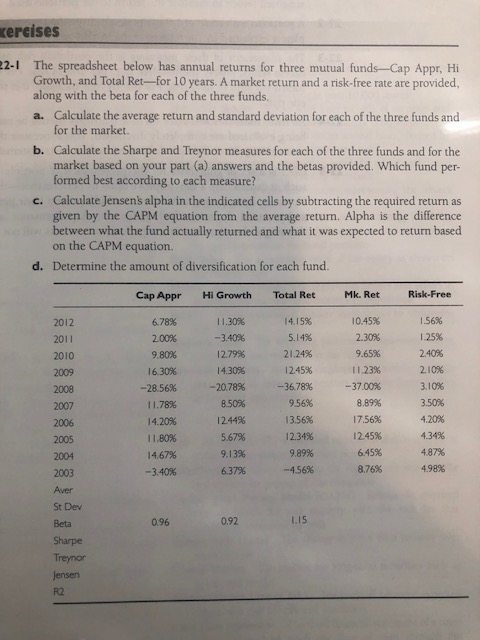

Kercises 22-1 The spreadsheet below has annual returns for three mutual funds-Cap Appr, Hi Growth, and Total Ret--for 10 years. A market return and a risk-free rate are provided, along with the beta for each of the three funds. a. Calculate the average return and standard deviation for each of the three funds and for the market. b. Calculate the Sharpe and Treynor measures for each of the three funds and for the market based on your part (a) answers and the betas provided. Which fund per- formed best according to each measure? c. Calculate Jensen's alpha in the indicated cells by subtracting the required return as given by the CAPM equation from the average return. Alpha is the difference between what the fund actually returned and what it was expected to return based on the CAPM equation. d. Determine the amount of diversification for each fund. Cap Appr Hi Growth Total Ret Mk. Ret Risk-Free 6.78% 2.00% 9.80% 16.30% -28.56% 11.78% 14.20% 11.80% 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 Aver St Dev Beta Sharpe Treynor Jensen 11.30% -3.40% 12.79% 14.30% -20.78% 8.50% 12.44% 5.67% 9.1396 6.37% 14.15% 5.14% 21.24% 12.45% -36.78% 9.56% 13.56% 12.34% 9.89% -456% 10.45% 2.30% 9.65% 11.23% -37.00% 8.89% 17.56% 12.45% 6.45% 8.76% 1.56% 1.25% 2.40% 2.10% 3.10% 3.50% 4.20% 4.34% 4.87% 4.98% 14.67% -3.40% 0.96 0.92 1.15 RO Kercises 22-1 The spreadsheet below has annual returns for three mutual funds-Cap Appr, Hi Growth, and Total Ret--for 10 years. A market return and a risk-free rate are provided, along with the beta for each of the three funds. a. Calculate the average return and standard deviation for each of the three funds and for the market. b. Calculate the Sharpe and Treynor measures for each of the three funds and for the market based on your part (a) answers and the betas provided. Which fund per- formed best according to each measure? c. Calculate Jensen's alpha in the indicated cells by subtracting the required return as given by the CAPM equation from the average return. Alpha is the difference between what the fund actually returned and what it was expected to return based on the CAPM equation. d. Determine the amount of diversification for each fund. Cap Appr Hi Growth Total Ret Mk. Ret Risk-Free 6.78% 2.00% 9.80% 16.30% -28.56% 11.78% 14.20% 11.80% 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 Aver St Dev Beta Sharpe Treynor Jensen 11.30% -3.40% 12.79% 14.30% -20.78% 8.50% 12.44% 5.67% 9.1396 6.37% 14.15% 5.14% 21.24% 12.45% -36.78% 9.56% 13.56% 12.34% 9.89% -456% 10.45% 2.30% 9.65% 11.23% -37.00% 8.89% 17.56% 12.45% 6.45% 8.76% 1.56% 1.25% 2.40% 2.10% 3.10% 3.50% 4.20% 4.34% 4.87% 4.98% 14.67% -3.40% 0.96 0.92 1.15 RO