Answered step by step

Verified Expert Solution

Question

1 Approved Answer

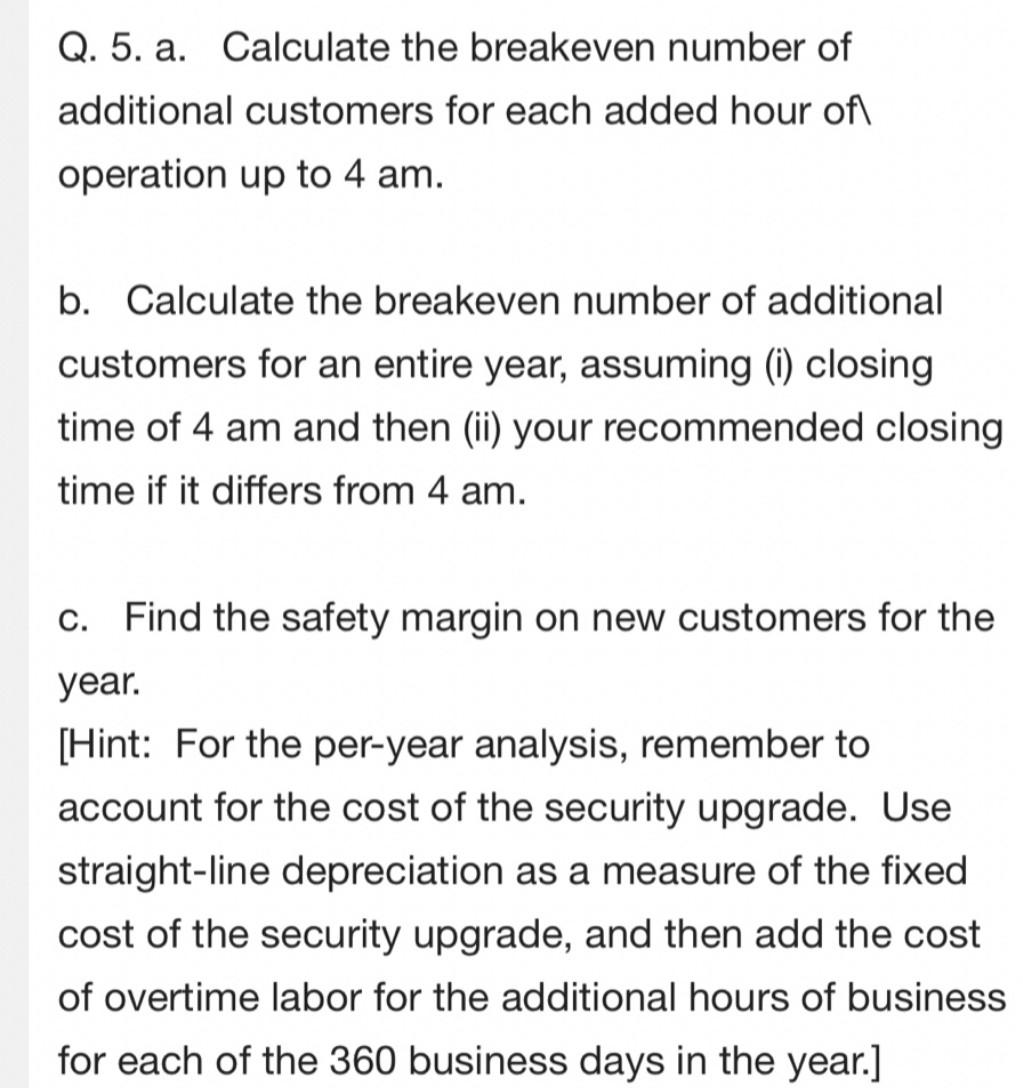

