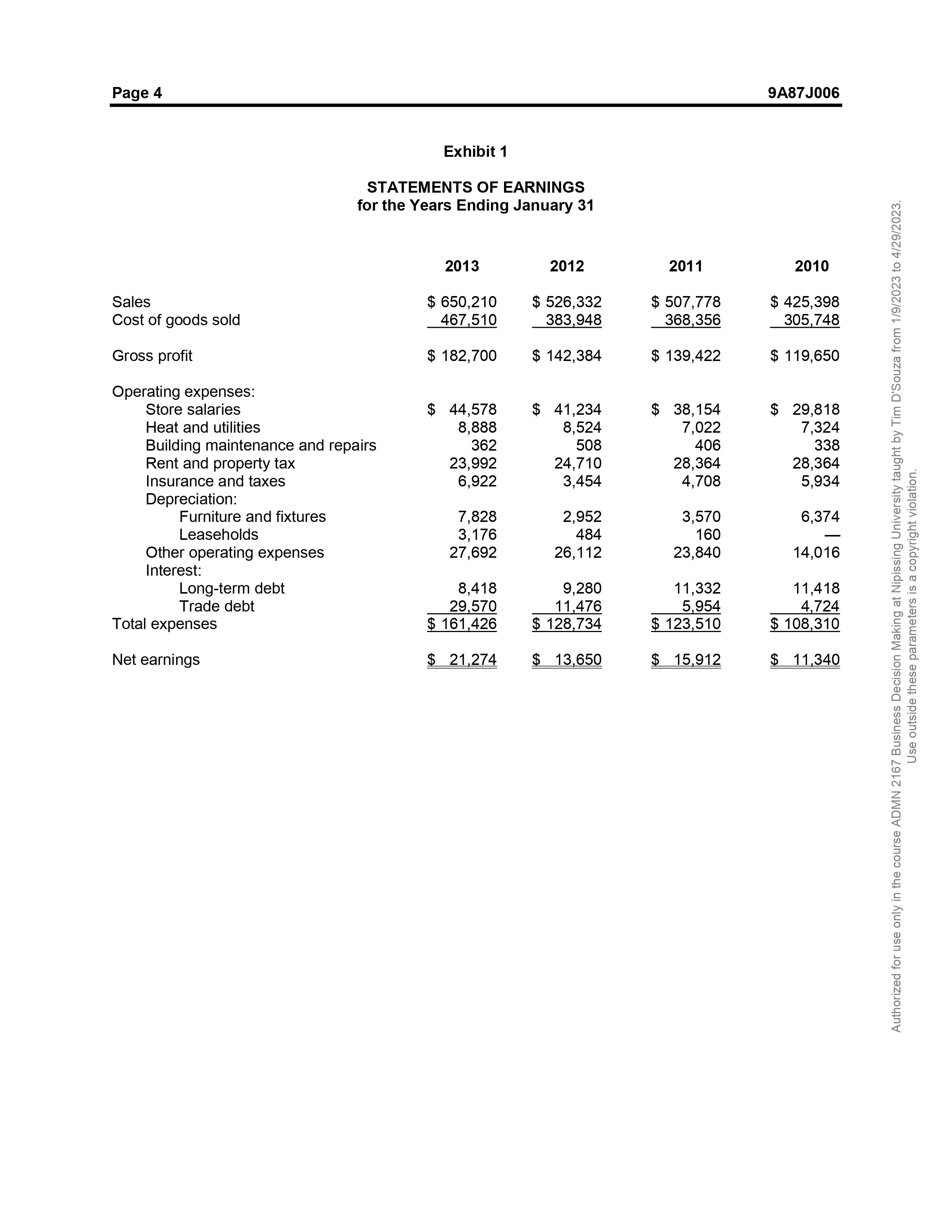

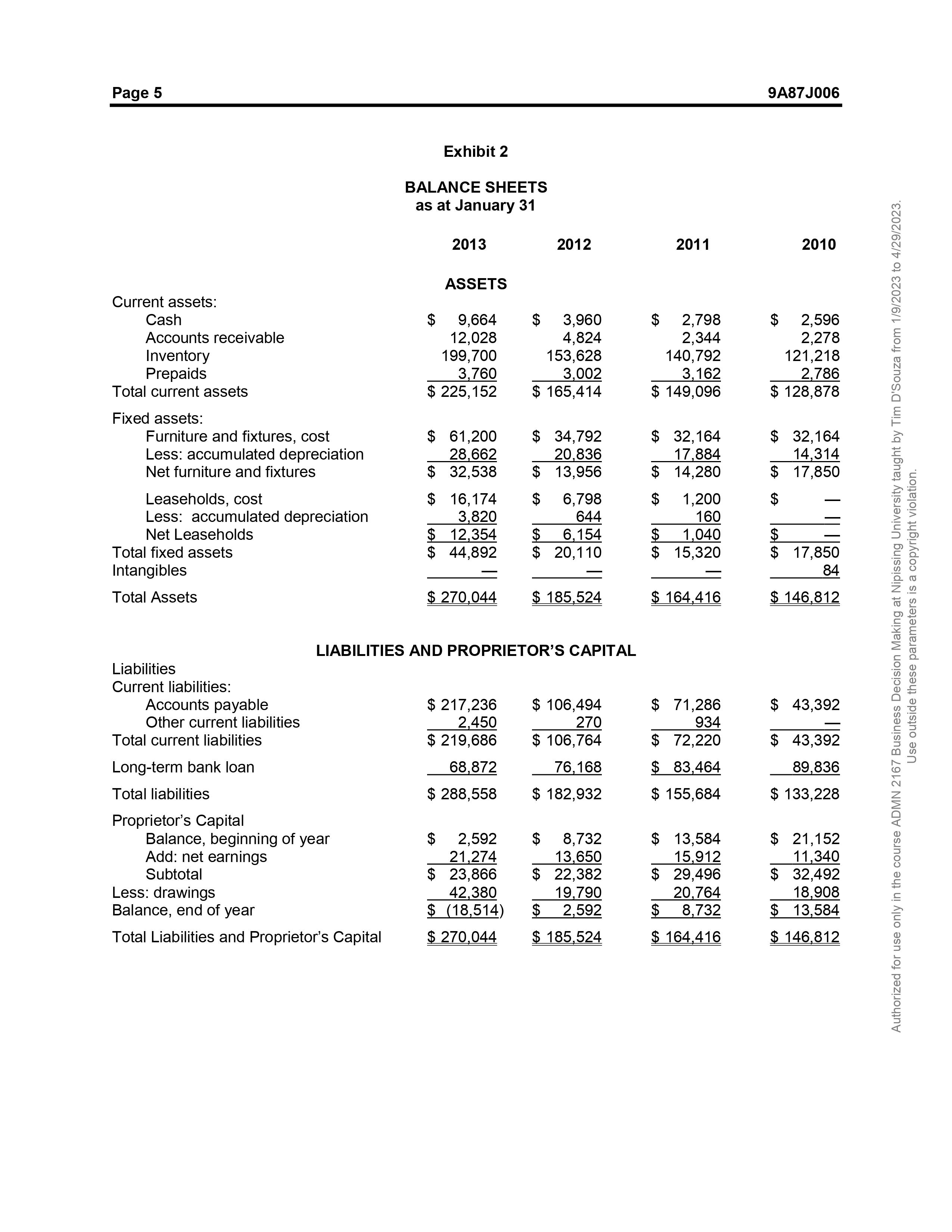

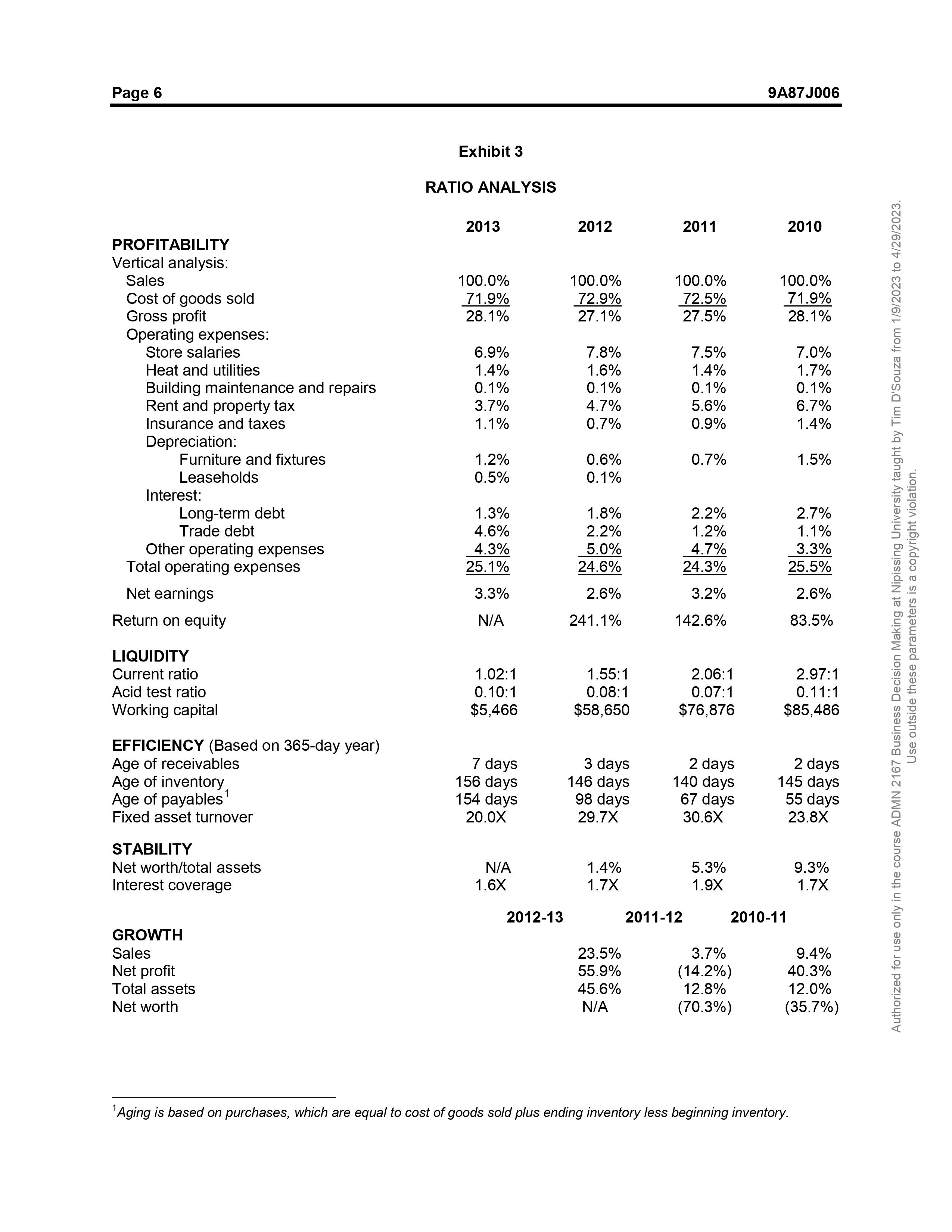

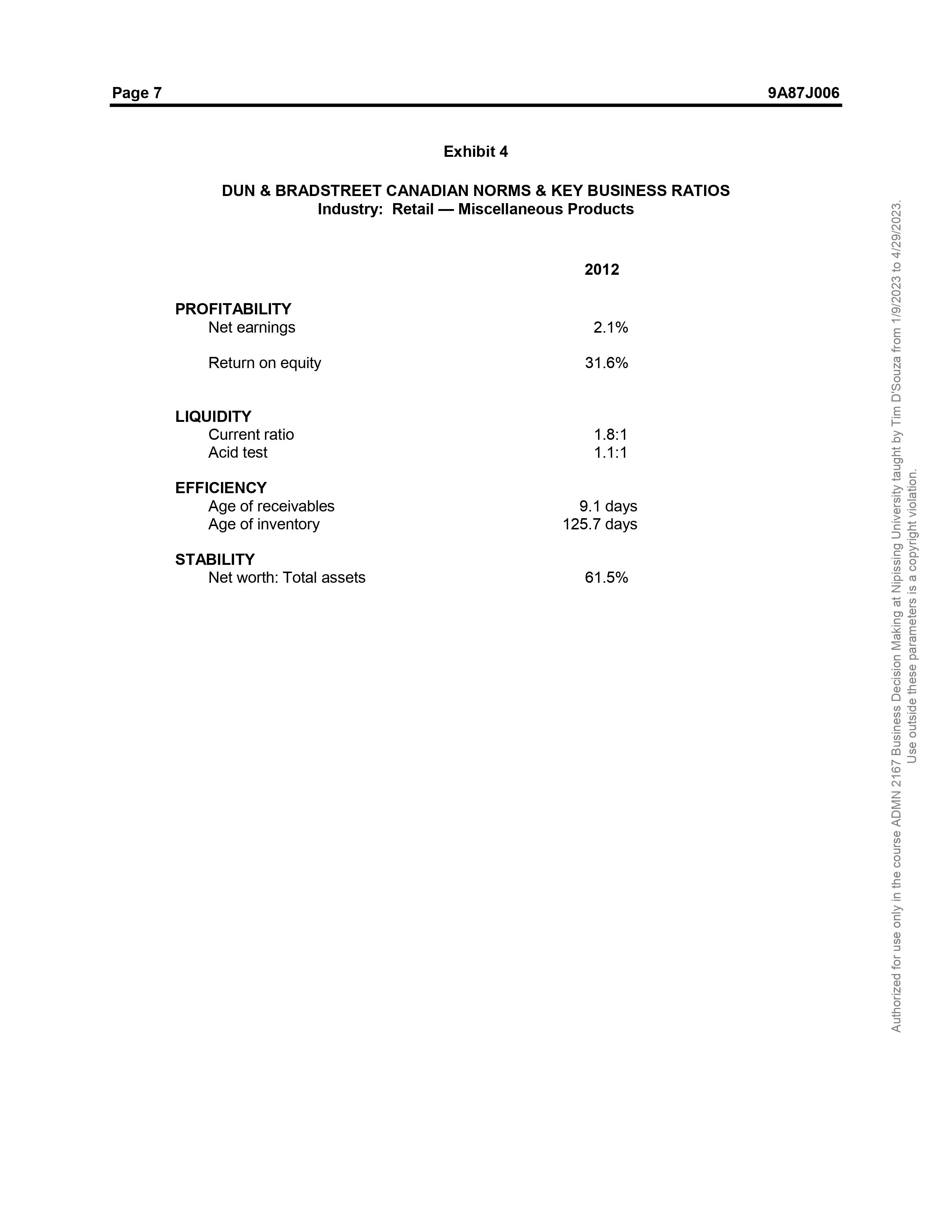

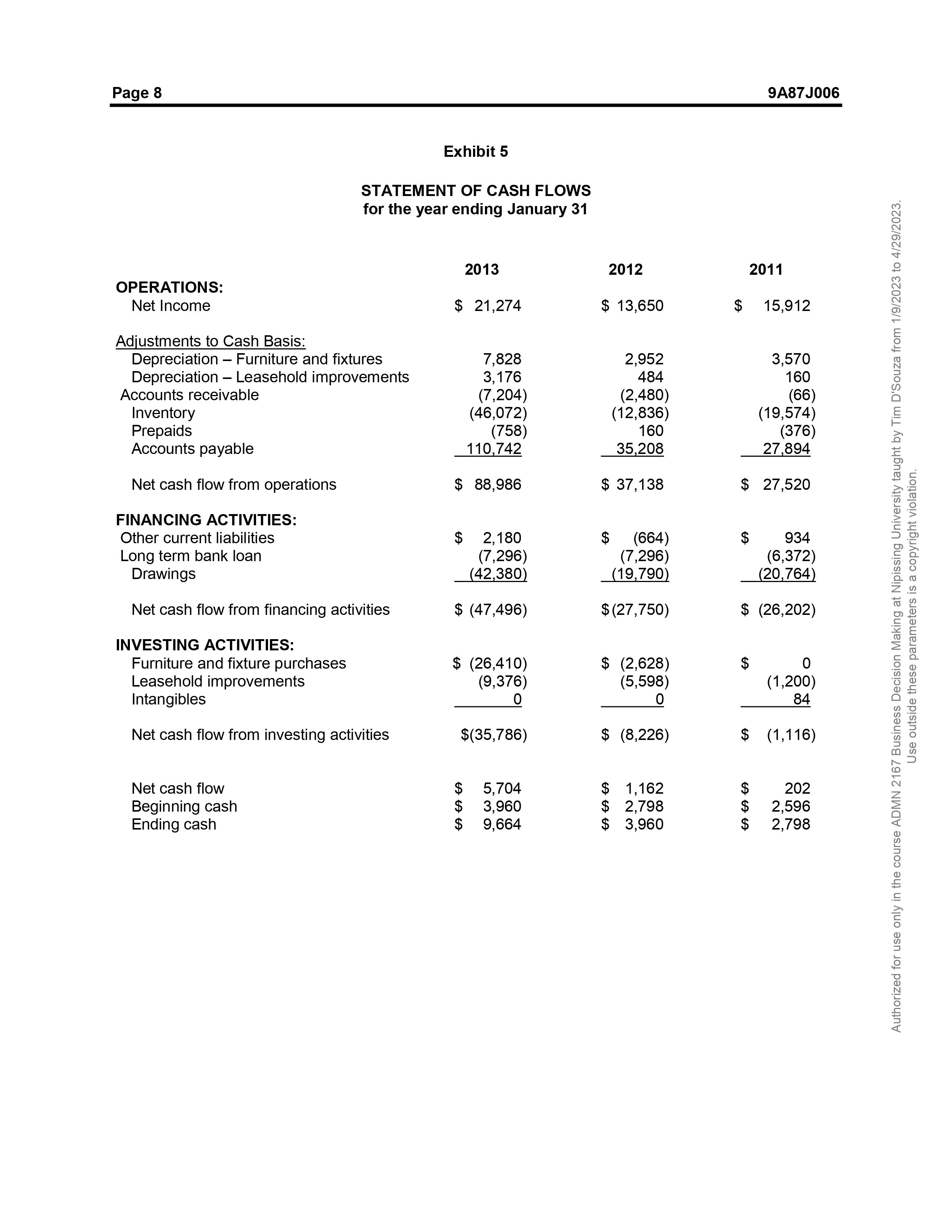

IVEY Publishing 9A87 JO06 LAWSONS Peter Farrell wrote this case under the supervision of Richard H. Mimick solely to provide material for class discussion. The authors do not intend to illustrate either effective or ineffective handling of a managerial situation. The authors may have disguised certain names and other identifying information to protect confidentiality. This publication may not be transmitted, photocopied, digitized or otherwise reproduced in any form or by any means without the permission of the copyright holder. Reproduction of this material is not covered under authorization by any reproduction rights organization. To order copies or request permission to reproduce materials, contact Ivey Publishing, Ivey Business School, Western University, London, Ontario, Canada, N6G ON1; (t) 519.661.3208; (e) cases@ivey.ca; www.iveycases.com. Copyright @ 1999, Richard Ivey School of Business Foundation Version: 2015-06-03 "I think I have all the information needed for your request Mr. Mackay. Give me a couple of days to come up with a decision and I'll contact you one way or another - good day!" So said Jackie Patrick, a newly appointed loans officer for the Commercial Bank of Ontario. She was addressing Paul Mackay, sole proprietor of Lawsons, a general merchandising retailer in Riverdale, Ontario. He had just requested a $194,000 bank loan to reduce his trade debt, as well as a $26,000 line of credit to service his tight months of cash shortage. Jackie felt she was fully prepared to scrutinize all relevant information in order Use outside these parameters is a copyright violation. Authorized for use only in the course ADMN 2167 Business Decision Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023 to make an