Answered step by step

Verified Expert Solution

Question

1 Approved Answer

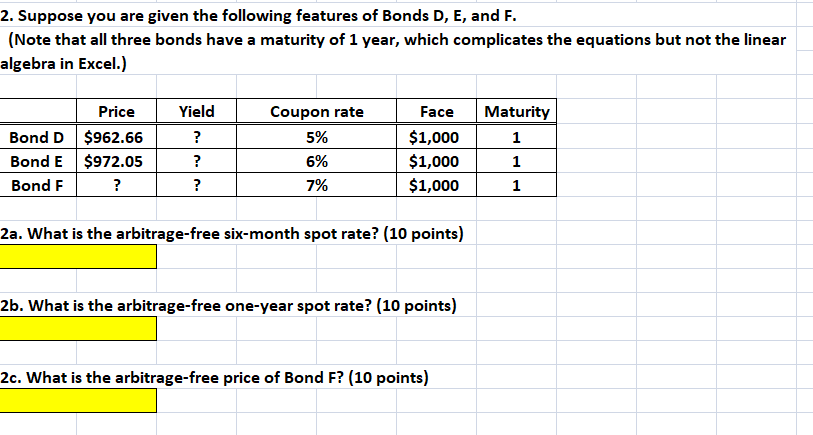

Kindly do it handwritten with explanation. 2. Suppose you are given the following features of Bonds D, E, and F. (Note that all three bonds

Kindly do it handwritten with explanation.

2. Suppose you are given the following features of Bonds D, E, and F. (Note that all three bonds have a maturity of 1 year, which complicates the equations but not the linear algebra in Excel.) 2a. What is the arbitrage-free six-month spot rate? (10 points) 2b. What is the arbitrage-free one-year spot rate? ( 10 points) 2c. What is the arbitrage-free price of Bond F? ( 10 points) 2. Suppose you are given the following features of Bonds D, E, and F. (Note that all three bonds have a maturity of 1 year, which complicates the equations but not the linear algebra in Excel.) 2a. What is the arbitrage-free six-month spot rate? (10 points) 2b. What is the arbitrage-free one-year spot rate? ( 10 points) 2c. What is the arbitrage-free price of Bond F? ( 10 points)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Financial Communication And Investor Relations

Authors: Alexander V. Laskin

1st Edition

1119240786, 978-1119240785