JUST ANSWER THE FIRST PAGE: ALL INFO ARE ALREADY GIVEN PRESENT VALUE OF SIMPLE ANNUITY DUE EXAMPLE: Hope borrows money for the renovation of her

JUST ANSWER THE FIRST PAGE: ALL INFO ARE ALREADY GIVEN

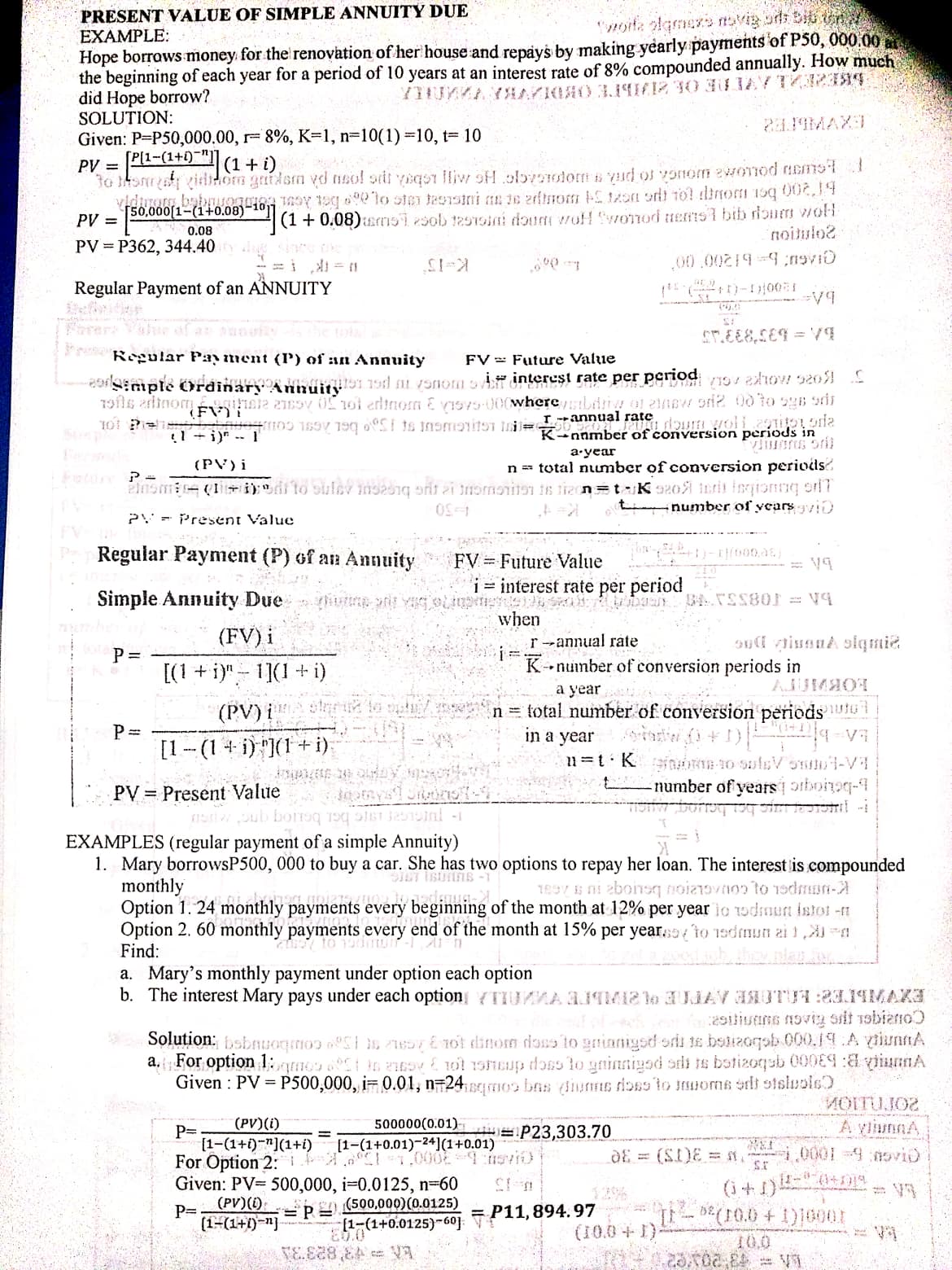

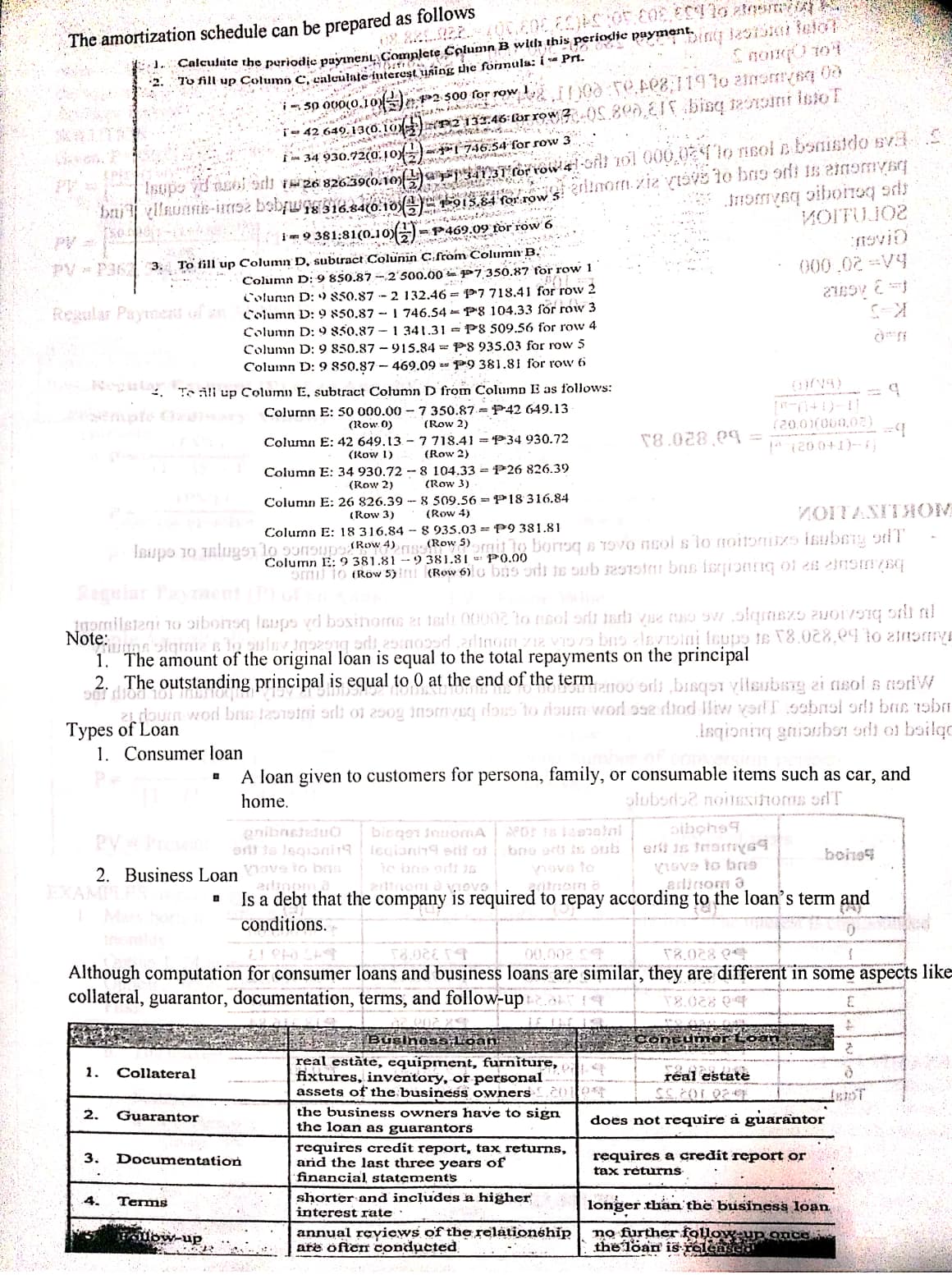

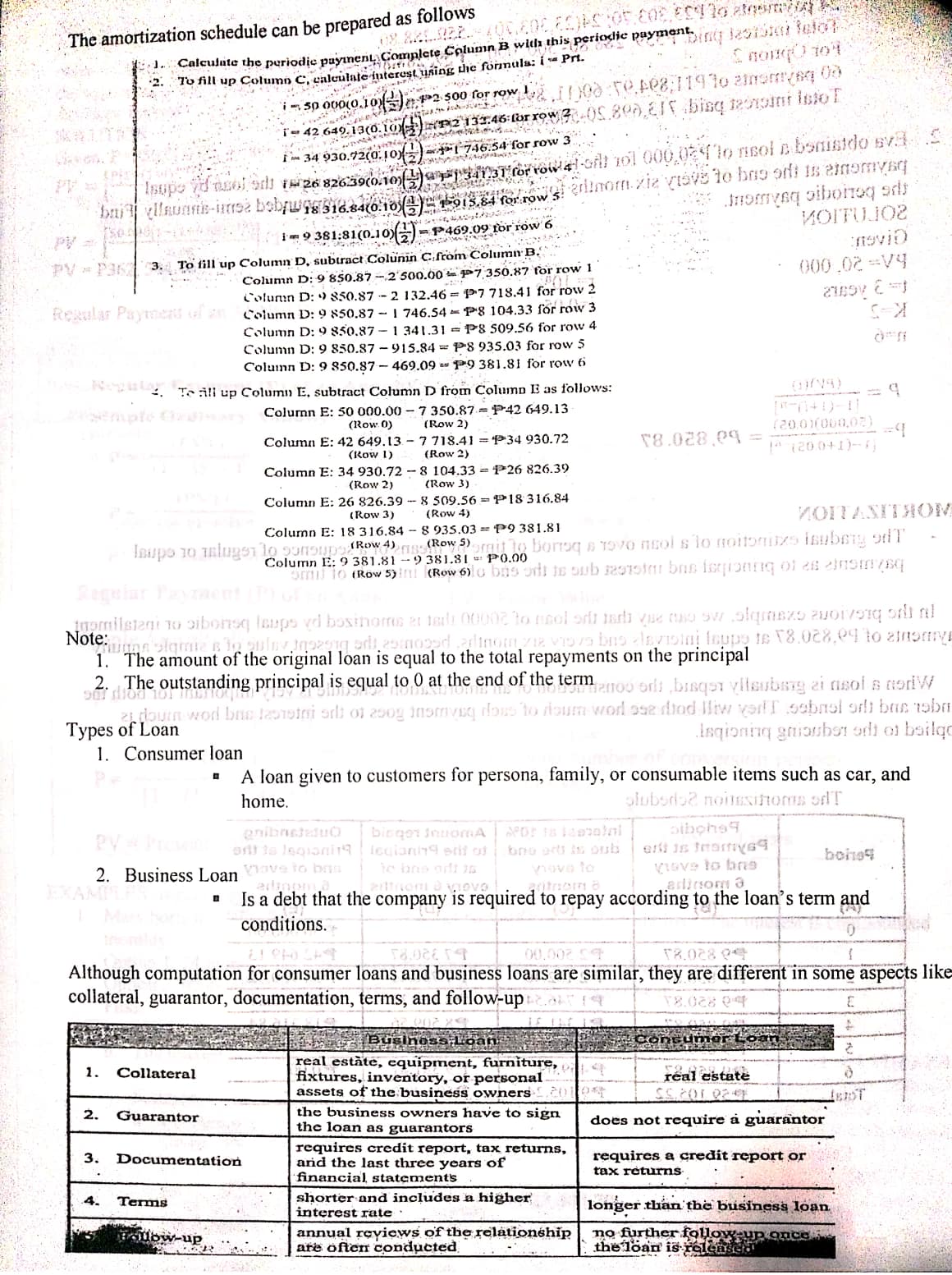

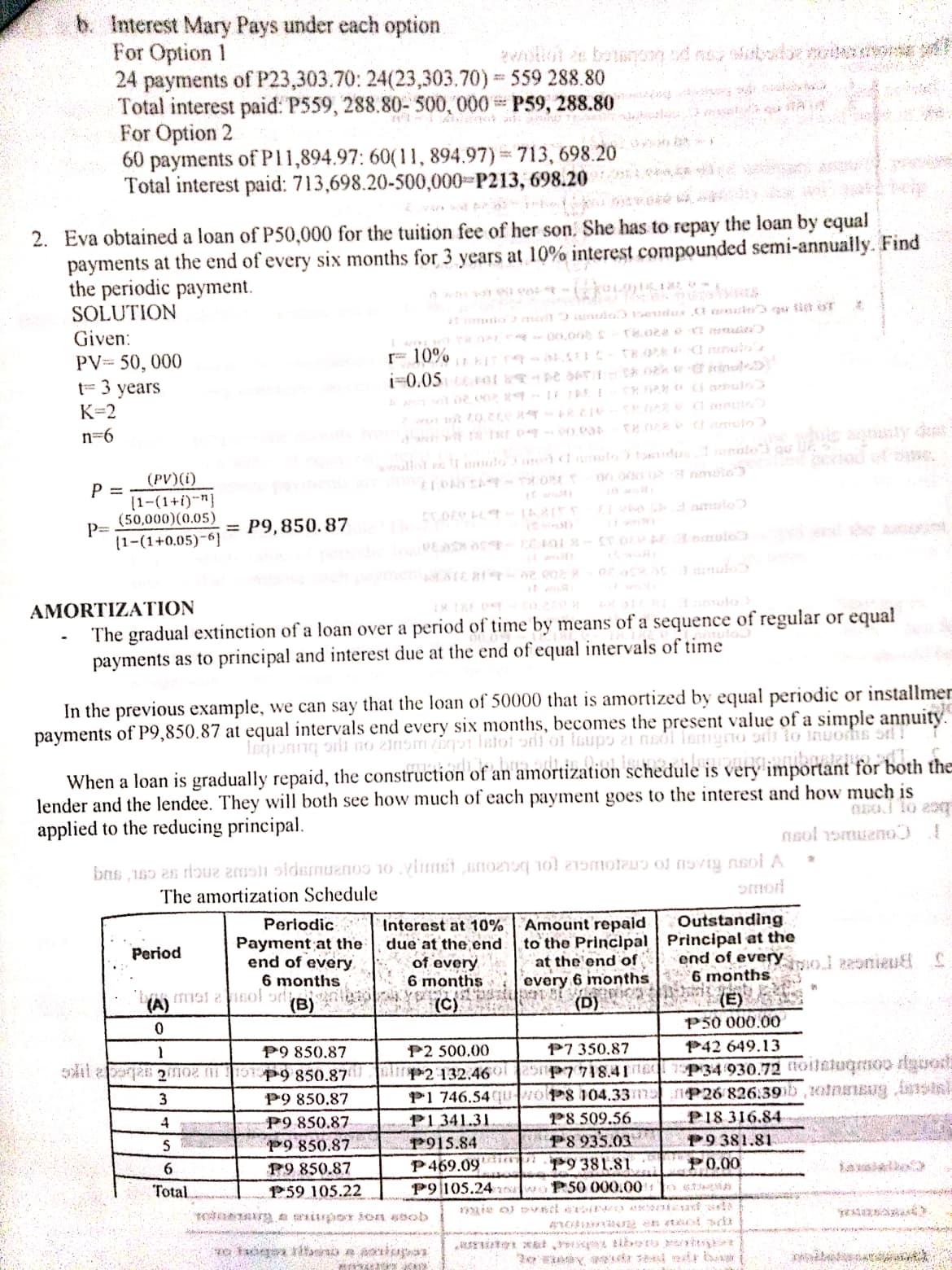

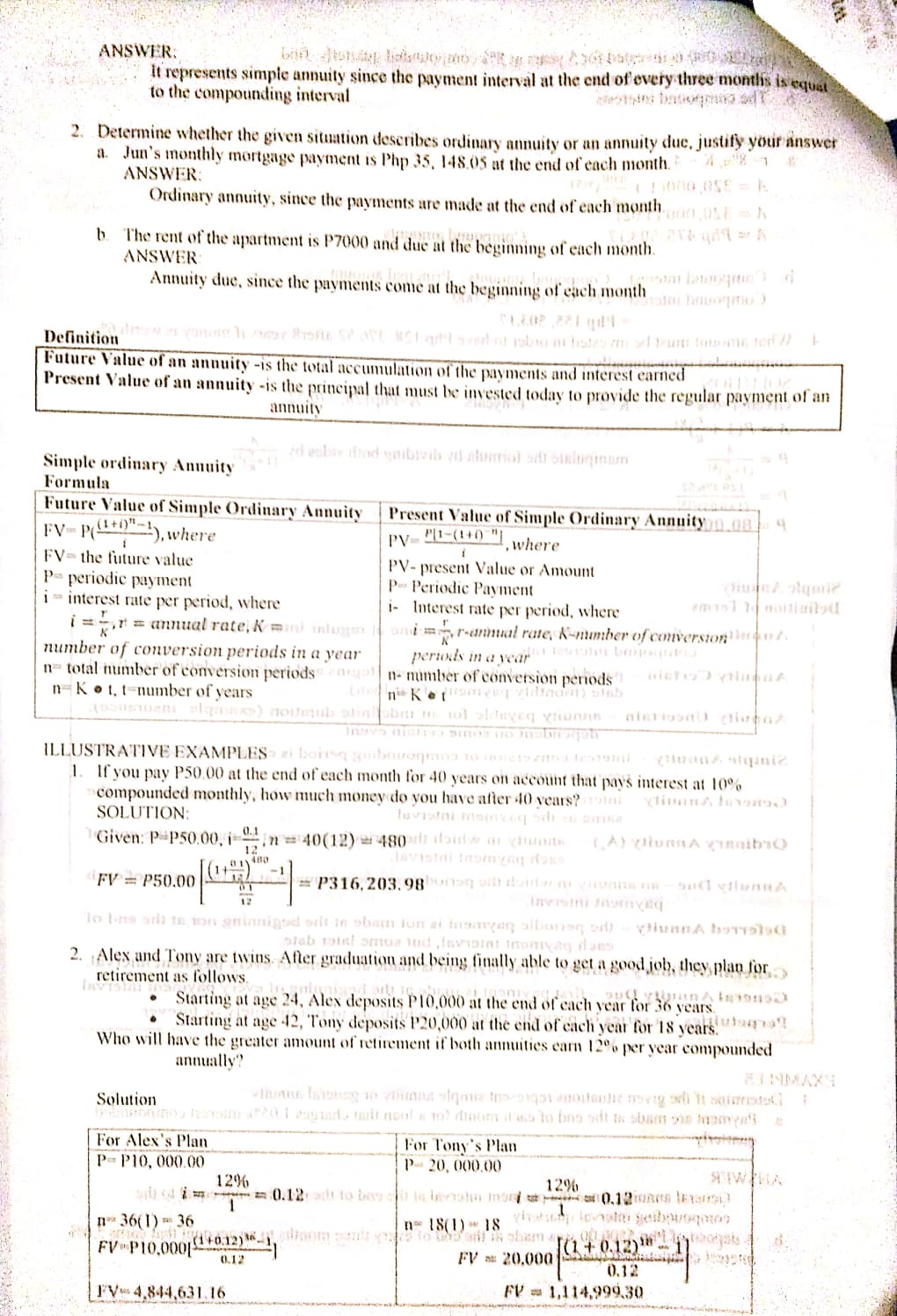

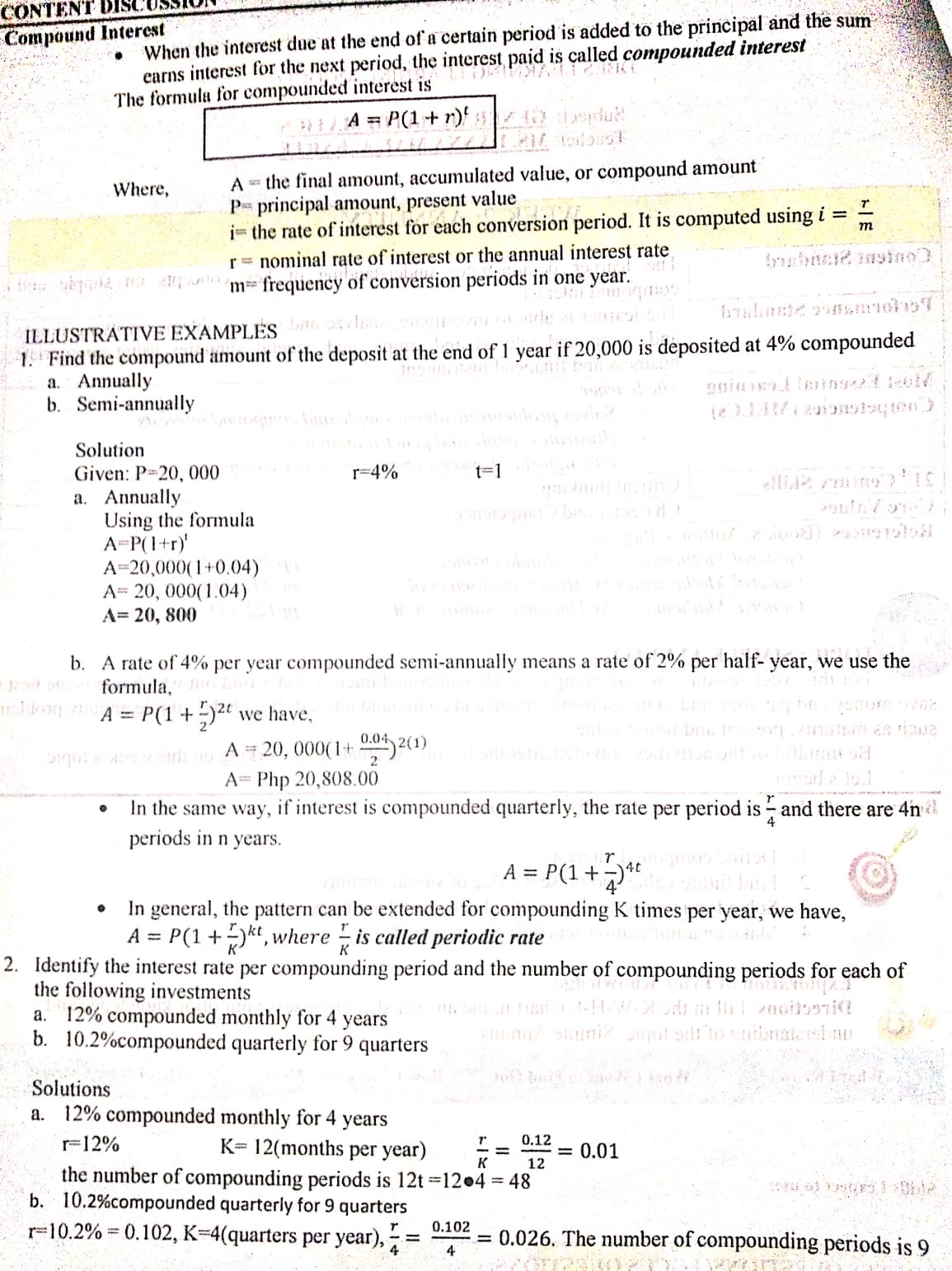

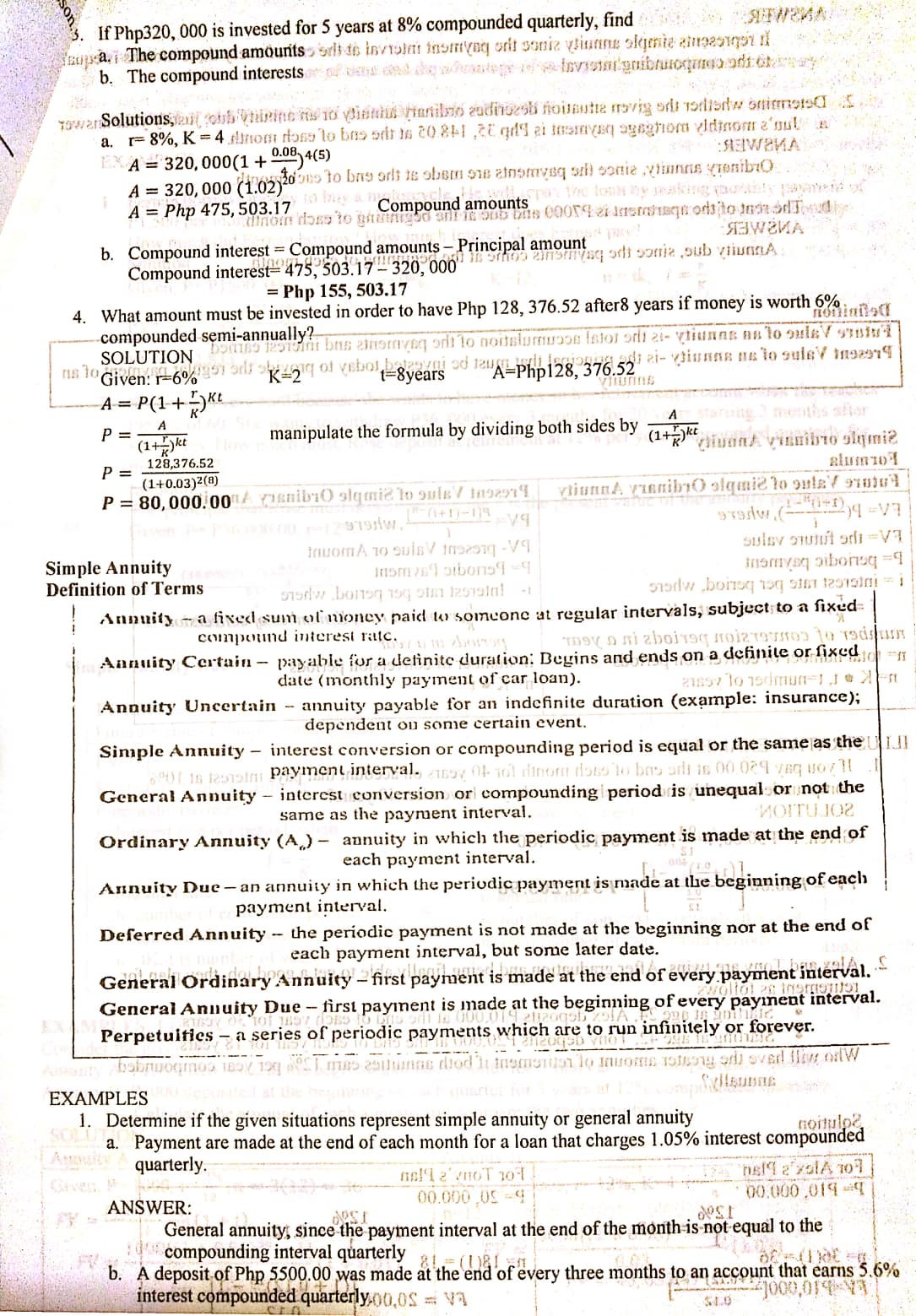

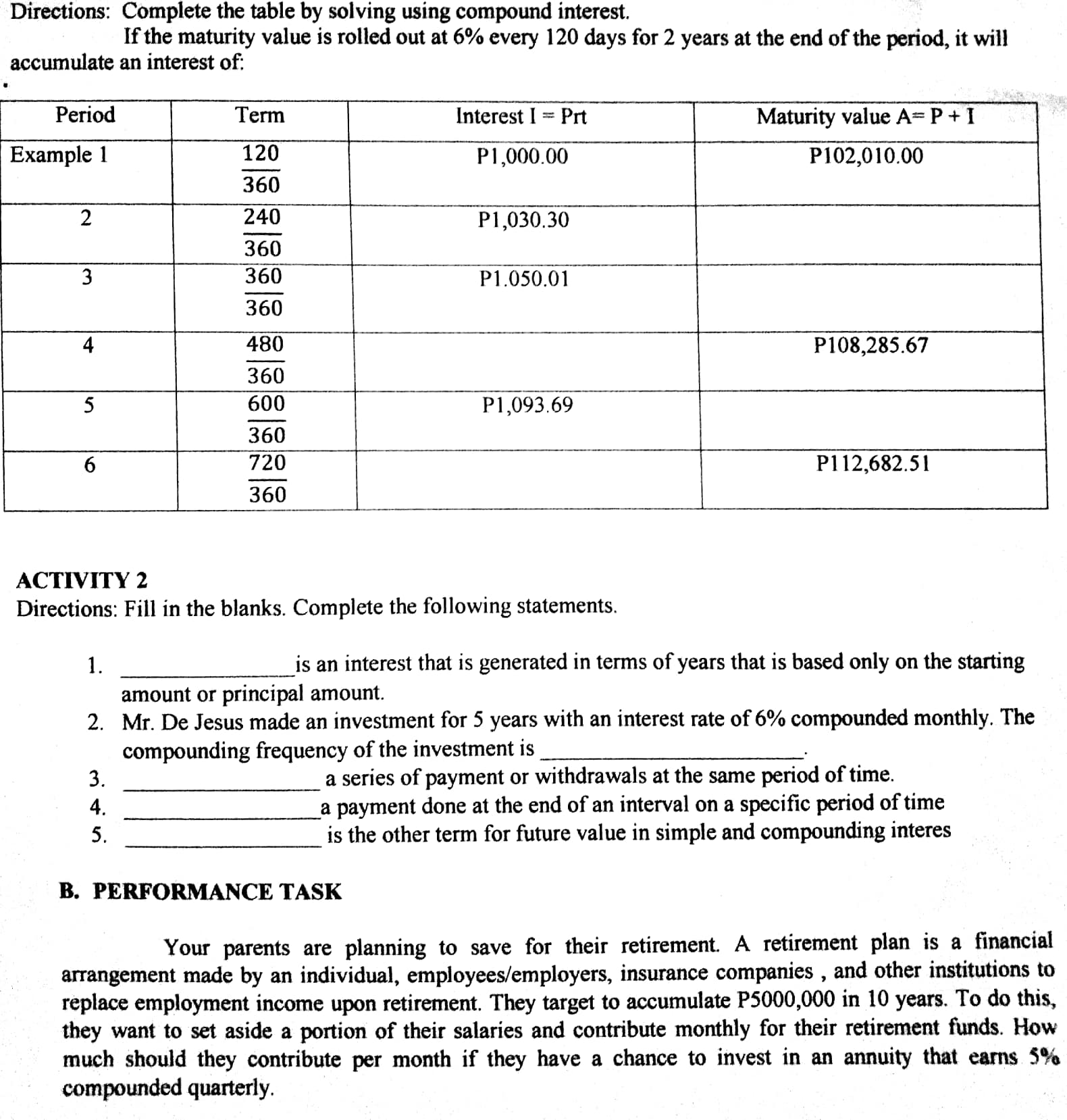

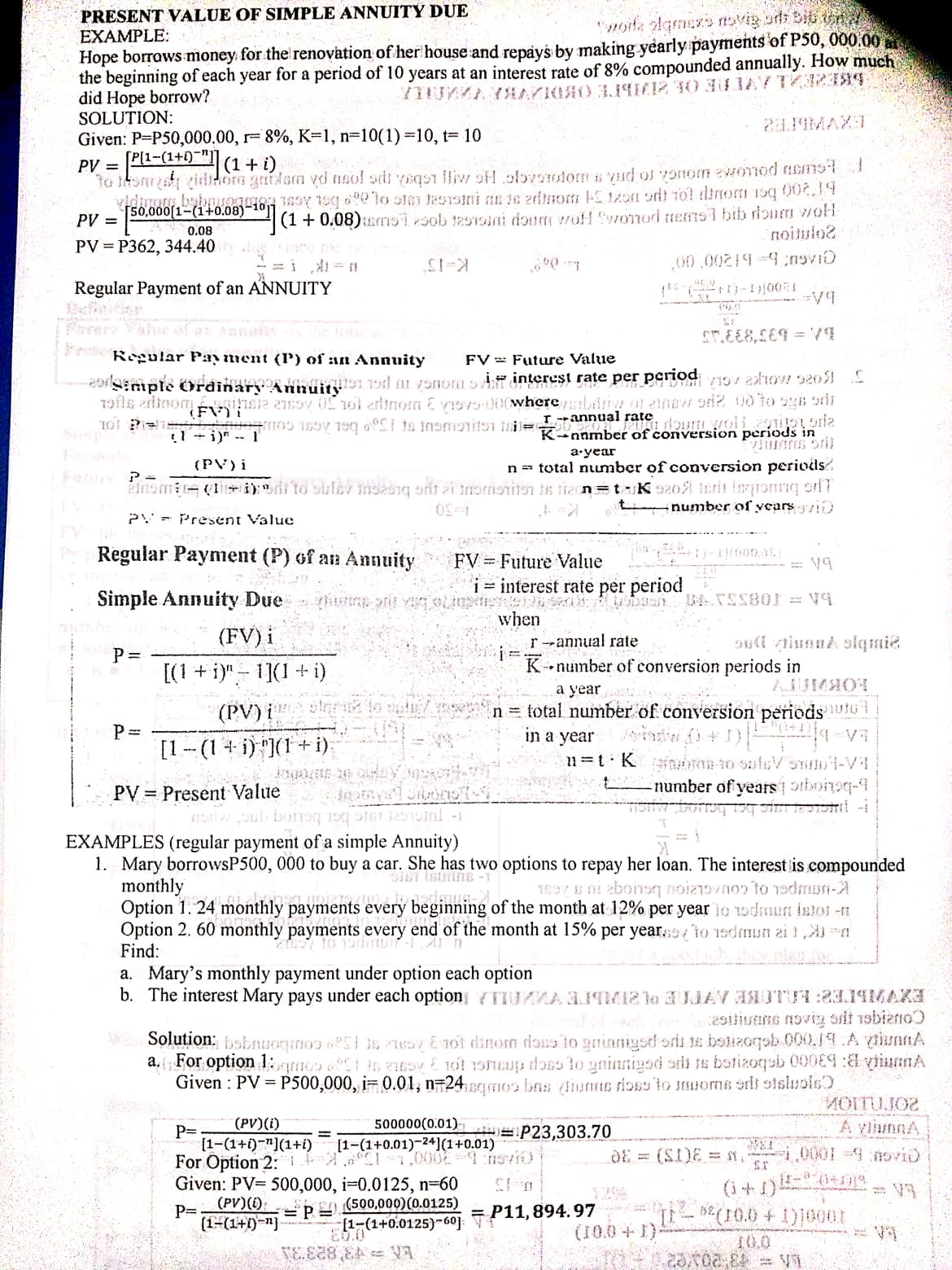

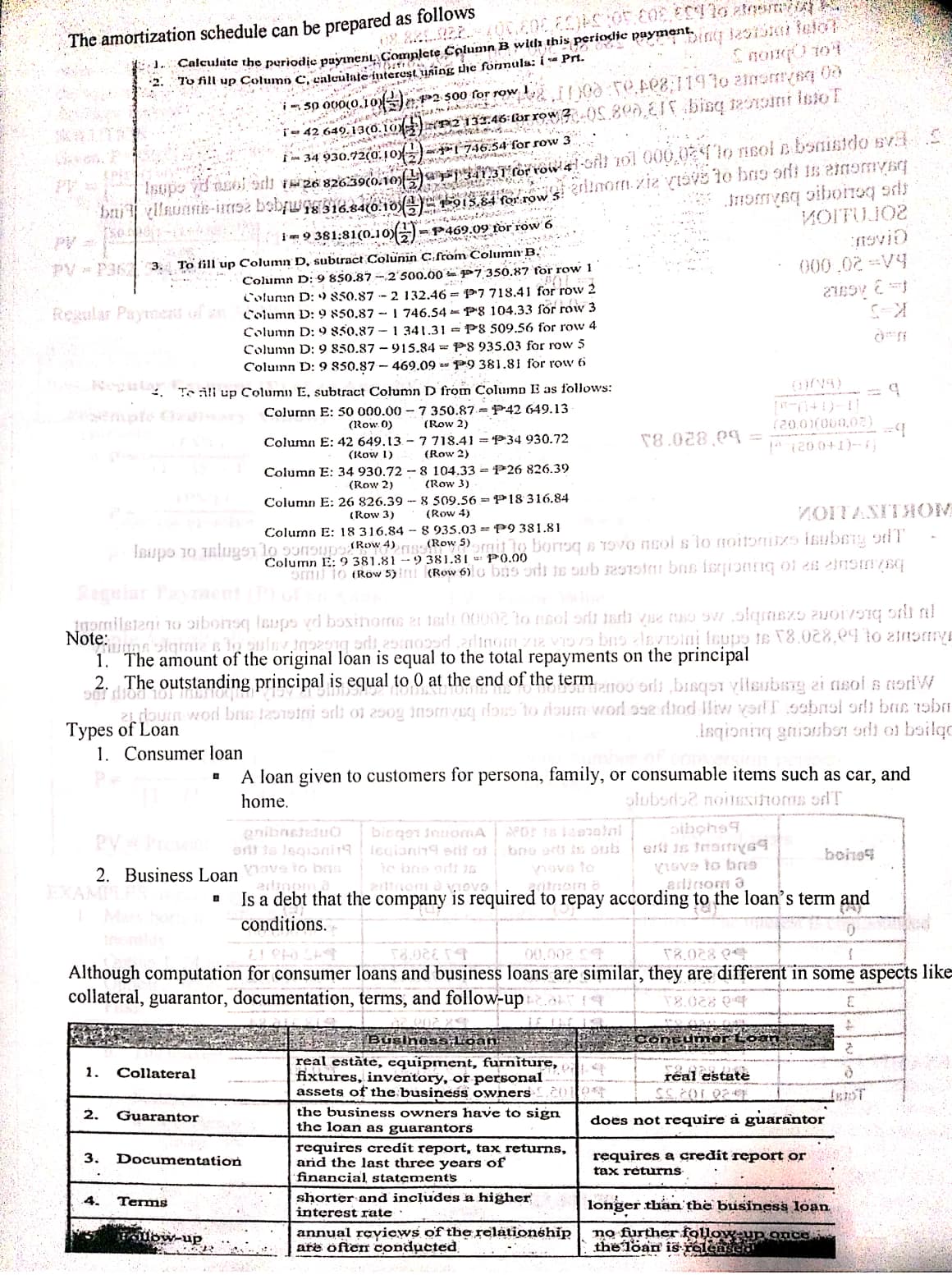

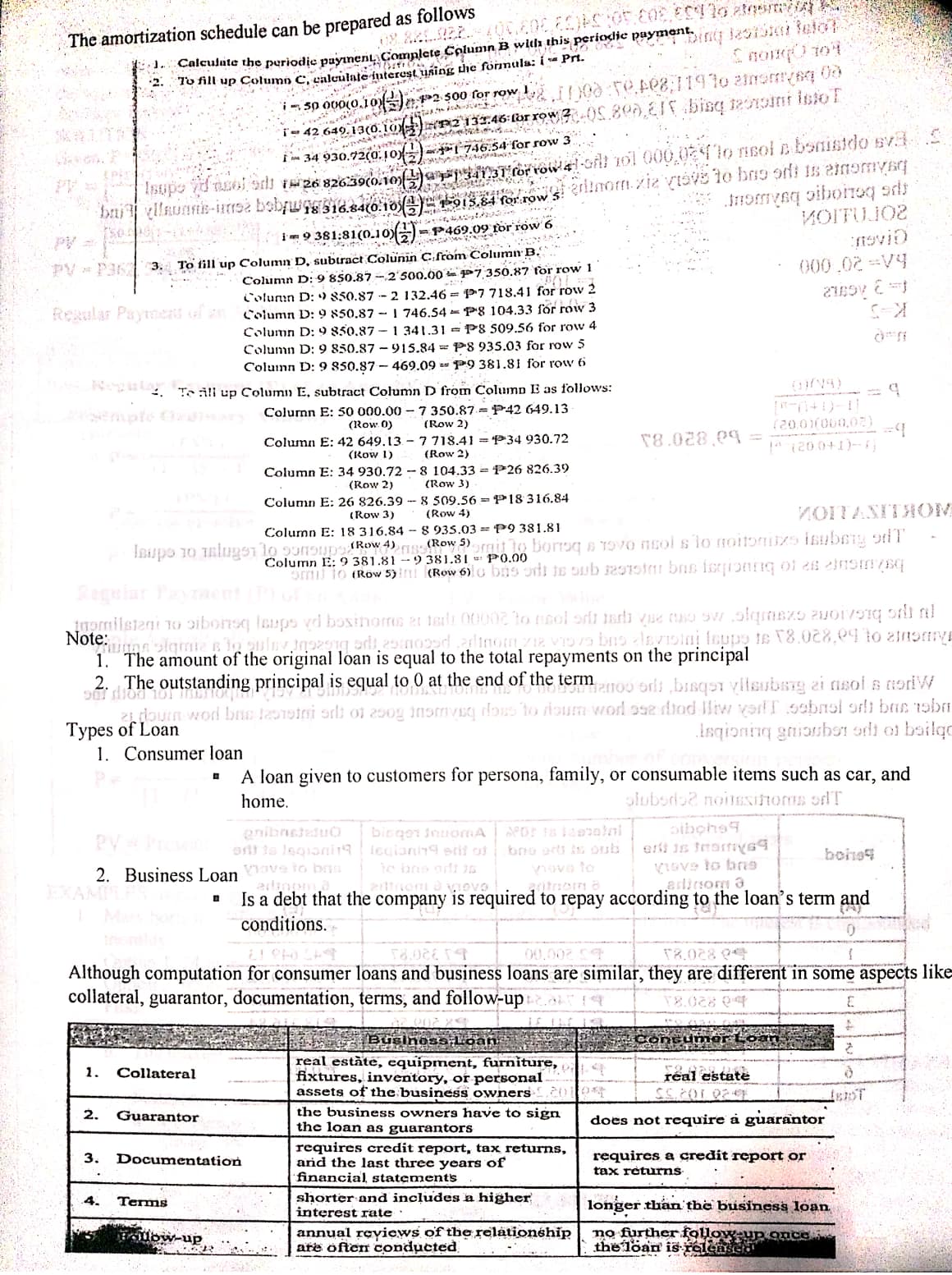

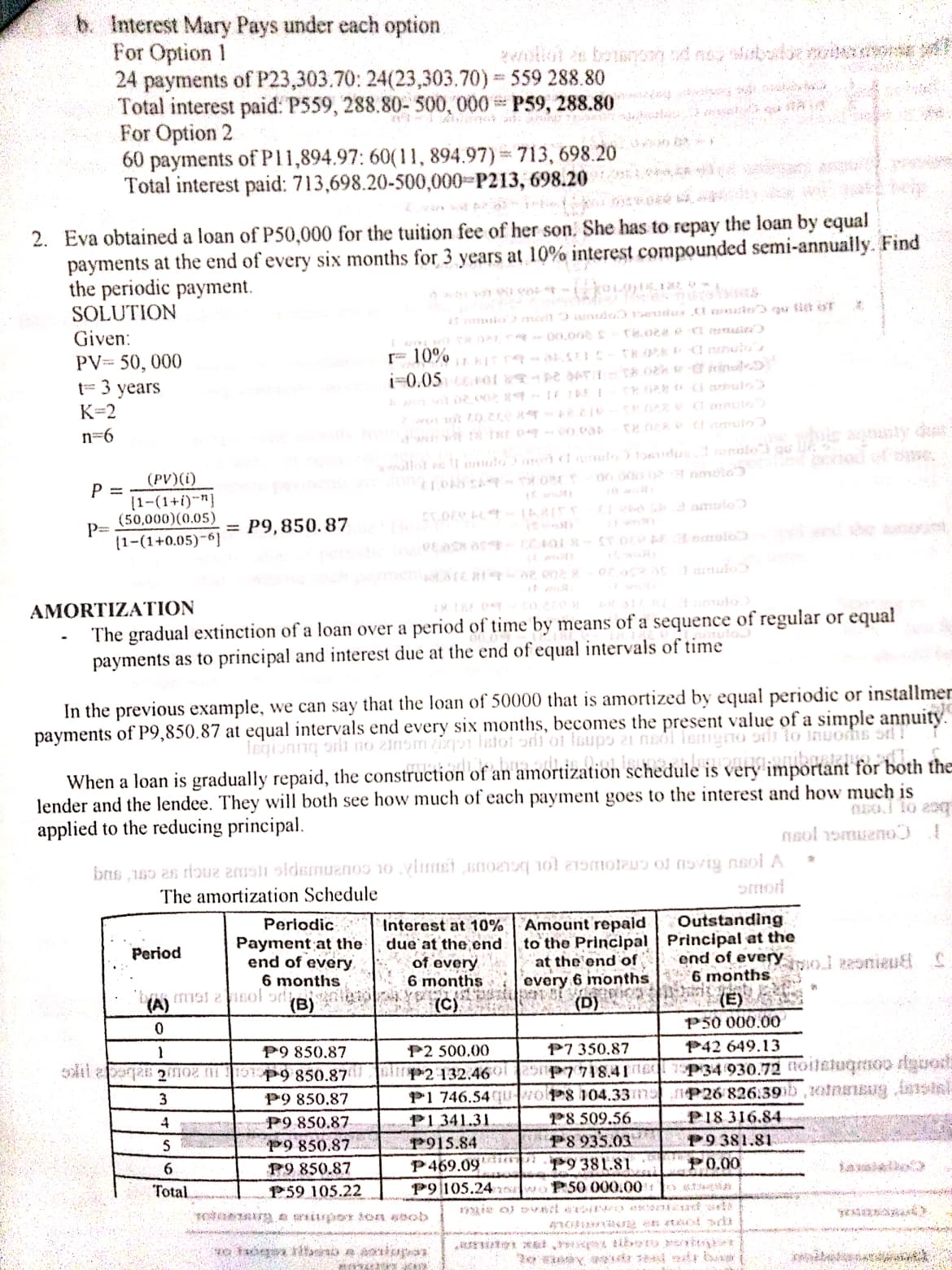

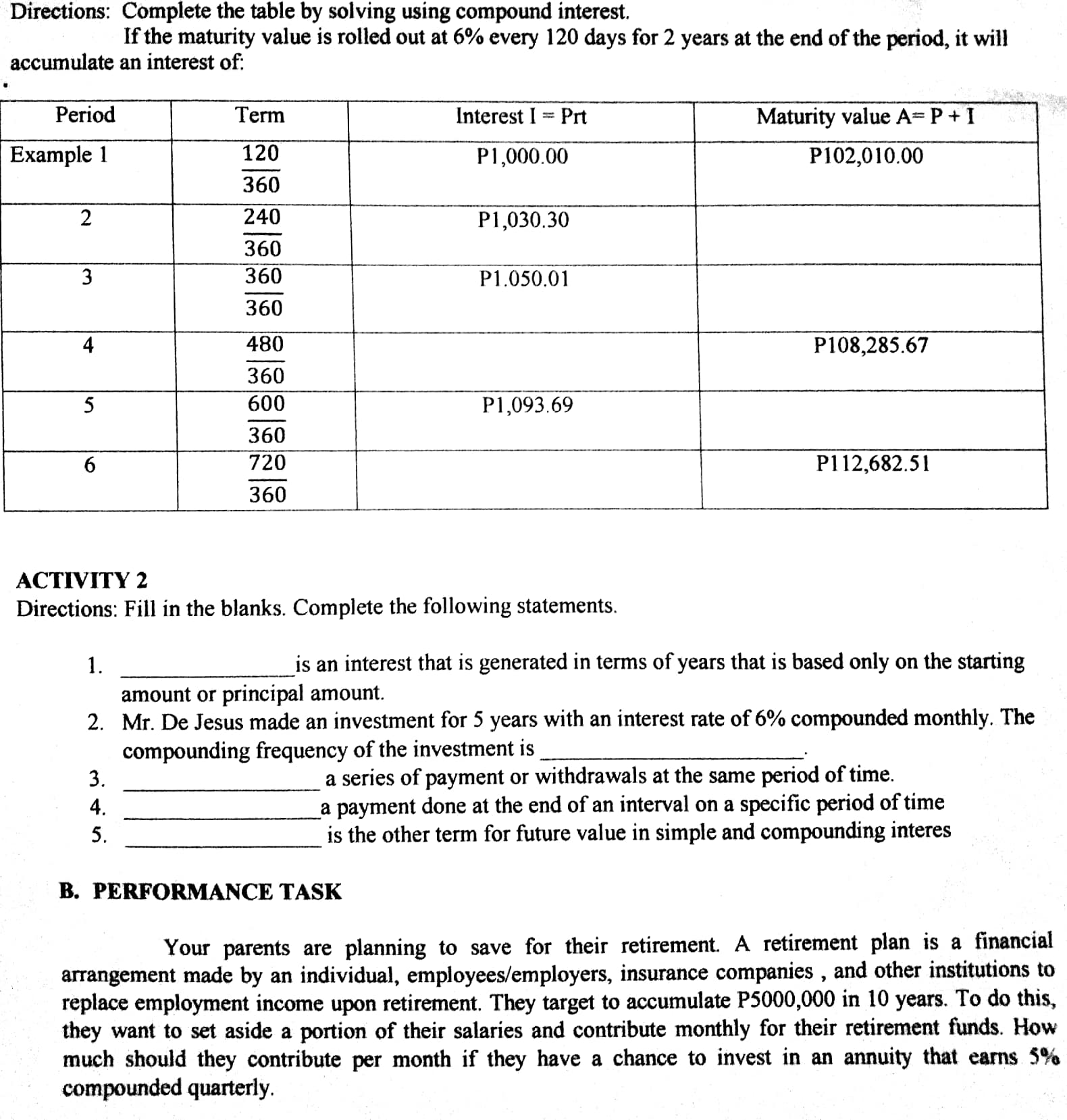

PRESENT VALUE OF SIMPLE ANNUITY DUE EXAMPLE: Hope borrows money for the renovation of her house and repays by making yearly payments of P50, 000.00 the beginning of each year for a period of 10 years at an interest rate of 8% compounded annually. How much did Hope borrow? SOLUTION: Given: P=P50,000.00, r= 8%, K=1, n=10(1) =10, t= 10 PATHMAXI PV = P(1-(1+0) " (1+i) How vidmom guidem vd no! and yeq Hiw of aboverooms wad of vonom ewonod nemat 1 PV = 50,000[1-(1+0.08)-101 (1 + 0.08) ams I esob resistal doun woll twonod nems'I bib ones woll 0.08 PV =P362, 344.40 nowlol = 1 ,MI= ,00 .00219 -9 :19V10 Regular Payment of an ANNUITY -Vq Free Regular Payment (P) of an Annuity FV = Future Value Simple Ordinary Annuity i and m /snom ,Li interest rate per period you show 9201 .[ 101 Bien Hmos 189v 19q off is insmonitor miez forannual rate in oum woll caution onda K-number of conversion periods in (PV) i a.year n = total number of conversion periods?. Plusmiss gift inwal to sblov insadiq of zi momonion is tieen= tak spod and Ingtoning off? PV = Present Value number of years JD Regular Payment (P) of an Annuity FV = Future Value =: Vq `i = interest rate per period Simple Annuity Due figure out yag outupmy USSBOT = Vq when (FV) i P = r -annual rate on givenA siqmie. [(1 + 1)" - 1](1 + i) K - number of conversion periods in a year n = total number of conversion periods in P = [1 - (1 4-1) "](1+1) in a year tamw () + ) PV = Present Value fromsong number of years | arbohog- tril mi EXAMPLES (regular payment of a simple Annuity) 1. Mary borrowsP500, 000 to buy a car. She has two options to repay her loan. The interest is compounded monthly ev s mi zbong notelovning to isdman-A Option 1. 24 monthly payments every beginning of the month at 12% per year to rodmun isfor -it Option 2. 