appropriate decision. Her appointment as loans officer, effective today, February 18, 2013, was an exciting opportunity for her as she had been preparing for this position for some time. LAWSONS Lawsons had been operating in Riverdale for nearly five years. Mackay felt that his store stressed value at competitive prices, targeting low to middle income families. The store offered a wide range of products in various categories such as: infants', children's and youths' wear ladies' wear men's wear accessories (footwear, pantyhose, jewellery, etc.) . . . home needs (domestics, housewares, notions, yarn, stationery) toys, health and beauty aids seasonal items (Christmas giftwrap and candy) To help finance the start up of the business in 2008, Mackay secured a long-term loan from the Commercial Bank of Ontario at the prime lending rate plus 1.5 per cent. As Mackay's personal assets were insufficient for security, the bank loan had been secured by a pledge against all company assets, and by a guarantee from Lawsons' major supplier, Forsyth Wholesale Lid. (FWL). Mackay's store, with the exception of its first partial year, had always generated positive earnings. However, after drawings, Mackay's equity in the firm decreased each year to its present level ofPage 2 9A87J006 ($18,914). Exhibits 1, 2, and 3 present Lawsons' statements of earnings, balance sheets and selected nancial ratios. Exhibit 4 presents selected industry ratios. PURCHASING PROCEDURES Mackay purchased most of his inventory from FWL, a wholesaler who dealt in the product categories and merchandise that Mackay stocked in his store. Other stock, not supplied through FWL, was purchased directly from local suppliers. Through an arrangement with FWL, Mackay made his merchandising decisions at two annual trade shows in May and October. At the May show, Mackay decided on back-to- school supplies, Christmas merchandise, and fall and winter clothing. Spring and summer merchandise