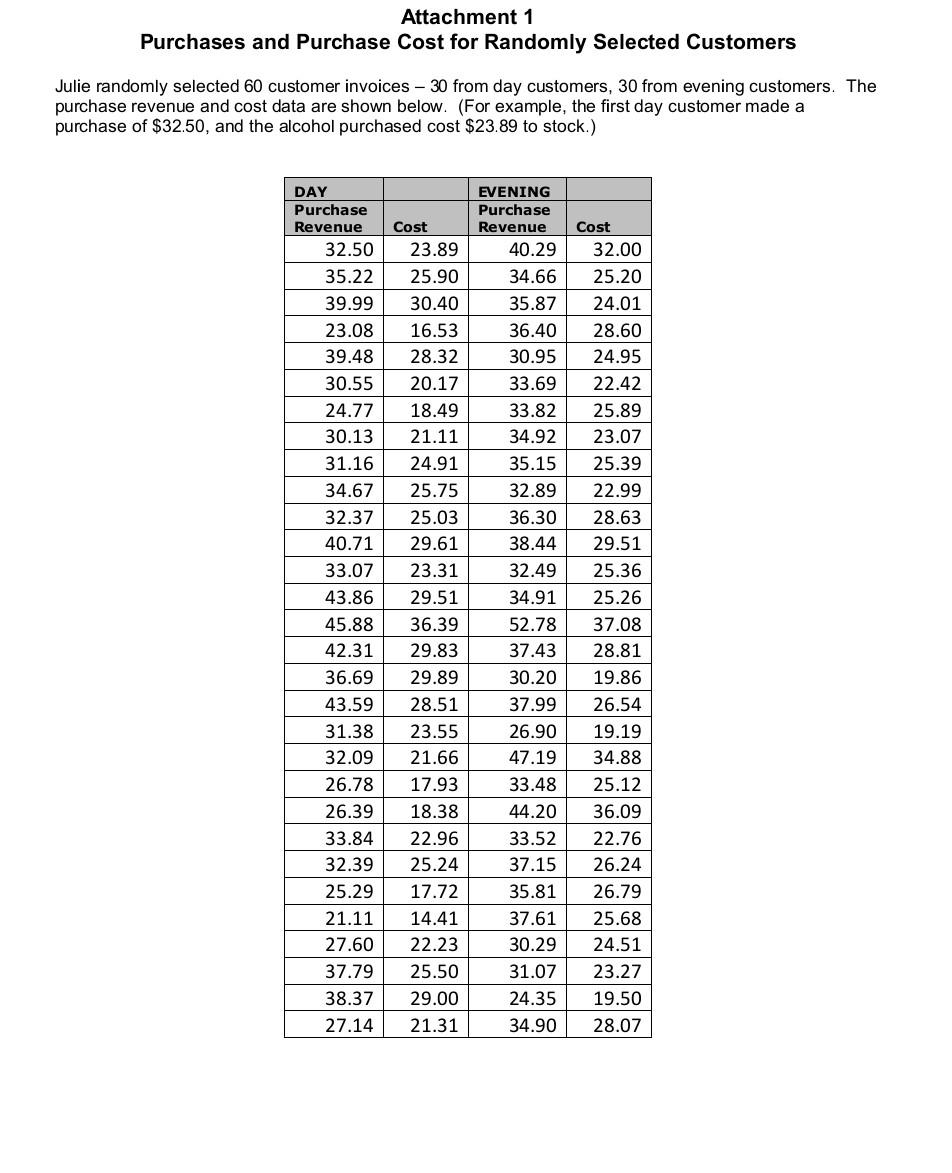

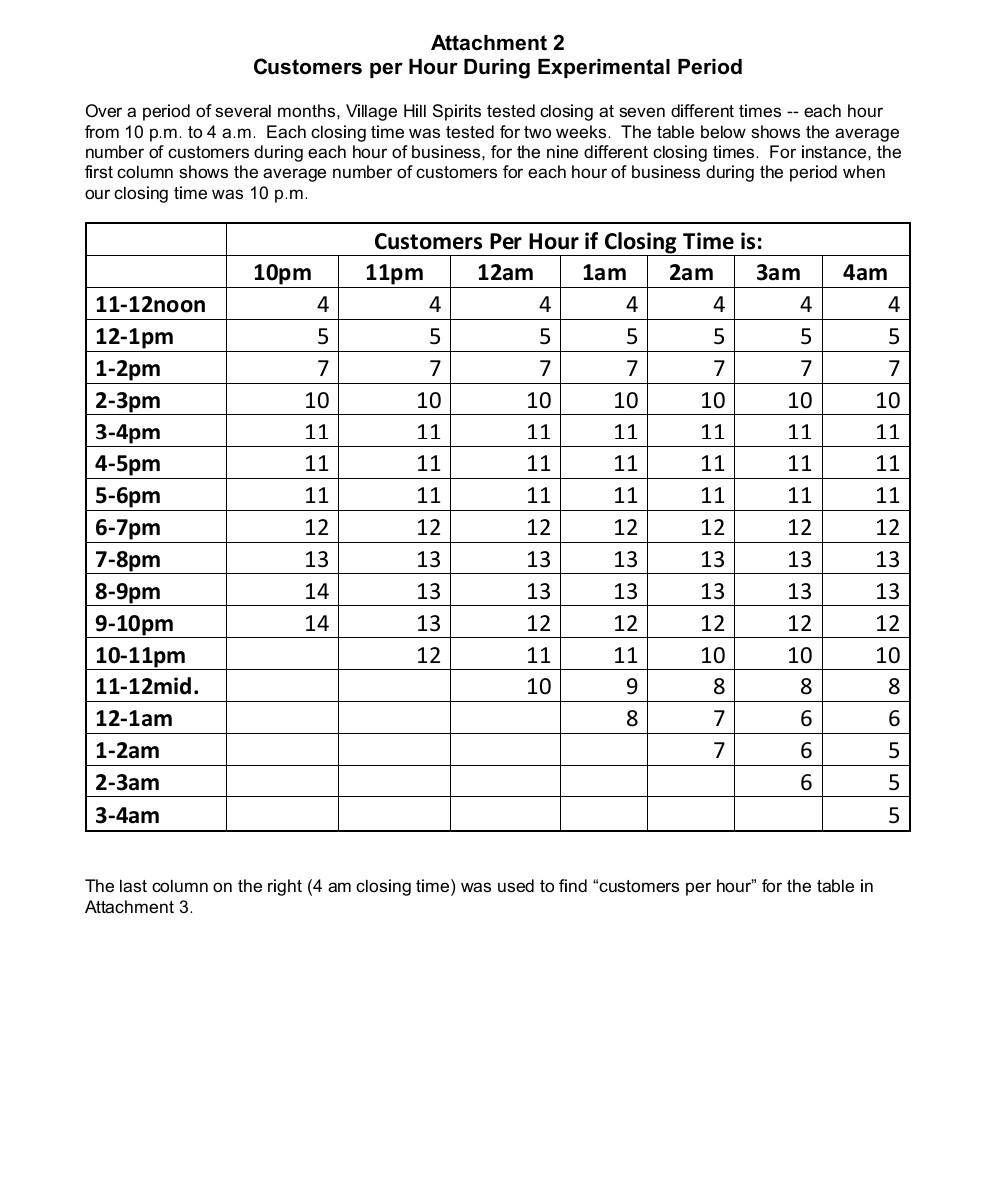

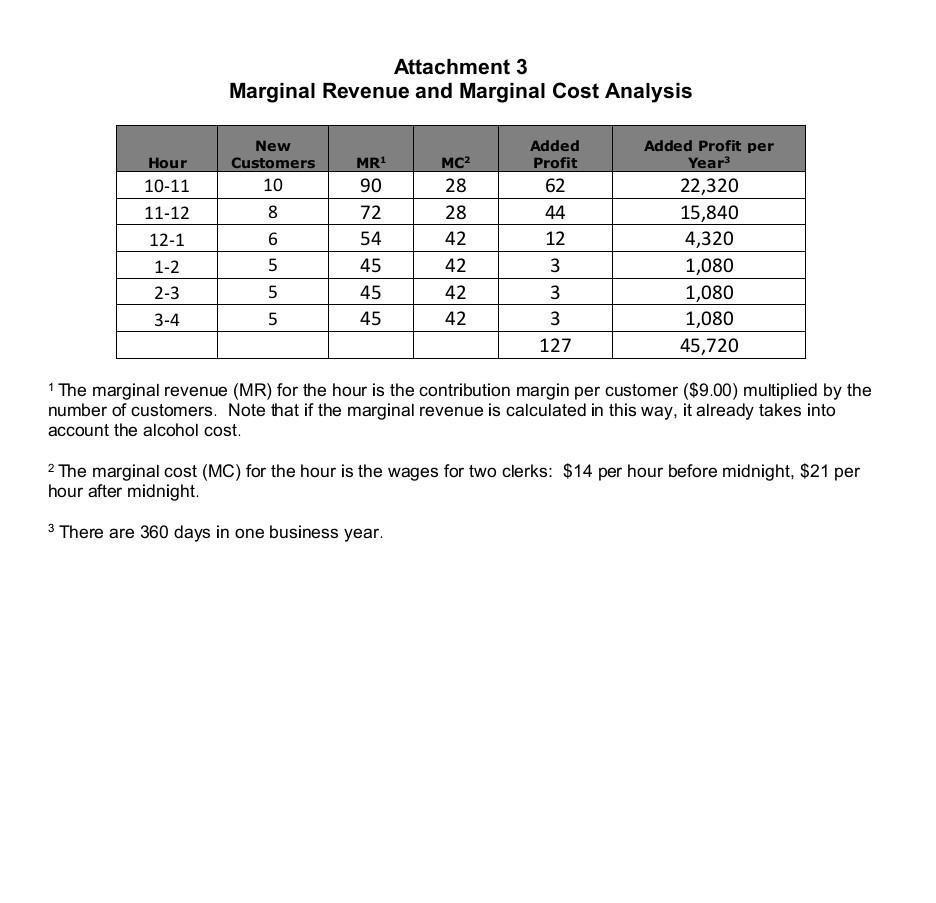

kindly assist with the above question ASAP Q. 5. a. Calculate the breakeven number of additional customers for each added hour of operation up to

