Question

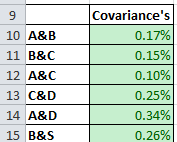

Josh is considering investing in four different two-factor portfolios. He is able to obtain the monthly returns of securities A, B , C and D

Josh is considering investing in four different two-factor portfolios. He is able to obtain the monthly returns of securities A, B , C and D for the years 2007 to 2014. In any of the possible two factor portfolios, the weight of each security in the portfolio will be 50%. The four possible portfolio combinations are A&B; B&C; A&C; C&D; A&D and B&D.

*Please use excel*

A.Calculate using the two-factor portfolio equations, the portfolio returns and risks (both standard deviation and variance) for the following portfolios: 1. A and B 2. B and C 3. A and C 4. C and D 5. A and D6. B and D

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultimate Beginners Guide To Understanding NFTs

Authors: LM Anderson

1st Edition

1739781732, 978-1739781736