was decided upon at the October show. FWL's purchasing agents accumulated all of the orders from the various retailers it dealt with and, as a large buying group, executed the orders and negotiated prices with the manufacturers. The merchandise was sent to FWL from the individual manufacturers and then was distributed to respective retail outlets, such as Lawsons. FWL required partial payment for this merchandise before the start of the particular selling season. The remainder was due in scheduled repayments throughout the selling season. Mackay was pleased with this arrangement that he had secured with FWL. He was convinced that his product costs were lower as a result. PAUL MACKAY Paul Mackay was 40 years old. He had immigrated to Canada in 2007 from his native England, where he had been employed by an insurance company as an accountant. Educationally, Mackay had completed a Business Economics degree at a military academy. When Mackay came to Canada, he admitted that he was unsure about what recognition he would receive for his previous labours, both corporate and educational. Consequently, Mackay embarked upon an entrepreneurial career. Candidly, Mackay expressed, \"I knew I wouldn't be satised in some corporate hierarchy I knew I needed to be in business for myself.\" In May 2008, a retail vacancy became available in Riverdale. Mackay seized this opportunity to turn his dream of independence into a reality, and opened Lawsons with the nancial backing of FWL. Mackay was an active resident of Riverdalc, often involving himself in community activities. He worked long hours at his store, performing both managerial and clerical duties. Frequently, Mackay could be seen in his store pricing and stocking goods, or bagging merchandise at the cash register. THE PROBLEM Low earnings and necessary owner withdrawals had contributed to Mackay's increasing trade debt. Past due amounts on trade debt were charged a penalty of 13.5 per cent