60 monthly payments every end of the month at 15% per yearas to isdmun ai 1 , Al Find: a. Mary's monthly payment under option each option b. The interest Mary pays under each option TIUMMA a191210 WUJAVAMUTUN :23.19MAX3 (asthuans novig silt Tabiarod Solution: babauogmos ."El is sweet & not dinom dons to gninnigsd sri is bonzogob 090.19 .A vijunnA a.For option 1: gros off in annow & not ismeup doss to gainniged ath is bolizoqeb 09089 : vianna Given : PV = P500,000, i= 0.01, n-24 xqmos bas (dunns ross to moms ends stelools.) MOITU.102 P=: (PV) (i) 500000(0.01) [1-(1+1)-m](1+i) [1-(1+0.01)-24](1+0.01) HI= P23,303.70 A vline For Option 2: i . DE = (SDEEM 28 3 0001 9 :movie Given: PV= 500,000, i=0.0125, n=60 P= - (PV)(0_ )(500,090) (0.0125) [1-(1+1)-n] - P11, 894. 97 [1-(1+0.0125)-60] 1 82(10.0 + 1)10901 (10.0 +1)- 10.0muityIiieltagfsbloerfhsenswolvifng annuity, nding the amount of annuity is usually asked. This amount of um 0 all payments of the annuity at the end of the last interest conversion period. Different examples on computin ' ' . ' ' g compound interest, future value of an ordinary annuity, present value of an ordinary annuity, future value of annuity due, present value of annuity due will make help you undemtand the process and follow the steps in solving the problem. {EVISED KNOWLEDGE: Actual answer to the process questions/ focus questions 1. Solve problems on compound interest? In solving problems on compound interest use the formula A = P(1 + r)r 2. How to differentiate annuity from annuity due? Annuity is a series of equal payments or withdrawals in the same period of time while annuity due is an mmuity where payments are done at the beginning of an interval for a specied period of time. 3. What is amortization schedule? How to create amortization schedule? Is a complete table of periodic loan payments, showing the amount of principal and the amount of interest that comprise each payment until the loan is paid off at the end of its term. To create amortization schedule you should know the monthly payment for the loan. Starting in month one , take the total amount of the loan and multiply it by the interest rate of the loan. Then for a loan with monthly repayments, divide the result by 12 to get you monthly interest. This should be done in an excel. The amortization schedule can be prepared as follows Ding lest stan tatort J. Calculate the periodic payment, Complete Column B with this periodic payment. 2. To fill up Column C, calculate interest using the formula: i - Pri. 1 -50 09010.10)(),12 500 forrow. ba Ipod Ve. me8; 1 19 to amongng On - 42 649.13(0.10),)#12 134.46:morrow3 05.805 216 bing momi InfoT 1 34 930.72(0.10)(2) +1 746.54 for row 3 ofgampumaThrowat all 161 000.9-[ to nsol n benisido sis Isupe " nsol ers to 26 8263906.10)2 momynq siborroq ads NOITU.102 1= 9 381:81 (0-10) 2)-1469.09 for row 6 PV * PJE 3. To fill up Column D. subtract Colunin Cifrom Column B. Column D: 9 850.87 -2 500.00 - P7,350.87 for row 1 000 02 =Vy Column D: 9 850.87 - 2 132.46 = P7 718.41 