kindly assist with the above question ASAP

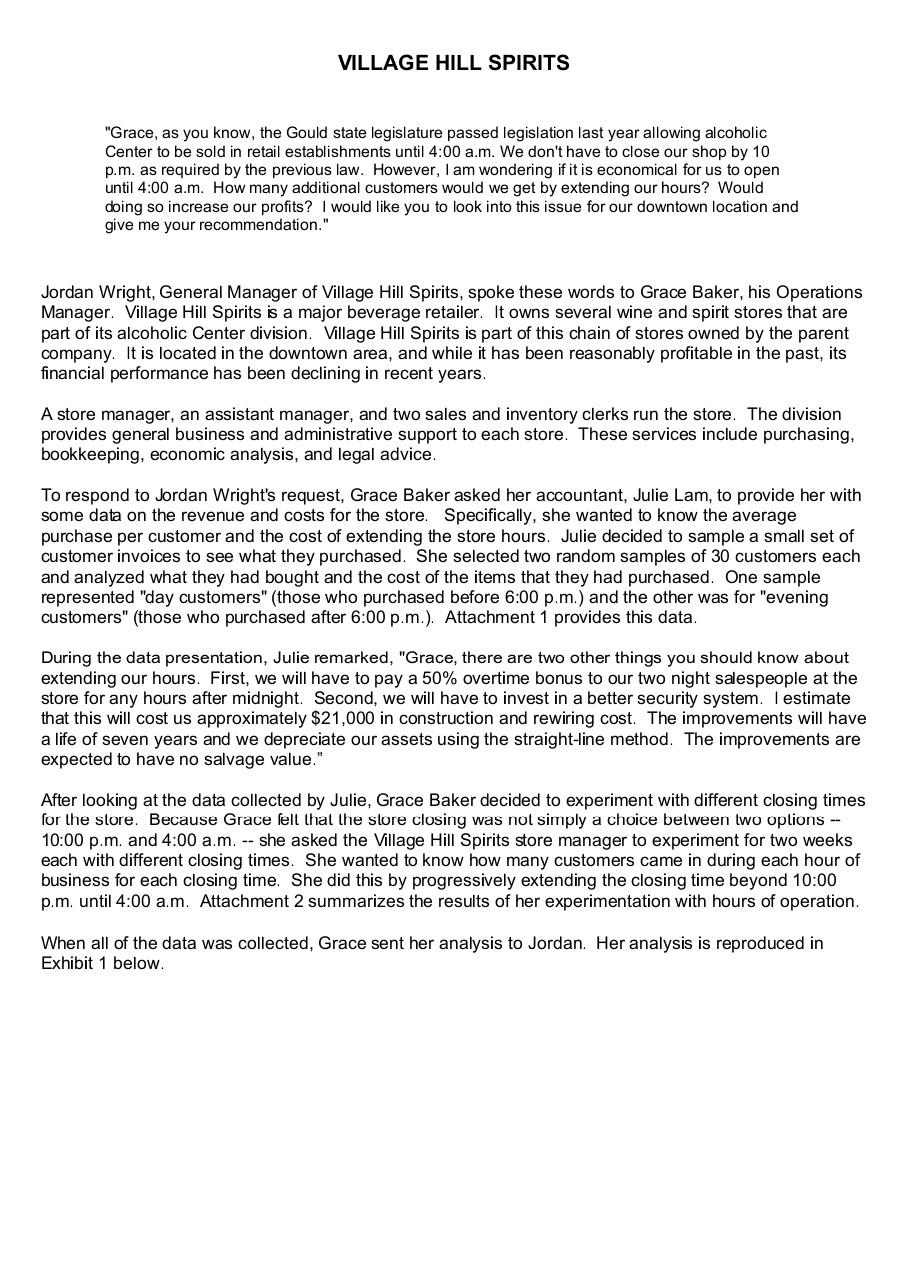

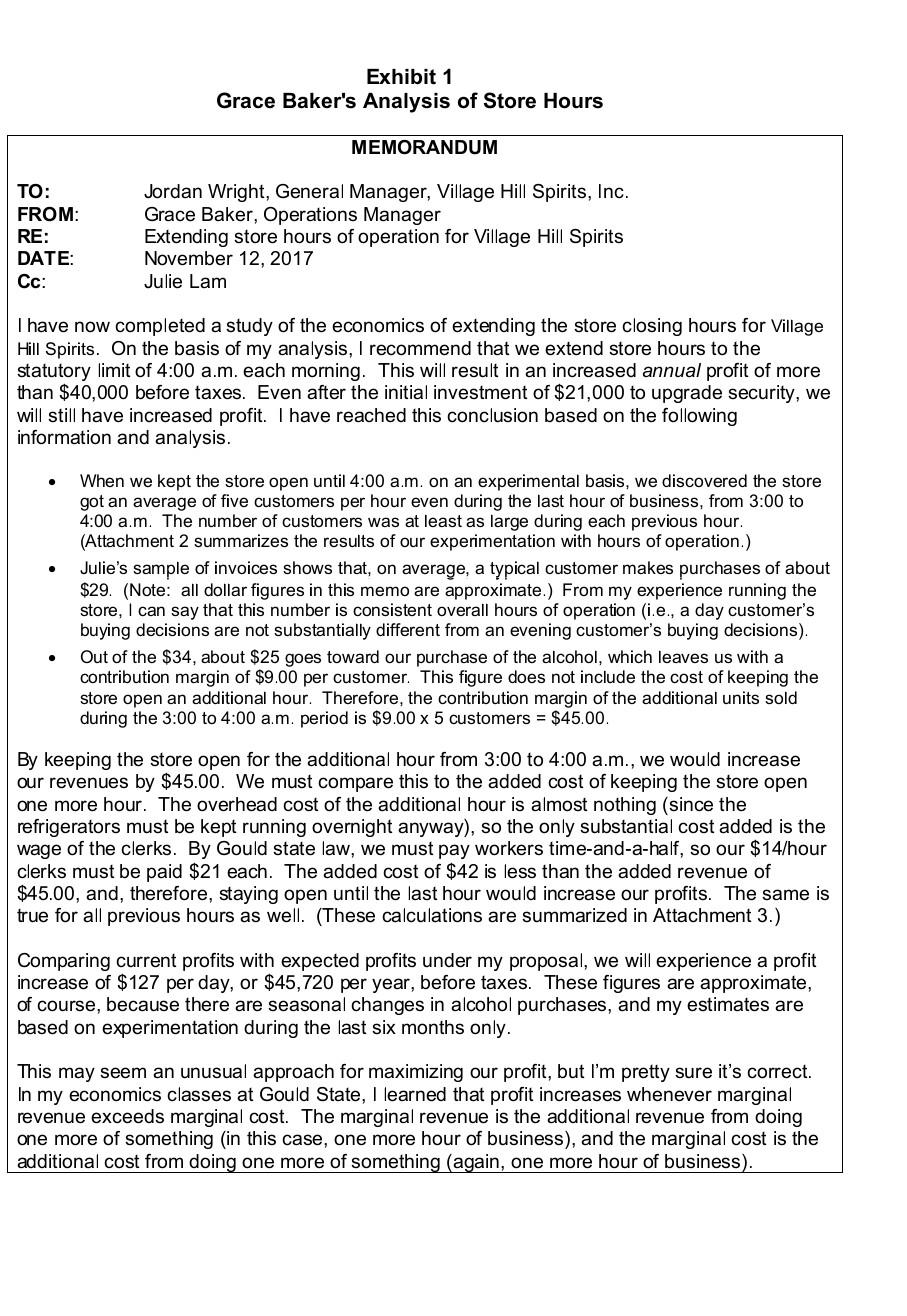

Q. 5. a. Calculate the breakeven number of additional customers for each added hour of\ operation up to 4 am. b. Calculate the breakeven number of additional customers for an entire year, assuming (i) closing time of 4 am and then (ii) your recommended closing time if it differs from 4 am. c. Find the safety margin on new customers for the year. [Hint: For the per-year analysis, remember to account for the cost of the security upgrade. Use straight-line depreciation as a measure of the fixed cost of the security upgrade, and then add the cost of overtime labor for the additional hours of business for each of the 360 business days in the year.] VILLAGE HILL SPIRITS "Grace, as you know, the Gould state legislature passed legislation last year allowing alcoholic Center to be sold in retail establishments until 4:00 a.m. We don't have to close our shop by 10 p.m. as required by the previous law. However, I am wondering if it is economical for us to open until 4:00 a.m. How many additional customers would we get by extending our hours? Would doing so increase our profits? I would like you to look into this issue for our downtown location and give me your recommendation." Jordan Wright, General Manager of Village Hill Spirits, spoke these words to Grace Baker, his Operations Manager. Village Hill Spirits is a major beverage retailer. It owns several wine and spirit stores that are part of its alcoholic Center division. Village Hill Spirits is part of this chain of stores owned by the parent company. It is located in the downtown area, and while it has been reasonably profitable in the past, its financial performance has been declining in recent years. A store manager, an assistant manager, and two sales and inventory clerks run the store. The division provides general business and administrative support to each store. These services include purchasing, bookkeeping, economic analysis, and legal advice. To respond to Jordan Wright's request, Grace Baker asked her accountant, Julie Lam, to provide her with some data on the revenue and costs for the store. Specifically, she wanted to know the average purchase per customer and the cost of extending the store hours. Julie decided to sample a small set of customer invoices to see what they purchased. She selected two random samples of 30 customers each and analyzed what they had bought and the cost of the items that they had purchased. One sample represented "day customers" (those who purchased before 6:00 p.m.) and the other was for "evening customers" (those who purchased after 6:00 p.m.). Attachment 1 provides this data. During the data presentation, Julie remarked, "Grace, there are two other things you should know about extending our hours. First, we will have to pay a 50% overtime bonus to our two night salespeople at the store for any hours after midnight. Second, we will have to invest in a better security system. I estimate that this will cost us approximately $21,000 in construction and rewiring cost. The improvements will have a life of seven years and we depreciate our assets using the straight-line method. The improvements are expected to have no salvage value." After looking at the data collected by Julie, Grace Baker decided to experiment with different closing times for the store. Because Grace felt that the store closing was not simply a choice belween two options -- 10:00 p.m. and 4:00 a.m. -- she asked the Village Hill Spirits store manager to experiment for two weeks each with different closing times. She wanted to know how many customers came in during each hour of business for each closing time. She did this by progressively extending the closing time beyond 10:00 p.m. until 4:00 a.m. Attachment 2 summarizes the results of her experimentation with hours of operation. When all of the data was collected, Grace sent her analysis to Jordan. Her analysis is reproduced in Exhibit 1 below. Exhibit 1 Grace Baker's Analysis of Store Hours MEMORANDUM TO: FROM: RE: DATE: Cc: Jordan Wright, General Manager, Village Hill Spirits, Inc. Grace Baker, Operations Manager Extending store hours of operation for Village Hill Spirits November 12, 2017 Julie Lam I have now completed a study of the economics of extending the store closing hours for Village Hill Spirits. On the basis of my analysis, I recommend that we extend store hours to the statutory limit of 4:00 a.m. each morning. This will result in an increased annual profit of more than $40,000 before taxes. Even after the initial investment of $21,000 to upgrade