Question

Jane Nkosi is a 38-year-old resident of the Republic of South Africa and holds the position of marketing director at Brandrush Agency (Pty) Ltd. Her

Jane Nkosi is a 38-year-old resident of the Republic of South Africa and holds the position of

marketing director at Brandrush Agency (Pty) Ltd. Her spouse, Jabu, suffered a paralyzing injury from

a motor vehicle accident three years ago. They are married under an ante nuptial contract and have

two minor daughters. Below are the relevant details for the 2024 year of assessment:

1) Jane received a monthly basic salary of R53 000.

2) She received an annual bonus of R53 000 on 15 December 2023.

3) Brandrush Agency (Pty) Ltd contributes 40% of her medical scheme contributions, with Jane

covering the remaining portion. The total contributions to the medical scheme for the year

amounted to R85 500. Notably, Jane incurred qualifying expenses of R78 320 that were not

covered by her medical scheme. Jane is the principal member of the medical aid, with her

husband and children as dependants.

4) Jane and her family reside in a house owned by her employer. The house has 3 bedrooms and

was provided to Jane unfurnished. She pays for her own electricity. Her remuneration proxy for

the 2023 year of assessment was R485 250.

5) Brandrush Agency (Pty) Ltd owns a holiday apartment in Margate with three bedrooms, a

spacious lounge, a dining room, a well-equipped kitchen, and two bathrooms. Employees are

occasionally granted the privilege to use the apartment for their vacations. Jane and her family

enjoyed an 11-day stay during the December school holidays without any rental costs. When the

apartment is not occupied by employees, it is leased out at a daily rate of R750.

6) Jane has always been passionate about supporting social causes and has made the following

donations during the year:

R80 000 to a reputable non-profit organisation that focuses on providing education and

resources to underprivileged children. Jane received an official section 18A certificate from

the organisation.

R15 000 to her spouse, Jabu, for his birthday.

A car that had cost Jane R110 000 (three years ago) was given to her closest friend, Zama.

The car had a market value of R70 000 on the date of the donation.

7) In addition to her earnings as a marketing director, Jane received the following investment

income during the year of assessment:

1) Interest from a money market account with a major bank in South Africa totalling R25 950.

2) Interest from a tax-free investment amounting to R4 120.

3) South African dividends paid into her bank account totalling R36 780.

4) Rental income of R72 000 earned from an investment property she owns.

5) Jane incurred the following expenses directly related to the investment property:

a. Property taxes and levies amounting to R45 870.

b. Advertising fees of R2 000 to attract a potential tenant.

c. Renovations costing R145 000, which involved converting the veranda into a half

bedroom to enhance the property's marketability.

8) When Jane purchased the investment property on 01 June 2023, she approached her employer

to assist her with financing. While Brandrush Agency (Pty) Ltd is not a financial institution, they

agreed to provide Jane with a loan of R120 000 at an interest rate of 3.25% on the same date. In

May 2023, the Reserve Bank had announced that the repurchase rate is 8,25%.

9) The total employees tax that was deducted from Janes earnings during the year of assessment

amounted to R112 000.

Required:

Q.1.1 Calculate the amount still due by Jane Nkosi to the South African Revenue

Services for the year of assessment ending 29 February 2024, after taking into

account any employees tax paid.

Show all your calculations.

State reasons for any amounts not included or deducted in your calculations.

Remember to structure your answer using the tax framework.