interest. Mackay indicated that of the present $217,236 in trade debt, he was paying penalty interest on $193,668. All of the overdue trade debt was owed to FWL. It was this overdue debt that had prompted his loan request. Mackay knew that, if he could transfer this trade debt to some other form of debt with lower interest charges such as the requested bank loan, protability could be increased. Mackay indicated that the current portion of the trade debt would be an acceptable amount to carry for this time of year, which he estimated to be 17 days of purchases. Authorized for use only in the course ADMN 2167 Business Dectsion Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023. Use outside these parameters is a copyright violation. Page 3 9A87J006 The total trade debt had increased to its present level in scal 2013 when Mackay decided that additional retail space would increase sales volume. Mackay felt that his store size was too small to effectively display product lines and, therefore, decided that the expansion was a necessary step in the store's turnaround. Additional furniture, xtures, and leasehold improvements totalled $36,000, which was nanced by FWL and added to Maekay's trade debt. Mackay explained that FWL nanced the improvements at Lawsons because it was interested in Mackay improving to the point where he could start paying off the trade debt owed to it. At the time of the expansion, FWL's nancial director stated, \"If this expansion is a means towards debt repayment, and I believe it is, FWL is committed to nancing the expansion.\" To go along with this capital expenditure, a greater investment in inventory was needed. Sales results in 2013 indicated to Mackay that the expansion was helping to improve sales volume. Mackay believed that with his purchasing arrangements with FWL, a seasonal line of credit was necessary, so that he could manage the months with tight cash positions. February through June were months