security, we will still have increased profit. I have reached this conclusion based on the following information and analysis. . . When we kept the store open until 4:00 a.m. on an experimental basis, we discovered the store got an average of five customers per hour even during the last hour of business, from 3:00 to 4:00 a.m. The number of customers was at least as large during each previous hour. (Attachment 2 summarizes the results of our experimentation with hours of operation.) Julie's sample of invoices shows that, on average, a typical customer makes purchases of about $29. (Note: all dollar figures in this memo are approximate.) From my experience running the store, I can say that this number is consistent overall hours of operation (i.e., a day customer's buying decisions are not substantially different from an evening customer's buying decisions). Out of the $34, about $25 goes toward our purchase of the alcohol, which leaves us with a contribution margin of $9.00 per customer. This figure does not include the cost of keeping the store open an additional hour. Therefore, the contribution margin of the additional units sold during the 3:00 to 4:00 a.m. period is $9.00 x 5 customers = $45.00. By keeping the store open for the additional hour from 3:00 to 4:00 a.m., we would increase our revenues by $45.00. We must compare this to the added cost of keeping the store open one more hour. The overhead cost of the additional hour is almost nothing (since the refrigerators must be kept running overnight anyway), so the only substantial cost added is the wage of the clerks. By Gould state law, we must pay workers time-and-a-half, so our $14/hour clerks must be paid $21 each. The added cost of $42 is less than the added revenue of $45.00, and, therefore, staying open until the last hour would increase our profits. The same is true for all previous hours as well. (These calculations are summarized in Attachment 3.) Comparing current profits with expected profits under my proposal, we will experience a profit increase of $127 per day, or $45,720 per year, before taxes. These figures are approximate, of course, because there are seasonal changes in alcohol purchases, and my estimates are based on experimentation during the last six months only. This may seem an unusual approach for maximizing our profit, but I'm pretty sure it's correct. In my economics classes at Gould State, I learned that profit increases whenever marginal revenue exceeds marginal cost. The marginal revenue is the additional revenue from doing one more of something in this case, one more hour of business), and the marginal cost is the additional cost from doing one more of something (again, one more hour of business). Later that week Grace and Jordan met to discuss Grace's analysis. "Grace", began Jordan, "I appreciate the work that you and Julie have put into this analysis. Obviously, you two have collected a lot of data and thought this through carefully. However, I am unclear about a few things and I would appreciate it if you could clarify them for me. First, I don't get this 'marginal approach.' I took economics in college, and I am embarrassed to admit that I heaved a sigh of relief and promptly forgot everything once the course was over. I am confused about how there can be two marginal costs in this situation, one for liquor and the other for the sales clerks. Second, Julie's sample suggests that evening customers seem to purchase a higher amount. Why then did you use the average purchase overall hours of operation? Third, I wonder if some customers who arrive during the very late hours might arrive earlier if the store closed earlier. Can you tell from your experimental data if that's true? And would that change your recommendation?" Required: Assume that you are Grace Baker and you have been asked to elaborate on the memo in Exhibit 1 to address the issues raised by Jordan Wright in both of his conversations with you. Use the report form from the course website. This case reviews the following LDC concepts: Financial accounting and 9; management accounting 2 and 8; microeconomics 6 and 7, and statistics 2 and 4 Attachment 1 Purchases and Purchase Cost for Randomly Selected Customers Julie randomly selected 60 customer invoices - 30 from day customers, 30 from evening customers. The purchase revenue and cost data are shown below. (For example, the first day customer made a purchase of $32.50, and the alcohol purchased cost $23.89 to stock.) DAY Purchase Revenue 32.50 35.22 39.99 23.08 39.48 30.55 24.77 30.13 31.16 34.67 32.37 40.71 33.07 43.86 45.88 42.31 36.69 43.59 31.38 32.09 26.78 26.39 33.84 32.39 25.29 21.11 27.60 37.79 38.37 27.14 Cost 23.89 25.90 30.40 16.53 28.32 20.17 18.49 21.11 24.91 25.75 25.03 29.61 23.31 29.51 36.39 29.83 29.89 28.51 23.55 21.66 17.93 18.38 22.96 25.24 17.72 14.41 22.23 25.50 29.00 21.31 EVENING Purchase Revenue 40.29 34.66 35.87 36.40 30.95 33.69 33.82 34.92 35.15 32.89 36.30 38.44 32.49 34.91 52.78 37.43 30.20 37.99 26.90 47.19 33.48 44.20 33.52 37.15 35.81 37.61 30.29 31.07 24.35 34.90 Cost 32.00 25.20 24.01 28.60 24.95 22.42 25.89 23.07 25.39 22.99 28.63 29.51 25.36 25.26 37.08 28.81 19.86 26.54 19.19 34.88 25.12 36.09 22.76 26.24 26.79 25.68 24.51 23.27 19.50 28.07 Attachment 2 Customers per Hour During Experimental Period Over a period of several months, Village Hill Spirits tested closing at seven different times -- each hour from 10 p.m. to 4 a.m. Each closing time was tested for two weeks. The table below shows the average number of customers during each hour of business, for the nine different closing times. For instance, the first column shows the average number of customers for each hour of business during the period when our closing time was 10 p.m. 10pm 4am 4 ulu 5 7 10 | | 7 10 9 |4|5|111 911 Customers Per Hour if Closing Time is: 11pm 12am 1am 2am 3am 4 4 4 4 4 5 5 5 5 7 7 7 7 7 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 13 13 13 13 13 13 13 13 13 12 12 12 12 11 11 10 10 10 9 11 11 11 1-1H- --- 11 11-12noon 12-1pm 1-2pm 2-3pm 3-4pm 4-5pm 5-6pm 6-7pm 7-8pm 8-9pm 9-10pm 10-11pm 11-12mid. 12-1am 1-2am 2-3am 3-4am 12 12 13 14 14 |5| 19877 13 13 13132. 12 10 1998-6.6.6 198655) 8 5 The last column on the right (4 am closing time) was used to find "customers per hour" for the table in Attachment 3 Attachment 3 Marginal Revenue and Marginal Cost Analysis Hour 10-11 11-12 12-1 New Customers 10 8 Added Profit 62 44 MR 90 72 54 45 45 45 MC2 28 28 42 42 42 6 12 Added Profit per Year3 22,320 15,840 4,320 1,080 1,080 1,080 45,720 5 1-2 2-3 5 3 3 3 127 3-4 5 42 1 The marginal revenue (MR) for the hour is the contribution margin per customer ($9.00) multiplied by the number of customers. Note that if the marginal revenue is calculated in this way, it already takes into account the alcohol cost. 2 The marginal cost (MC) for the hour is the wages for two clerks: $14 per hour before midnight, $21 per hour after midnight 3 There are 360 days in one business year. Q. 5. a. Calculate the breakeven number of additional customers for each added hour of\ operation up to 4 am. b. Calculate the breakeven number of additional customers for an entire year, assuming (i) closing time of 4 am and then (ii) your recommended closing time if it differs from 4 am. c. Find the safety margin on new customers for the year. [Hint: For the per-year analysis, remember to account for the cost of the security upgrade. Use straight-line depreciation as a measure of the fixed cost of the security upgrade, and then add the cost of overtime labor for the additional hours of business for each of the 360 business days in the year.] VILLAGE HILL SPIRITS "Grace, as you know, the Gould state legislature passed legislation last year allowing alcoholic Center to be sold in retail establishments until 4:00 a.m. We don't have to close our shop by 10 p.m. as required by the previous law. However, I am wondering if it is economical for us to open until 4:00 a.m. How many additional customers would we get by extending our hours? Would doing so increase our profits? I would like you to look into this issue for our downtown location and give me your recommendation." Jordan Wright, General Manager of Village Hill Spirits, spoke these words to Grace Baker, his Operations Manager. Village Hill Spirits is a major beverage retailer. It owns several wine and spirit stores that are part of its alcoholic Center division. Village Hill Spirits is part of this chain of stores owned by the parent company. It is located in the downtown area, and while it has been reasonably profitable in the past, its financial performance has been declining in recent years. A store manager, an assistant manager, and two sales and inventory clerks run the store. The division provides general business and administrative support to each store. These services include purchasing, bookkeeping, economic analysis, and legal advice. To respond to Jordan Wright's request, Grace Baker asked her accountant, Julie Lam, to provide her with some data on the revenue and costs for the store. Specifically, she wanted to know the average purchase per customer and the cost of extending the store hours. Julie decided to sample a small set of customer invoices to see what they purchased. She selected two random samples of 30 customers each and analyzed what they had bought and the cost of the items that they had purchased. One sample represented "day customers" (those who purchased before 6:00 p.m.) and the other was for "evening customers" (those who purchased after 6:00 p.m.). Attachment 1 provides this data. During the data presentation, Julie remarked, "Grace, there are two other things you should know about extending our hours. First, we will have to pay a 50% overtime bonus to our two night salespeople at the store for any hours after midnight. Second, we will have to invest in a better security system. I estimate that this will cost us approximately $21,000 in construction and rewiring cost. The improvements will have a life of seven years and we depreciate our assets using the straight-line method. The improvements are expected to have no salvage value." After looking at the data collected by Julie, Grace Baker decided to experiment with different closing times for the store. Because Grace felt that the store closing was not simply a choice belween two options -- 10:00 p.m. and 4:00 a.m. -- she asked the Village Hill Spirits store manager to experiment for two weeks each with different closing times. She wanted to know how many customers came in during each hour of business for each closing time. She did this by progressively extending the closing time beyond 10:00 p.m. until 4:00 a.m. Attachment 2 summarizes the results of her experimentation with hours of operation. When all of the data was collected, Grace sent her analysis to Jordan. Her analysis is reproduced in Exhibit 1 below. Exhibit 1 Grace Baker's Analysis of Store Hours MEMORANDUM TO: FROM: RE: DATE: Cc: Jordan Wright, General Manager, Village Hill Spirits, Inc. Grace Baker, Operations Manager Extending store hours of operation for Village Hill Spirits November 12, 2017 Julie Lam I have now completed a study of the economics of extending the store closing hours for Village Hill Spirits. On the basis of my analysis, I recommend that we extend store hours to the statutory limit of 4:00 a.m. each morning. This will result in an increased annual profit of more than $40,000 before taxes. Even after the initial investment of $21,000 to upgrade security, we will still have increased profit. I have reached this conclusion based on the following information and analysis. . . When we kept the store open until 4:00 a.m. on an experimental basis, we discovered the store got an average of five customers per hour even during the last hour of business, from 3:00 to 4:00 a.m. The number of customers was at least as large during each previous hour. (Attachment 2 summarizes the results of our experimentation with hours of operation.) Julie's sample of invoices shows that, on average, a typical customer makes purchases of about $29. (Note: all dollar figures in this memo are approximate.) From my experience running the store, I can say that this number is consistent overall hours of operation (i.e., a day customer's buying decisions are not substantially different from an evening customer's buying decisions). Out of the $34, about $25 goes toward our purchase of the alcohol, which leaves us with a contribution margin of $9.00 per customer. This figure does not include the cost of keeping the store open an additional hour. Therefore, the contribution margin of the additional units sold during the 3:00 to 4:00 a.m. period is $9.00 x 5 customers = $45.00. By keeping the store open for the additional hour from 3:00 to 4:00 a.m., we would increase our revenues by $45.00. We must compare this to the added cost of keeping the store open one more hour. The overhead cost of the additional hour is almost nothing (since the refrigerators must be kept running overnight anyway), so the only substantial cost added is the wage of the clerks. By Gould state law, we must pay workers time-and-a-half, so our $14/hour clerks must be paid $21 each. The added cost of $42 is less than the added revenue of $45.00, and, therefore, staying open until the last hour would increase our profits. The same is true for all previous hours as well. (These calculations are summarized in Attachment 3.) Comparing current profits with expected profits under my proposal, we will experience a profit increase of $127 per day, or $45,720 per year, before taxes. These figures are approximate, of course, because there are seasonal changes in alcohol purchases, and my estimates are based on experimentation during the last six months only. This may seem an unusual approach for maximizing our profit, but I'm pretty sure it's correct. In my economics classes at Gould State, I learned that profit increases whenever marginal revenue exceeds marginal cost. The marginal revenue is the additional revenue from doing one more of something in this case, one more hour of business), and the marginal cost is the additional cost from doing one more of something (again, one more hour of business). Later that week Grace and Jordan met to discuss Grace's analysis. "Grace", began Jordan, "I appreciate the work that you and Julie have put into this analysis. Obviously, you two have collected a lot of data and thought this through carefully. However, I am unclear about a few things and I would appreciate it if you could clarify them for me. First, I don't get this 'marginal approach.' I took economics in college, and I am embarrassed to admit that I heaved a sigh of relief and promptly forgot everything once the course was over. I am confused about how there can be two marginal costs in this situation, one for liquor and the other for the sales clerks. Second, Julie's sample suggests that evening customers seem to purchase a higher amount. Why then did you use the average purchase overall hours of operation? Third, I wonder if some customers who arrive during the very late hours might arrive earlier if the store closed earlier. Can you tell from your experimental data if that's true? And would that change your recommendation?" Required: Assume that you are Grace Baker and you have been asked to elaborate on the memo in Exhibit 1 to address the issues raised by Jordan Wright in both of his conversations with you. Use the report form from the course website. This case reviews the following LDC concepts: Financial accounting and 9; management accounting 2 and 8; microeconomics 6 and 7, and statistics 2 and 4 Attachment 1 Purchases and Purchase Cost for Randomly Selected Customers Julie randomly selected 60 customer invoices - 30 from day customers, 30 from evening customers. The purchase revenue and cost data are shown below. (For example, the first day customer made a purchase of $32.50, and the alcohol purchased cost $23.89 to stock.) DAY Purchase Revenue 32.50 35.22 39.99 23.08 39.48 30.55 24.77 30.13 31.16 34.67 32.37 40.71 33.07 43.86 45.88 42.31 36.69 43.59 31.38 32.09 26.78 26.39 33.84 32.39 25.29 21.11 27.60 37.79 38.37 27.14 Cost 23.89 25.90 30.40 16.53 28.32 20.17 18.49 21.11 24.91 25.75 25.03 29.61 23.31 29.51 36.39 29.83 29.89 28.51 23.55 21.66 17.93 18.38 22.96 25.24 17.72 14.41 22.23 25.50 29.00 21.31 EVENING Purchase Revenue 40.29 34.66 35.87 36.40 30.95 33.69 33.82 34.92 35.15 32.89 36.30 38.44 32.49 34.91 52.78 37.43 30.20 37.99 26.90 47.19 33.48 44.20 33.52 37.15 35.81 37.61 30.29 31.07 24.35 34.90 Cost 32.00 25.20 24.01 28.60 24.95 22.42 25.89 23.07 25.39 22.99 28.63 29.51 25.36 25.26 37.08 28.81 19.86 26.54 19.19 34.88 25.12 36.09 22.76 26.24 26.79 25.68 24.51 23.27 19.50 28.07 Attachment 2 Customers per Hour During Experimental Period Over a period of several months, Village Hill Spirits tested closing at seven different times -- each hour from 10 p.m. to 4 a.m. Each closing time was tested for two weeks. The table below shows the average number of customers during each hour of business, for the nine different closing times. For instance, the first column shows the average number of customers for each hour of business during the period when our closing time was 10 p.m. 10pm 4am 4 ulu 5 7 10 | | 7 10 9 |4|5|111 911 Customers Per Hour if Closing Time is: 11pm 12am 1am 2am 3am 4 4 4 4 4 5 5 5 5 7 7 7 7 7 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 13 13 13 13 13 13 13 13 13 12 12 12 12 11 11 10 10 10 9 11 11 11 1-1H- --- 11 11-12noon 12-1pm 1-2pm 2-3pm 3-4pm 4-5pm 5-6pm 6-7pm 7-8pm 8-9pm 9-10pm 10-11pm 11-12mid. 12-1am 1-2am 2-3am 3-4am 12 12 13 14 14 |5| 19877 13 13 13132. 12 10 1998-6.6.6 198655) 8 5 The last column on the right (4 am closing time) was used to find "customers per hour" for the table in Attachment 3 Attachment 3 Marginal Revenue and Marginal Cost Analysis Hour 10-11 11-12 12-1 New Customers 10 8 Added Profit 62 44 MR 90 72 54 45 45 45 MC2 28 28 42 42 42 6 12 Added Profit per Year3 22,320 15,840 4,320 1,080 1,080 1,080 45,720 5 1-2 2-3 5 3 3 3 127 3-4 5 42 1 The marginal revenue (MR) for the hour is the contribution margin per customer ($9.00) multiplied by the number of customers. Note that if the marginal revenue is calculated in this way, it already takes into account the alcohol cost. 2 The marginal cost (MC) for the hour is the wages for two clerks: $14 per hour before midnight, $21 per hour after midnight 3 There are 360 days in one business yearStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public School Finance Decoded

Authors: Jay C. Toland

1st Edition

1475827679, 978-1475827675