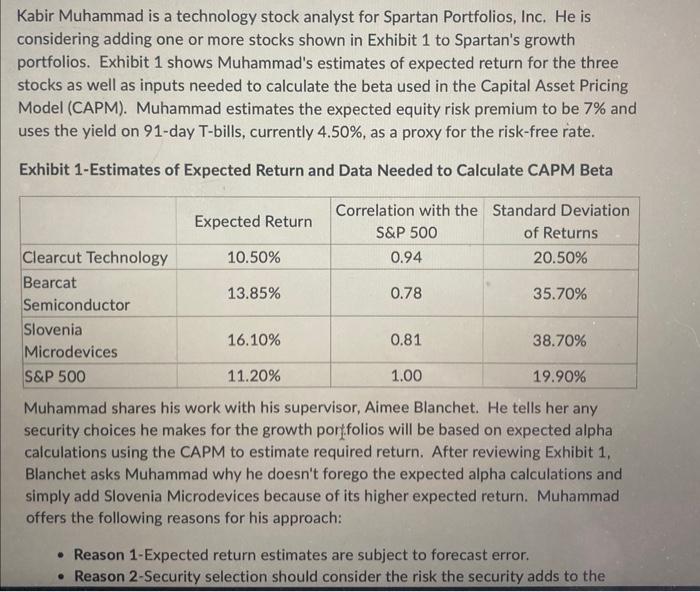

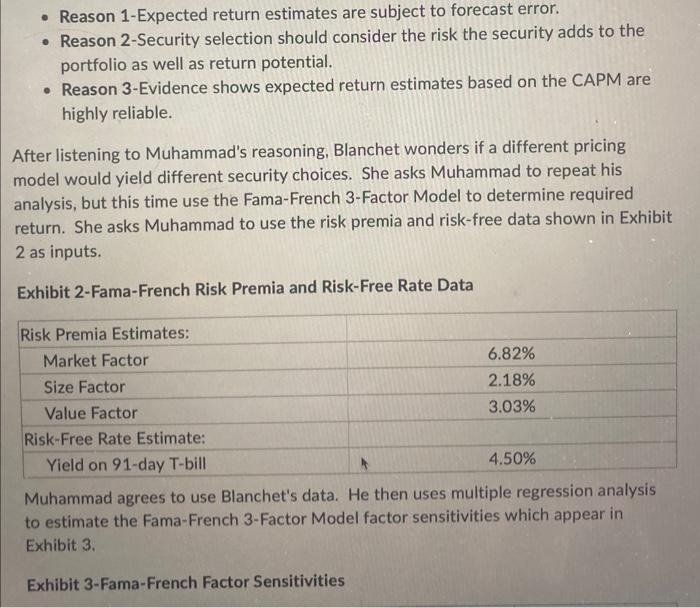

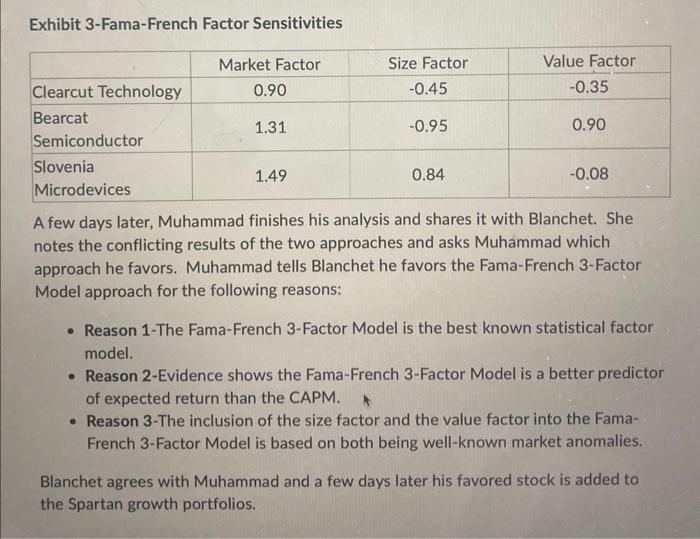

Kabir Muhammad is a technology stock analyst for Spartan Portfolios, Inc. He is considering adding one or more stocks shown in Exhibit 1 to Spartan's growth portfolios. Exhibit 1 shows Muhammad's estimates of expected return for the three stocks as well as inputs needed to calculate the beta used in the Capital Asset Pricing Model (CAPM). Muhammad estimates the expected equity risk premium to be 7% and uses the yield on 91-day T-bills, currently 4.50%, as a proxy for the risk-free rate. Exhibit 1-Estimates of Expected Return and Data Needed to Calculate CAPM Beta Muhammad shares his work with his supervisor, Aimee Blanchet. He tells her any security choices he makes for the growth por folios will be based on expected alpha calculations using the CAPM to estimate required return. After reviewing Exhibit 1 , Blanchet asks Muhammad why he doesn't forego the expected alpha calculations and simply add Slovenia Microdevices because of its higher expected return. Muhammad offers the following reasons for his approach: - Reason 1-Expected return estimates are subject to forecast error. - Reason 2-Security selection should consider the risk the security adds to the - Reason 1-Expected return estimates are subject to forecast error. - Reason 2-Security selection should consider the risk the security adds to the portfolio as well as return potential. - Reason 3-Evidence shows expected return estimates based on the CAPM are highly reliable. After listening to Muhammad's reasoning, Blanchet wonders if a different pricing model would yield different security choices. She asks Muhammad to repeat his analysis, but this time use the Fama-French 3-Factor Model to determine required return. She asks Muhammad to use the risk premia and risk-free data shown in Exhibit 2 as inputs. Exhibit 2-Fama-French Risk Premia and Risk-Free Rate Data Muhammad agrees to use Blanchet's data. He then uses multiple regression analysis to estimate the Fama-French 3-Factor Model factor sensitivities which appear in Exhibit 3. Exhibit 3-Fama-French Factor Sensitivities Exhibit 3-Fama-French Factor Sensitivities A few days later, Muhammad finishes his analysis and shares it with Blanchet. She notes the conflicting results of the two approaches and asks Muhammad which approach he favors. Muhammad tells Blanchet he favors the Fama-French 3-Factor Model approach for the following reasons: - Reason 1-The Fama-French 3-Factor Model is the best known statistical factor model. - Reason 2-Evidence shows the Fama-French 3-Factor Model is a better predictor of expected return than the CAPM. - Reason 3-The inclusion of the size factor and the value factor into the FamaFrench 3-Factor Model is based on both being well-known market anomalies. Blanchet agrees with Muhammad and a few days later his favored stock is added to the Spartan growth portfolios. Based on the data in Exhibit 1, Exhibit 2, and Exhibit 3, and using the Fama-French 3-Factor Model to determine required return, what is the expected alpha for Slovenia Microdevices? 0.15%0.47%0.88%