of cash outows with the total cumulative cash outows peaking at about four per cent of sales. Lawsons would therefore require the equivalent of four per cent of sales in extra cash during cash outow periods. PROJECTIONS Mackay did not anticipate any additional capital expenditures for some time, given the just-completed expansion. Sales growth of 10 per cent in each of the next two years was projected. With respect to interest charges, Mackay calculated that if less expensive debt could be found, Lawson's interest expense for all debt, including the proposed line of credit, would be $27,500 and $26,920 for 2014 and 2015, respectively. Store salaries were to remain constant as a dollar amount because of improved employee productivity. Mackay realized he had a great deal of money tied up inventory, but he hoped that, as he gained greater experience in handling the added sales volume, inventory could be reduced to pre-2013 levels. With respect to drawings, Mackay explained that due to his depleted savings, future withdrawals from the rm would be at the 2013 level. JACKIE PATRICK Patrick had hoped that her rst loan request in her new position would be straightforward. However, a closer look indicated that this request would certainly require careful attention and scrutiny. She suspected her superiors would be reviewing her rst series of recommendations carefully, given her newness in the position Authorized for use only in the course ADMN 2167 Business Decrsion Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023. Use outside these parameters is a copyright violation. Page 4 9A87J006 Exhibit 1 STATEMENTS OF EARNINGS for the Years Ending January 31 2013 2012 2011 2010 Sales 3 650,210 3 526,332 $ 507,778 3 425,398 Cost of goods sold 467 510 383 948 368,356 305 748 Gross profit 3 182,700 3 142,384 3 139,422 3 119,650 Operating expenses: Store salaries 3 44,578 3 41,234 3 38,154 3 29,818 Heat and utilities 8,888 8,524 7,022 7,324 