for row 2 Regular Payment of an Column D: 9 850.87 - 1 746.54 - 18 104.33 for row 3 Column D: 9 850.87 - 1 341.31 = P8 509.56 for row 4 Column D: 9 850.87 - 915.84 = P.8 935.03 for row 5 Column D: 9 850.87 - 469.09 = 19 381.81 for row 6 120 To all up Column E. subtract Column D from Column E as follows: - = 9 Semple Cra Column E: 50 000.00 - 7 350.87 = P-42 649.13 (Row 0) (Row 2) (20.01(060.02) Column E: 42 649.13 - 7 718.41 = 934 930.72 T8.028 09 = (Row 1) (Row 2) " (20 0+1)-5 Column E: 34 930.72 - 8 104.33 = 126 826.39 (Row 2) (Row 3) Column E: 26 826.39 - 8 509.56 = P18 316.84 (Row 3) (Row 4) MOITANITHON Column E: 18 316.84 - 8 935.03 = P9 381.81 laupo 10 mlugs pungu(Row 4),g.(Row 5) Borisq s Tovo nsol s to nottornzs isubang odT Column E: 9 381.81 - 9 381.81 = P0.00 Regular Payment twomilsient to sibonse leaps vd bostomes at tardi 00002 to nicol offi mardi que to swr alqmasks moronq off nil Note. nonolame Bias ova bus davisin loupy is $8.028,24 to amonin 1. The amount of the original loan is equal to the total repayments on the principal 2. The outstanding principal is equal to 0 at the end of the term fanoo ords , bisqs vilsubing ai nsol s noriw i douth wod bus lastomni ard of 2bog insming dons to soum word ase did Itw vor! I sebaol orli ban 9ba Types of Loan Isqioning gnioubs1 off of boilq 1. Consumer loan A loan given to customers for persona, family, or consumable items such as car, and home. slobod92 noussihom ofd'T PV bioqor InuomA | Nor Is lanzalal biboho 9 ort is legioning | icdianing erif of 2. Business Loan have to ban viove to bins EXAM arlinom a " Is a debt that the company is required to repay according to the loan's term and conditions. TR.028 04 Although computation for consumer loans and business loans are similar, they are different in some aspects like collateral, guarantor, documentation, terms, and follow-up consumer 1. Collateral real estate, equipment, furniture, fixtures, inventory, or personal real estate assets of the business owners { 20) 2. Guarantor the business owners have to sign the loan as guarantors does not require a guarantor 3. requires credit report, tax returns, Documentation and the last three years of requires a credit report or financial statements tax returns Terms shorter and includes a higher interest rate . longer than the business loan, Follow-up annual reviews of the relationship no further follow- up once are often conducted the loan is releasedThe amortization schedule can be prepared as follows Ding lest stan tatort J. Calculate the periodic payment, Complete Column B with this periodic payment. 2. To fill up Column C, calculate interest using the formula: i - Pri. 1 -50 09010.10)(),12 500 forrow. ba Ipod Ve. me8; 1 19 to amongng On - 42 649.13(0.10),)#12 134.46:morrow3 05.805 216 bing momi InfoT 1 34 930.72(0.10)(2) +1 746.54 for row 3 ofgampumaThrowat all 161 000.9-[ to nsol n benisido sis Isupe " nsol ers to 26 8263906.10)2 momynq siborroq ads NOITU.102 1= 9 381:81 (0-10) 2)-1469.09 for row 6 PV * PJE 3. To fill up Column D. subtract Colunin Cifrom Column B. Column D: 9 850.87 -2 500.00 - P7,350.87 for row 1 000 02 =Vy Column D: 9 850.87 - 2 132.46 = P7 718.41 for row 2 Regular Payment of an Column D: 9 850.87 - 1 746.54 - 18 104.33 for row 3 Column D: 9 850.87 - 1 341.31 = P8 509.56 for row 4 Column D: 9 850.87 - 915.84 = P.8 935.03 for row 5 Column D: 9 850.87 - 469.09 = 19 381.81 for row 6 120 To all up Column E. subtract Column D from Column E as follows: - = 9 Semple Cra Column E: 50 000.00 - 7 350.87 = P-42 649.13 (Row 0) (Row 2) (20.01(060.02) Column E: 42 649.13 - 7 718.41 = 934 930.72 T8.028 09 = (Row 1) (Row 2) " (20 0+1)-5 Column E: 34 930.72 - 8 104.33 = 126 826.39 (Row 2) (Row 3) Column E: 26 826.39 - 8 509.56 = P18 316.84 (Row 3) (Row 4) MOITANITHON Column E: 18 316.84 - 8 935.03 = P9 381.81 laupo 10 mlugs pungu(Row 4),g.(Row 5) Borisq s Tovo nsol s to nottornzs isubang odT Column E: 9 381.81 - 9 381.81 = P0.00 Regular Payment twomilsient to sibonse leaps vd bostomes at tardi 00002 to nicol offi mardi que to swr alqmasks moronq off nil Note. nonolame Bias ova bus davisin loupy is $8.028,24 to amonin 1. The amount of the original loan is equal to the total repayments on the principal 2. The outstanding principal is equal to 0 at the end of the term fanoo ords , bisqs vilsubing ai nsol s noriw i douth wod bus lastomni ard of 2bog insming dons to soum word ase did Itw vor! I sebaol orli ban 9ba Types of Loan Isqioning gnioubs1 off of boilq 1. Consumer loan A loan given to customers for persona, family, or consumable items such as car, and home. slobod92 noussihom ofd'T PV bioqor InuomA | Nor Is lanzalal biboho 9 ort is legioning | icdianing erif of 2. Business Loan have to ban viove to bins EXAM arlinom a " Is a debt that the company is required to repay according to the loan's term and conditions. TR.028 04 Although computation for consumer loans and business loans are similar, they are different in some aspects like collateral, guarantor, documentation, terms, and follow-up consumer 1. Collateral real estate, equipment, furniture, fixtures, inventory, or personal real estate assets of the business owners { 20) 2. Guarantor the business owners have to sign the loan as guarantors does not require a guarantor 3. requires credit report, tax returns, Documentation and the last three years of requires a credit report or financial statements tax returns Terms shorter and includes a higher interest rate . longer than the business loan, Follow-up annual reviews of the relationship no further follow- up once are often conducted the loan is releasedb. Interest Mary Pays under each option For Option 1 24 payments of P23,303.70: 24(23,303,70) = 559 288.80 Total interest paid: P559, 288,80- 500, 000 = P59, 288.80 For Option 2 60 payments of P1 1,894.97: 60( 1 1, 894.97) = 713, 698.20 Total interest paid: 713,698.20-500,000=P213, 698.20 2. Eva obtained a loan of P50,000 for the tuition fee of her son. She has to repay the loan by equal payments at the end of every six months for 3 years at 10% interest compounded semi-annually. Find the periodic payment. SOLUTION Given: PV= 50, 000 t= 3 years K=2 n=6 P = (PV) (i) [1-(1+1)-n P= (50,000) (0.05) (1-(1+0.05)-6] = P9, 850.87 AMORTIZATION The gradual extinction of a loan over a period of time by means of a sequence of regular or equal payments as to principal and interest due at the end of equal intervals of time In the previous example, we can say that the loan of 50000 that is amortized by equal periodic or installmer payments of P9,850.87 at equal intervals end every six months, becomes the present value of a simple annuity When a loan is gradually repaid, the construction of an amortization schedule is very important for both the lender and the lendee. They will both see how much of each payment goes to the interest and how much is applied to the reducing principal. nsol Yomueno bus , iso en roue amish oidsmuanos 10 . limit snomoq 101 asmoleus of noviy nnoi A The amortization Schedule smond Periodic Interest at 10% Amount repaid Outstanding Period Payment at the due at the end to the Principal Principal at the end of every of every at the end of end of every mol monieull 6 months 6 months every 6 months 6 months (A) 1791 2 (B) (C) (D) (E 0 P50 000.00 1 P9 850.87 P2 500.00 P7 350.87 P42 649.13 sail a paras 20iod (1 1 101 p9 850.87 lip-2 132.460 P7 718.41780 P34930.72 nollatugmoo dawson 3 P9 850.87 P1 746.54qu 18 104.33my 1P 26 826.39 4 P9 850.87 P1341.31 18 509.56 P18 316.84 P9 850.87 12915.84 P8 935.03 P9 381.81 6 P9 850.87 P 469.09 19 381.81 P0.00 Total 159 105.22 P9 105.24 P:50 000.00ANSWER. it represents simple annuity since the payment interval at the end of every three months is equal to the compounding interval 2. Determine whether the given situation describes ordinary annuity or an annuity due, justify your answer a. Jun's monthly mortgage payment is Php 35. 148.05 at the end of each month. Ack ANSWER: Ordinary annuity, since the payments are made at the end of each month.an DLE = h . The rent of the apartment is P7000 and due at the beginning of each month. ANSWER Annuity due, since the payments come at the beginning of each month Definition Future Value of an annuity -is the total accumulation of the payments and interest earned Present Value of an annuity -is the principal that must be invested today to provide the regular payment of an annuity Simple ordinary Annuity Formula Future Value of Simple Ordinary Annuity Present Value of Simple Ordinary Annuityon.08 4 FV P((+9) ), where py- 201-(140 where FV-the future value PV- present Value or Amount P- periodic payment P- Periodic Payment i = interest rate per period, where i- Interest rate per period, where i = -r = annual rate, K mini mlugm and marr-annual rate. K-number of conversion ! Ingul number of conversion periods in a year periods in a year n= total number of conversion periods n- number of conversion periods n K o t. t number of years noumub ali ILLUSTRATIVE EXAMPLES al borg gubnvonmna 1. If you pay P50.00 at the end of each month for 40 years on account that pays interest at 10% compounded monthly, how much money do you have after 40 years? quint Ytiming Inome SOLUTION: Given: P-P50.00, 1 in = 40(12) = 480 0 life an chunis Avital Inomean make FV = P50.00 316,203.98bung aint dunto a enunna na -on ellynA To Ins ard in ton gninniged out in sbach lon al mnaming albung of) - CiunnA barralad stab total amon ind ,faviaint inputvag does 2. Alex and Tony are twins. After graduation and being finally able to get a good job, they plan for retirement as follows. Starting at age 24, Alex deposits P10,000 at the end of each year for 36 years. Starting at age 42, Tony deposits P20,000 at the end of each year for 18 years. anal Who will have the greater amount of retirement if both annuities earn 1206 per year compounded annually? Solution For Alex's Plan For Tony's Plan P P10, 000.00 P- 20, 000.00 SHIWILLA 12% 12% 1 36(1) = 36 n IS(1) - 18 FV P10.000 (140.12)., mommy 0.12 FV =: 20.000 (1 + 0.12) - 1 0.12 FV 4.844.631.16 FV = 1,114,999.30CONTENT DISCUS Compound Interest When the interest due at the end of a certain period is added to the principal and the sum earns interest for the next period, the interest paid is called compounded interest The formula for compounded interest is A = P(1+)'3 Where, A = the final amount, accumulated value, or compound amount P= principal amount, present value i= the rate of interest for each conversion period. It is computed using i = r = nominal rate of interest or the annual interest rate Kine Poona 83 214tom= frequency of conversion periods in one year. ILLUSTRATIVE EXAMPLES aylar 1. Find the compound amount of the deposit at the end of 1 year if 20,000 is deposited at 4% compounded a. Annually b. Semi-annually Solution Given: P=20, 000 r=4% 1= 1 a. Annually Using the formula A=P( 1+r)' A=20,000(1+0.04) A= 20, 000( 1.04) A= 20, 800 b. A rate of 4% per year compounded semi-annually means a rate of 2% per half- year, we use the formula," Join A = P(1 + -)2 we have, bigot . dover zu1 0 A = 20, 000(1+ 0.04 2(1) A= Php 20,808.00 . In the same way, if interest is compounded quarterly, the rate per period is - and there are 4n periods in n years. A = P(1 + 7) . In general, the pattern can be extended for compounding K times per year, we have, A = P(1 + -)kt, where - is called periodic rate 2. Identify the interest rate per compounding period and the number of compounding periods for each of the following investments a. 12% compounded monthly for 4 years b. 10.2%compounded quarterly for 9 quarters Solutions a. 12% compounded monthly for 4 years r=12% K= 12(months per year) ! = 0.12 - = = 0.01 K 12 the number of compounding periods is 12t =1204 = 48 b. 10.2%compounded quarterly for 9 quarters r=10.2% = 0.102, K=4(quarters per year), = = 0.102 4 = 0.026. The number of compounding periods is 9If Php320, 000 is invested for 5 years at 8% compounded quarterly, find INMATE farpea. The compound amounts sil to invrain instriving ons sonia vliname alumnie amgeorggirl b. The compound interests prangand dogwhorange of se levisin guibrogmop ohioterra Towar Solutions, aif oub himnine is mo vintus manilao zodigest nouautie moving or isdistw orimmoral at a. r= 8%, K = 4 dmom doss to bas sir is 20 841 , Et gid ai toomeon ageghom vidinon e'sula XA = 320, 000(1 + 0 A = 320, 000 (1.02)20909 to bris art is sbem sis atomsq sill sonia , (inns (monibid. A = Php 475, 503.17 Compound amounts no town by yeaking go inly pornmid of b. Compound interest = Compound amounts - Principal amount Compound interest- 475, 503.17 -320, 060's mos inshivaq andi sonfe oub viunnA = Php 155, 503.17 4. What amount must be invested in order to have Php 128, 376.52 after8 years if money is worth 6% compounded semi-annually? SOLUTION Domino 1251Sim bus ammorning or to nouslumoos falo or 21- viunna as to ouisV sain't na Given: 160 *=2 qol (-gyears A-Php128, 376.52 25 mi- (siunan na to sulsV inoas A = P(1 + !)KL itunes P = - ( 1 + 5 ) ke manipulate the formula by dividing both sides by starving . months star "divan A vinnibno gigmiz P = 128,376.52 (1+0.03)2(8) P = 80, 000.00 / Yisnib10 olqmid to gulBY 192971 viiunnA yannib O olqmic to outaV squint " (+1)-19 InuomA 10 ouisV In92919 -Vq sulsy swift ord =Va Simple Annuity mom /81 0ibono9 -9 momysq oibonoq =q Definition of Terms grow bonoq isq 9in 12stani = i Annuity - a fixed sum of money paid to someone at regular intervals, subject to a fixed compound interest rate. Annuity Certain - payable for a definite duration: Begins and ends on a definite or fixed date (monthly payment of car loan). Annuity Uncertain - annuity payable for an indefinite duration (example: insurance); dependent on some certain event. Simple Annuity - interest conversion or compounding period is equal or the same as the Ull 50f is lesion payment interval, annoy Of Tol inom dogs to bas ath is 90.024 vaq wow !! General Annuity - interest conversion or compounding period is unequal or not the same as the payment interval. NOITU102 Ordinary Annuity (A,) - annuity in which the periodic payment is made at the end of each payment interval. Annuity Due - an annuity in which the periodic payment is made at the beginning of each payment interval. Deferred Annuity - the periodic payment is not made at the beginning nor at the end of each payment interval, but some later date. General Ordinary Annuity - first payment is made at the end of every payment interval. General Annuity Due - first payment is made at the beginning of every payment interval. Perpetuities - a series of periodic payments which are to run infinitely or forever. bobrogmos iBoy 19qafI mes esthummus died it inemomust lo moms isting and oved flay orW EXAMPLES 1. Determine if the given situations represent simple annuity or general annuity a. Payment are made at the end of each month for a loan that charges 1.05% interest compounded quarterly. nal'1 2 (NOT 10-1 ANSWER: 00.000 05 -4 00.000 019 -q General annuity, since the payment interval at the end of the month is not equal to the compounding interval quarterly b. A deposit of Php 5500.00 was made at the end of every three months to an account that earns 5.6% interest compounded quarterly oo,0S = Va 21000,01 7 473Directions: Complete the table by solving using compound interest. If the maturity value is rolled out at 6% every 120 days for 2 years at the end of the period, it will accumulate an interest of: Example 1 120 l ,000. 00 PIOZ, 010 00 360 360 360 P1 .050 0] 360 g). {403,285.67 360 5 Pl,093.69 360 3'32 P112,682.Sl 360 ACTIVITY 2 Directions: Fill in the blanks. Complete the following statements. l. is an interest that is generated in terms of years that is based only on the starting amount or principal amount. 2. Mr. De Jesus made an investment for 5 years with an interest rate of 6% compounded monthly. The compounding frequency of the investment is 3. a series of payment or withdrawals at the same period of time. 4. a payment done at the end of an interval on a specic period of time 5. is the other term for future value in simple and compounding interes B. PERFORMANCE TASK Your parents are planning to save for their retirement A retirement plan is a nancial arrangement made by an individual employees/employers, insurance companies, and other institutions to replace employment income upon retirement. 'I'hey target to accumulate P5000, 000 m 10 years. To do this, they want to set aside a portion of their salaries and contribute monthly for their retirement funds. How much 'should they contribute per month if they have a chance to invest in an annuity that earns 5% compounded quarterly

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance