JUST NEED HELP SOLVING PART G

-------------------------------------------------------------

EXAMPLE FOR SOLVING PART G --->

-------------------------------------------------

| Company_Return | Market_Return | Treasury_Bill_Return |

| -0.035449 | -0.082619 | 0.005859 |

| -0.002394 | 0.025812 | 0.005859 |

| 0.179976 | 0.012094 | 0.006289 |

| -0.010419 | -0.023591 | 0.006893 |

| 0.058229 | 0.101888 | 0.006479 |

| 0.088803 | -0.010313 | 0.005899 |

| -0.066188 | 0.005712 | 0.006754 |

| -0.109261 | -0.102419 | 0.006177 |

| -0.232636 | -0.043126 | 0.005945 |

| 0.079823 | -0.010859 | 0.006594 |

| 0.195324 | 0.071901 | 0.005632 |

| 0.189786 | 0.045237 | 0.005915 |

| 0.281247 | 0.059515 | 0.004663 |

| 0.028227 | 0.088262 | 0.004741 |

| 0.191063 | 0.026432 | 0.004384 |

| -0.179045 | 0.006896 | 0.005434 |

| -0.154051 | 0.037771 | 0.004378 |

| -0.125742 | -0.049829 | 0.004097 |

| 0.097771 | 0.040955 | 0.004742 |

| 0.164071 | 0.045298 | 0.004689 |

| -0.048706 | -0.002081 | 0.004656 |

| 0.022356 | 0.005901 | 0.004299 |

| -0.015073 | -0.036002 | 0.003817 |

| 0.121696 | 0.114502 | 0.003803 |

| 0.147575 | -0.002113 | 0.003046 |

| 0.047748 | 0.032573 | 0.002861 |

| -0.137981 | -0.033753 | 0.003376 |

| 0.017323 | -0.006558 | 0.003353 |

| -0.010381 | 0.007744 | 0.002717 |

| -0.194235 | -0.035327 | 0.003164 |

| -0.028961 | 0.057279 | 0.002953 |

| -0.003705 | -0.037037 | 0.002583 |

| -0.033759 | 0.020023 | 0.002476 |

| 0.176663 | 0.002729 | 0.002336 |

| 0.096854 | 0.024573 | 0.002322 |

| 0.058481 | 0.020305 | 0.002301 |

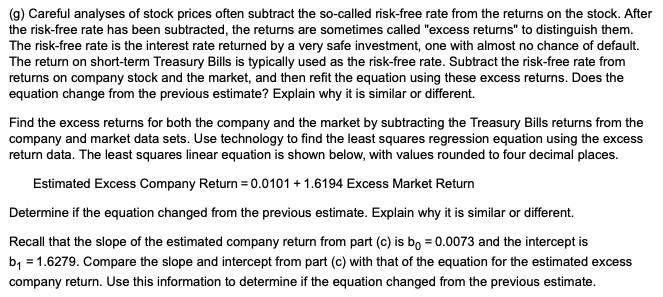

The accompanying data set tracks the monthly performance of stock in a large computer company. The data include 36 monthly returns on the company, as well as returns on the entire stock market and returns on short-term Treasury Bills. Complete parts (a) through (9) below. : Click the icon to view the data table. (c) Estimate the least squares linear equation for Company Return on Market Return. Interpret the intercept and slope. Be sure to include their units. Note if either estimate represents a large extrapolation and is consequently not reliable. Complete the equation for the fitted line below. Estimated Company Return = 0.0093 + 1.3805 Market Return (Round to four decimal places as needed.) (g) Careful analyses of stock prices often subtract the so-called risk-free rate from the returns on the stock. After the risk-free rate has been subtracted, the returns are sometimes called "excess returns" to distinguish them. The risk-free rate is the interest rate returned by a very safe investment, one with almost no chance of default. The return on short-term Treasury Bills is typically used as the risk-free rate. Subtract the risk-free rate from returns on company stock and the market, and then refit the equation using these excess returns. Does the equation change from the previous estimate? Explain why it is similar or different. Complete the equation for the refitted line below. Excess Market Return Estimated Excess Company Return = + (Round to four decimal places as needed.) (g) Careful analyses of stock prices often subtract the so-called risk-free rate from the returns on the stock. After the risk-free rate has been subtracted, the returns are sometimes called "excess returns" to distinguish them. The risk-free rate is the interest rate returned by a very safe investment, one with almost no chance of default. The return on short-term Treasury Bills is typically used as the risk-free rate. Subtract the risk-free rate from returns on company stock and the market, and then refit the equation using these excess returns. Does the equation change from the previous estimate? Explain why it is similar or different. Find the excess returns for both the company and the market by subtracting the Treasury Bills returns from the company and market data sets. Use technology to find the least squares regression equation using the excess return data. The least squares linear equation is shown below, with values rounded to four decimal places. Estimated Excess Company Return = 0.0101 + 1.6194 Excess Market Return Determine if the equation changed from the previous estimate. Explain why it is similar or different. Recall that the slope of the estimated company return from part (c) is bo = 0.0073 and the intercept is by = 1.6279. Compare the slope and intercept from part (c) with that of the equation for the estimated excess company return. Use this information to determine if the equation changed from the previous estimate. The accompanying data set tracks the monthly performance of stock in a large computer company. The data include 36 monthly returns on the company, as well as returns on the entire stock market and returns on short-term Treasury Bills. Complete parts (a) through (9) below. : Click the icon to view the data table. (c) Estimate the least squares linear equation for Company Return on Market Return. Interpret the intercept and slope. Be sure to include their units. Note if either estimate represents a large extrapolation and is consequently not reliable. Complete the equation for the fitted line below. Estimated Company Return = 0.0093 + 1.3805 Market Return (Round to four decimal places as needed.) (g) Careful analyses of stock prices often subtract the so-called risk-free rate from the returns on the stock. After the risk-free rate has been subtracted, the returns are sometimes called "excess returns" to distinguish them. The risk-free rate is the interest rate returned by a very safe investment, one with almost no chance of default. The return on short-term Treasury Bills is typically used as the risk-free rate. Subtract the risk-free rate from returns on company stock and the market, and then refit the equation using these excess returns. Does the equation change from the previous estimate? Explain why it is similar or different. Complete the equation for the refitted line below. Excess Market Return Estimated Excess Company Return = + (Round to four decimal places as needed.) (g) Careful analyses of stock prices often subtract the so-called risk-free rate from the returns on the stock. After the risk-free rate has been subtracted, the returns are sometimes called "excess returns" to distinguish them. The risk-free rate is the interest rate returned by a very safe investment, one with almost no chance of default. The return on short-term Treasury Bills is typically used as the risk-free rate. Subtract the risk-free rate from returns on company stock and the market, and then refit the equation using these excess returns. Does the equation change from the previous estimate? Explain why it is similar or different. Find the excess returns for both the company and the market by subtracting the Treasury Bills returns from the company and market data sets. Use technology to find the least squares regression equation using the excess return data. The least squares linear equation is shown below, with values rounded to four decimal places. Estimated Excess Company Return = 0.0101 + 1.6194 Excess Market Return Determine if the equation changed from the previous estimate. Explain why it is similar or different. Recall that the slope of the estimated company return from part (c) is bo = 0.0073 and the intercept is by = 1.6279. Compare the slope and intercept from part (c) with that of the equation for the estimated excess company return. Use this information to determine if the equation changed from the previous estimate