Building maintenance and repairs 362 508 406 338 Rent and property tax 23,992 24,710 28,364 28,364 Insurance and taxes 6,922 3,454 4,708 5,934 Depreciation: Furniture and fixtures 7,828 2,952 3,570 6,374 Leaseholds 3,176 484 160 Other operating expenses 27,692 26,112 23,840 14,016 Interest: Long-term debt 8,418 9,280 11,332 11,418 Trade debt 29 570 11 476 5,954 4 724 Total expenses 3 161 426 3 128 734 $ 123,510 $ 108 310 Net earnings 3 21 274 3 13 650 3 15,912 3 11 340 Authorized for use only in the course ADMN 2167 Business Dectsion Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023. Use outside these parameters is a copyright violation. Page 5 9A87J006 Exhibit 2 BALANCE SHEETS as at January 31 2013 2012 2011 2010 ASSETS Current assets: Cash 3 9,664 3 3,960 $ 2,798 $ 2,596 Accounts receivable 12,028 4,824 2,344 2,278 Inventory 199,700 153,628 140,792 121,218 Prepaids 3 760 3 002 3,162 2 786 Total current assets 3 225,152 $ 165,414 $ 149,096 $ 128,878 Fixed assets: Furniture and fixtures, cost $ 61,200 3 34,792 $ 32,164 $ 32,164 Less: accumulated depreciation 28 662 20 836 17,884 14 314 Net furniture and fixtures $ 32,538 3 13,956 $ 14,280 $ 17,850 Leaseholds, cost 3 16,174 $ 6,798 $ 1,200 $ Less: accumulated depreciation 3 820 644 160 Net Leaseholds 3 12 354 3 6 154 3 1,040 3 Total fixed assets 3 44,892 $ 20,110 $ 15,320 $ 17,850 Intangibles 84 Total Assets 3 270 044 3 185 524 3 164,416 3 146 812 LIABILITIES AND PROPRIETOR'S CAPITAL Liabilities Current liabilities: Accounts payable $ 217,236 $ 106,494 $ 71,286 $ 43,392 Other current liabilities 2 450 270 934 Total current liabilities $ 219,686 3 106,764 $ 72,220 $ 43,392 Long-term bank loan 68 872 76 168 3 83,464 89 836 Total liabilities $ 288,558 $ 182,932 $ 155,684 $ 133,228 Proprietor's Capital Balance, beginning of year $ 2,592 $ 8,732 $ 13,584 $ 21,152 Add: net earnings 21 274 13 650 15,912 11 340 Subtotal $ 23,866 $ 22,382 $ 29,496 $ 32,492 Less: drawings 42 380 19 