Answered step by step

Verified Expert Solution

Question

1 Approved Answer

kindly assist Study the information provided below and answer the following questions: INFORMATION An institutional investor is considering three mutual funds. The first is a

kindly assist

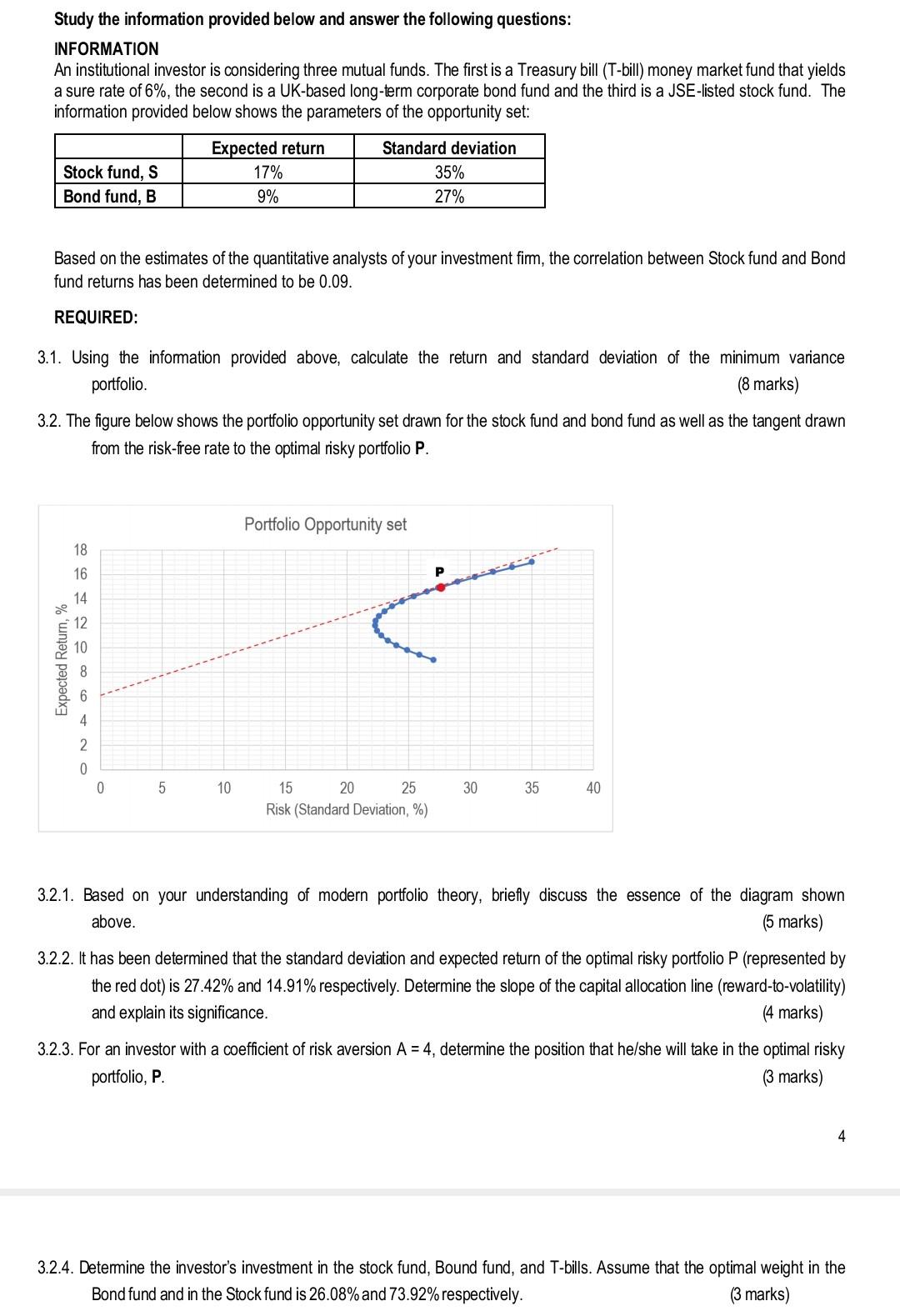

Study the information provided below and answer the following questions: INFORMATION An institutional investor is considering three mutual funds. The first is a Treasury bill (T-bill) money market fund that yields a sure rate of 6%, the second is a UK-based long-term corporate bond fund and the third is a JSE-listed stock fund. The information provided below shows the parameters of the opportunity set: Based on the estimates of the quantitative analysts of your investment fim, the correlation between Stock fund and Bond fund returns has been determined to be 0.09 . REQUIRED: 3.1. Using the information provided above, calculate the return and standard deviation of the minimum variance portfolio. (8 marks) 3.2. The figure below shows the portfolio opportunity set drawn for the stock fund and bond fund as well as the tangent drawn from the risk-free rate to the optimal risky portfolio P. 3.2.1. Based on your understanding of modern portfolio theory, briefly discuss the essence of the diagram shown above. ( 5 marks) 3.2.2. It has been determined that the standard deviation and expected return of the optimal risky portfolio P (represented by the red dot) is 27.42% and 14.91% respectively. Determine the slope of the capital allocation line (reward-to-volatility) and explain its significance. (4 marks) 3.2.3. For an investor with a coefficient of risk aversion A=4, determine the position that he/she will take in the optimal risky portfolio, P. (3 marks) 4 3.2.4. Determine the investor's investment in the stock fund, Bound fund, and T-bills. Assume that the optimal weight in the Bond fund and in the Stock fund is 26.08% and 73.92% respectivelyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Cornerstones Of Managerial Accounting

Authors: Dan L. Heitger, Maryanne M. Mowen, Don R. Hansen

1st Edition