Round to the nearest rand.

please use this format

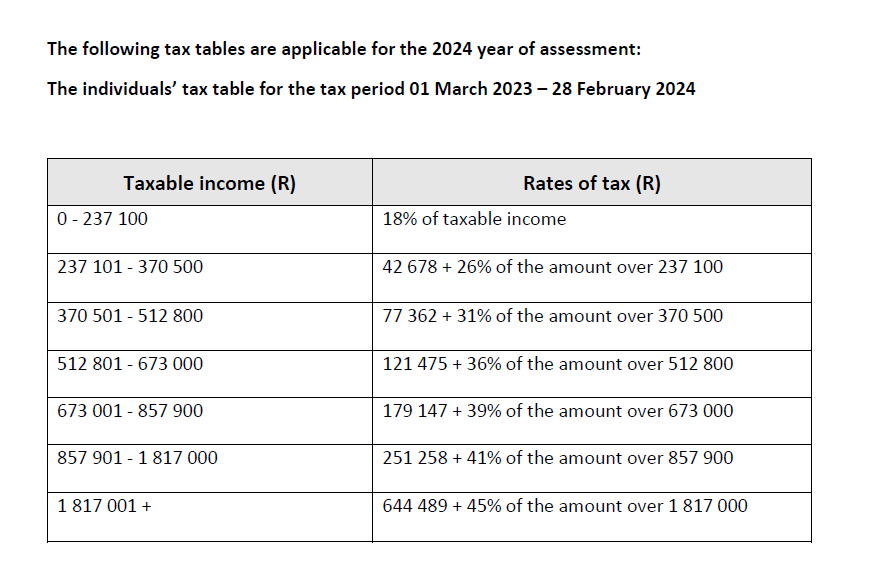

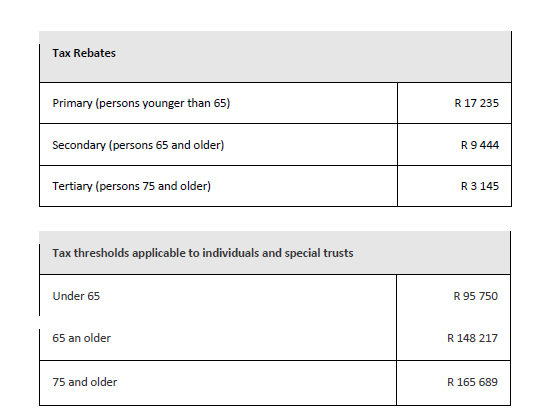

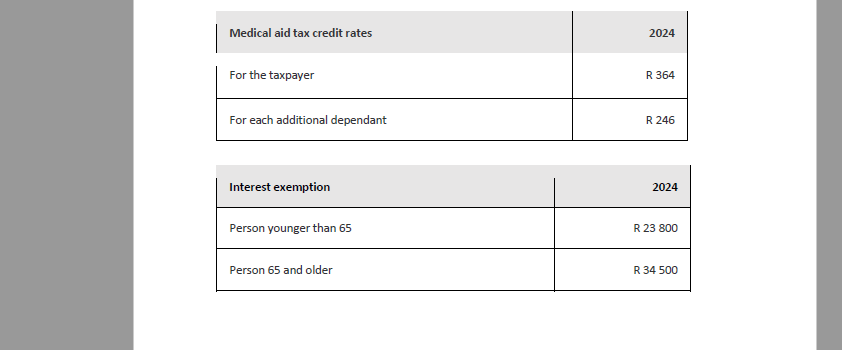

\begin{tabular}{|l|r|} \hline Tax Rebates \\ \hline Primary (persons younger than 65) & R 17235 \\ \hline Secondary (persons 65 and older) & R 9444 \\ \hline Tertiary (persons 75 and older) & R 3145 \\ \hline \end{tabular} \begin{tabular}{l|l|} Tax thresholds applicable to individuals and special trusts \\ \hline Under 65 & R 95750 \\ \hline 65 an older & R 148217 \\ \hline 75 and older & R 165689 \\ \hline \end{tabular} Medical aid tax credit rates For the taxpayer 2024 R 364 Interest exemption 2024 \begin{tabular}{|l|c|} \hline Person younger than 65 & R 23800 \\ \hline Person 65 and older & R 34500 \\ \hline \end{tabular} The following tax tables are applicable for the 2024 year of assessment: The individuals' tax table for the tax period 01 March 2023 - 28 February 2024 The basic formula for the calculation of income tax Gross income Less: Exempt income = Income Less: Deductions Add: Taxable portion of capital gains Less: Assessed loss carried forward from previous year = Taxable income Tax liability calculated using tax table Less: Rebates = Net normal tax payable Less: Prepaid expenses = Net tax due/(refundable) \begin{tabular}{|l|r|} \hline Tax Rebates \\ \hline Primary (persons younger than 65) & R 17235 \\ \hline Secondary (persons 65 and older) & R 9444 \\ \hline Tertiary (persons 75 and older) & R 3145 \\ \hline \end{tabular} \begin{tabular}{l|l|} Tax thresholds applicable to individuals and special trusts \\ \hline Under 65 & R 95750 \\ \hline 65 an older & R 148217 \\ \hline 75 and older & R 165689 \\ \hline \end{tabular} Medical aid tax credit rates For the taxpayer 2024 R 364 Interest exemption 2024 \begin{tabular}{|l|c|} \hline Person younger than 65 & R 23800 \\ \hline Person 65 and older & R 34500 \\ \hline \end{tabular} The following tax tables are applicable for the 2024 year of assessment: The individuals' tax table for the tax period 01 March 2023 - 28 February 2024 The basic formula for the calculation of income tax Gross income Less: Exempt income = Income Less: Deductions Add: Taxable portion of capital gains Less: Assessed loss carried forward from previous year = Taxable income Tax liability calculated using tax table Less: Rebates = Net normal tax payable Less: Prepaid expenses = Net tax due/(refundable)

\begin{tabular}{|l|r|} \hline Tax Rebates \\ \hline Primary (persons younger than 65) & R 17235 \\ \hline Secondary (persons 65 and older) & R 9444 \\ \hline Tertiary (persons 75 and older) & R 3145 \\ \hline \end{tabular} \begin{tabular}{l|l|} Tax thresholds applicable to individuals and special trusts \\ \hline Under 65 & R 95750 \\ \hline 65 an older & R 148217 \\ \hline 75 and older & R 165689 \\ \hline \end{tabular} Medical aid tax credit rates For the taxpayer 2024 R 364 Interest exemption 2024 \begin{tabular}{|l|c|} \hline Person younger than 65 & R 23800 \\ \hline Person 65 and older & R 34500 \\ \hline \end{tabular} The following tax tables are applicable for the 2024 year of assessment: The individuals' tax table for the tax period 01 March 2023 - 28 February 2024 The basic formula for the calculation of income tax Gross income Less: Exempt income = Income Less: Deductions Add: Taxable portion of capital gains Less: Assessed loss carried forward from previous year = Taxable income Tax liability calculated using tax table Less: Rebates = Net normal tax payable Less: Prepaid expenses = Net tax due/(refundable) \begin{tabular}{|l|r|} \hline Tax Rebates \\ \hline Primary (persons younger than 65) & R 17235 \\ \hline Secondary (persons 65 and older) & R 9444 \\ \hline Tertiary (persons 75 and older) & R 3145 \\ \hline \end{tabular} \begin{tabular}{l|l|} Tax thresholds applicable to individuals and special trusts \\ \hline Under 65 & R 95750 \\ \hline 65 an older & R 148217 \\ \hline 75 and older & R 165689 \\ \hline \end{tabular} Medical aid tax credit rates For the taxpayer 2024 R 364 Interest exemption 2024 \begin{tabular}{|l|c|} \hline Person younger than 65 & R 23800 \\ \hline Person 65 and older & R 34500 \\ \hline \end{tabular} The following tax tables are applicable for the 2024 year of assessment: The individuals' tax table for the tax period 01 March 2023 - 28 February 2024 The basic formula for the calculation of income tax Gross income Less: Exempt income = Income Less: Deductions Add: Taxable portion of capital gains Less: Assessed loss carried forward from previous year = Taxable income Tax liability calculated using tax table Less: Rebates = Net normal tax payable Less: Prepaid expenses = Net tax due/(refundable) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantum Economics And Finance

Authors: David Orrell

3rd Edition

1916081630, 978-1916081635