790 20,764 18 908 Balance, end of year 3 (18,514) $ 2 592 $ 8,732 $ 13 584 Total Liabilities and Proprietor's Capital 3 270 044 3 185 524 3 164,416 3 146 812 Authorized for use only In the course ADMN 2167 Business Decrsion Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023. Use outside these parameters is a copyright violation. Page 6 9A87J006 Exhibit 3 RATIO ANALYSIS 2013 2012 2011 2010 PROFITABILITY Vertical analysis: Sales 100.0% 100.0% 100.0% 100.0% Cost of goods sold 71.9% 72.9% 72.5% 71.9% Gross profit 28.1% 27.1% 27.5% 28.1% Operating expenses: Store salaries 6.9% 7.8% 7.5% 7.0% Heat and utilities 1.4% 1.6% 1.4% 1.7% Building maintenance and repairs 0.1% 0.1% 0.1% 0.1% Rent and property tax 3.7% 4.7% 5.6% 6.7% Insurance and taxes 1.1% 0.7% 0.9% 1.4% Depreciation: Furniture and fixtures 1.2% 0.6% 0.7% 1.5% Leaseholds 0.5% 0.1% Interest: Long-term debt 1.3% 1.8% 2.2% 2.7% Trade debt 4.6% 2.2% 1.2% 1.1% Other operating expenses 4.3% 5.0% 4.7% 3.3% Total operating expenses 25.1% 24.6% 24.3% 25.5% Net earnings 3.3% 2.6% 3.2% 2.6% Return on equity N/A 241.1% 142.6% 83.5% LIQUIDITY Current ratio 1.02:1 1.55:1 2.06:1 2.97:1 Acid test ratio 0.10:1 0.08:1 0.07:1 0.11:1 Working capital $5,466 $58,650 $76,876 $85,486 EFFICIENCY (Based on 365-day year) Age of receivables 7 days 3 days 2 days 2 days Age of inventory 156 days 146 days 140 days 145 days Age of payables1 154 days 98 days 67 days 55 days Fixed asset turnover 20.0X 29.7X 30.6X 23.8X STABILITY Net worth/total assets N/A 1.4% 5.3% 9.3% Interest coverage 1.6X 1.7X 1.9x 1.7X 2012-13 2011-12 2010-11 GROWTH Sales 23.5% 3.7% 9.4% Net profit 55.9% (14.2%) 40.3% Total assets 45.6% 12.8% 12.0% Net worth N/A (70.3%) (35.7%) 1Aging is based on purchases, which are equal to cost of goods sold plus ending inventory less beginning inventory. Authorized for use only in the course ADMN 2167 Business Decrsion Making at Nipissing University taught by Tim D'Souza from 1(9/2023 to 4/29/2023. Use outside these parameters is a copyright violation. Page 7 9A87 J006 Exhibit 4 DUN & BRADSTREET CANADIAN NORMS & KEY BUSINESS RATIOS Industry: Retail - Miscellaneous Products 2012 PROFITABILITY Net earnings 2.1% Return on equity 31.6% LIQUIDITY Current ratio 1.8:1 Acid test 1.1:1 EFFICIENCY Age of receivables 9.1 days Age of inventory 125.7 days STABILITY Net worth: Total assets 61.5% Use outside these parameters is a copyright violation. Authorized for use only in the course ADMN 2167 Business Decision Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023Page 8 9A87J006 Exhibit 5 STATEMENT OF CASH FLOWS for the year ending January 31 2013 2012 2011 OPERATIONS: Net Income $ 21,274 $ 13,650 $ 15,912 Adiustments to Cash Basis: Depreciation Furniture and fixtures 7,828 2,952 3,570 Depreciation Leasehold improvements 3,176 484 160 Accounts receivable (7,204) (2,480) (66) Inventory (46,072) (12,836) (19,574) Prepaids (758) 160 (376) Accounts payable 110 742 35,208 27,894 Net cash flow from operations :5 88,986 $ 37,138 $ 27,520 FINANCING ACTIVITIES: Other current liabilities $ 2,180 $ (664) $ 934 Long term bank loan (7,296) (7,296) (6,372) Drawings (42 380) (19,790) (20,764) Net cash flow from financing activities $ (47,496) $(27,750) $ (26,202) INVESTING ACTIVITIES: Furniture and fixture purchases $ (26,410) $ (2,628) $ 0 Leasehold improvements (9,376) (5,598) (1,200) Intangibles 0 0 84 Net cash flow from investing activities $(35,786) $ (8,226) $ (1,116) Net cash flow $ 5,704 $ 1,162 $ 202 Beginning cash $ 3,960 $ 2,798 $ 2,596 Ending cash $ 9,664 $ 3,960 $ 2,798 Authorized for use only in the course ADMN 2167 Business Decrsion Making at Nipissing University taught by Tim D'Souza from 1/9/2023 to 4/29/2023. Use outside these parameters is a copyright violation. What would be your recommendation(s) on the loan request? Would you make any recommendations to Mackay

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance