Kindly help me solve these

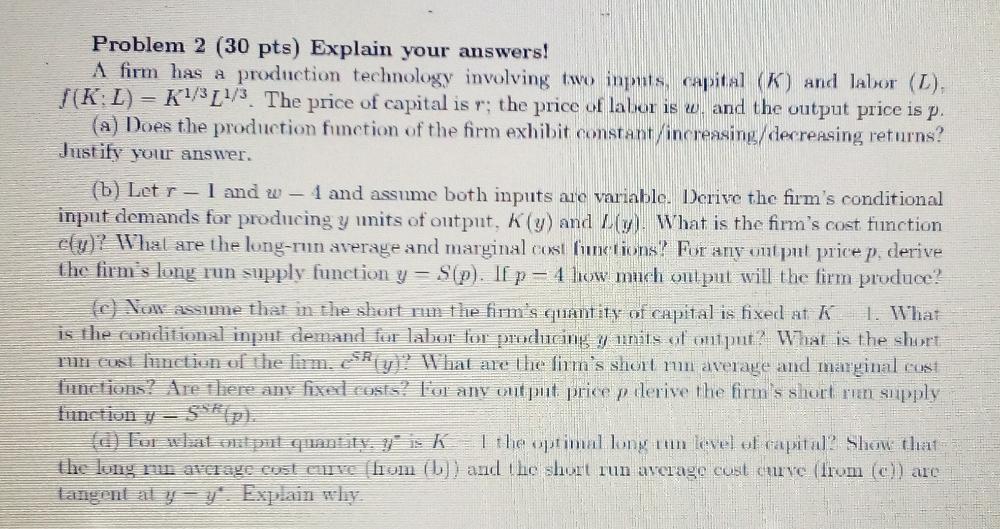

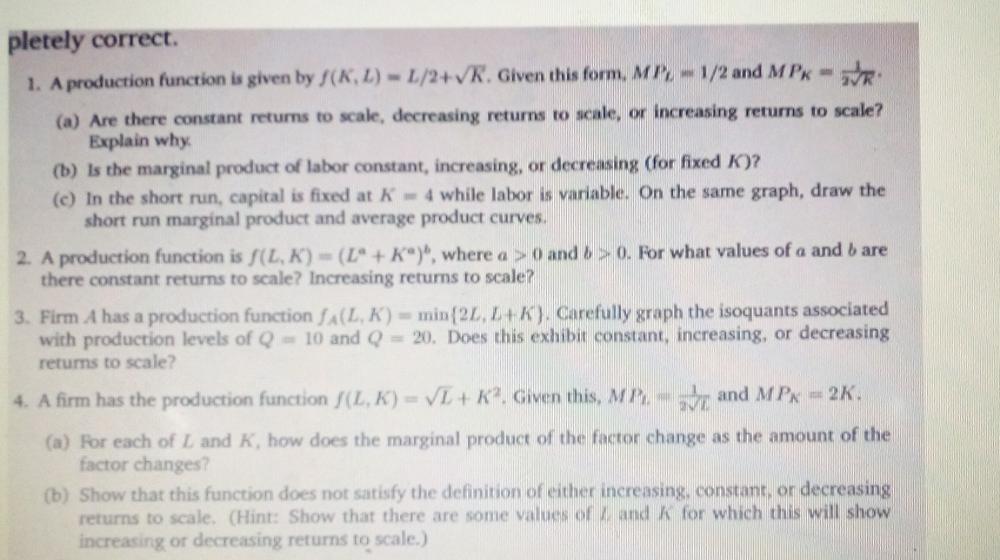

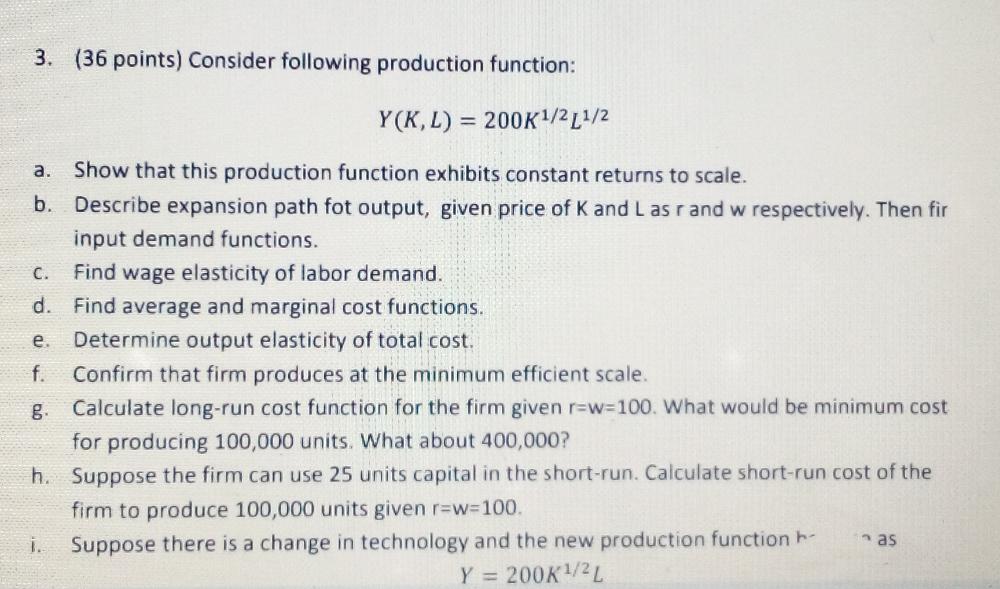

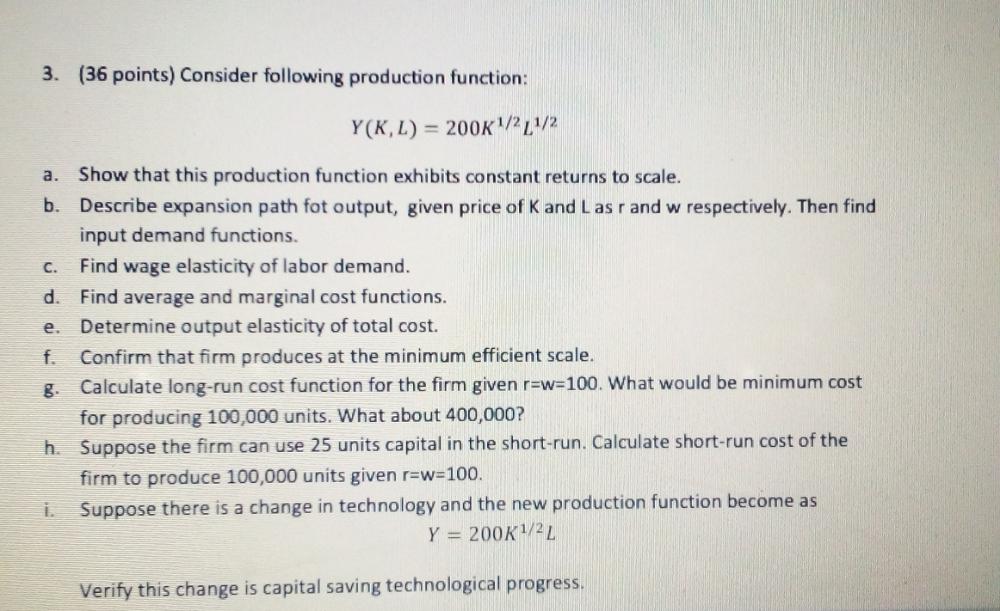

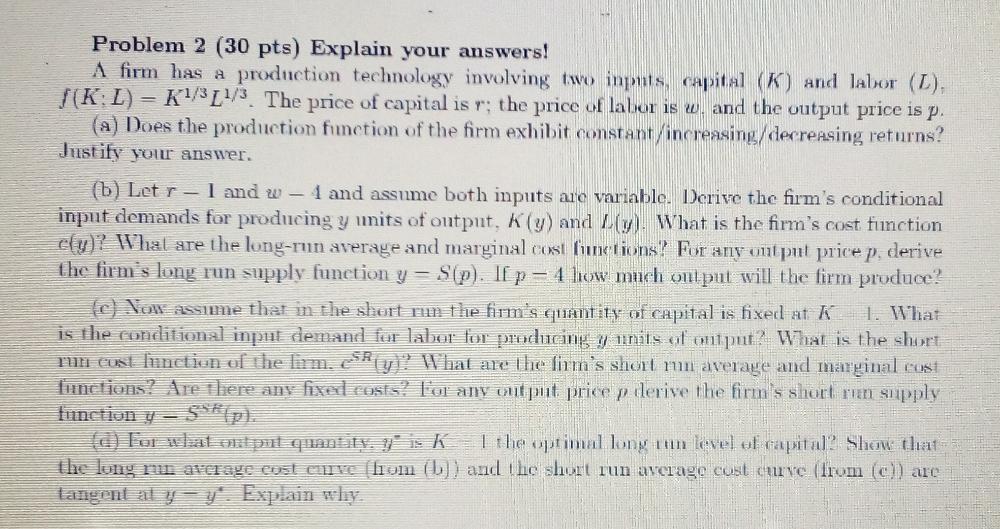

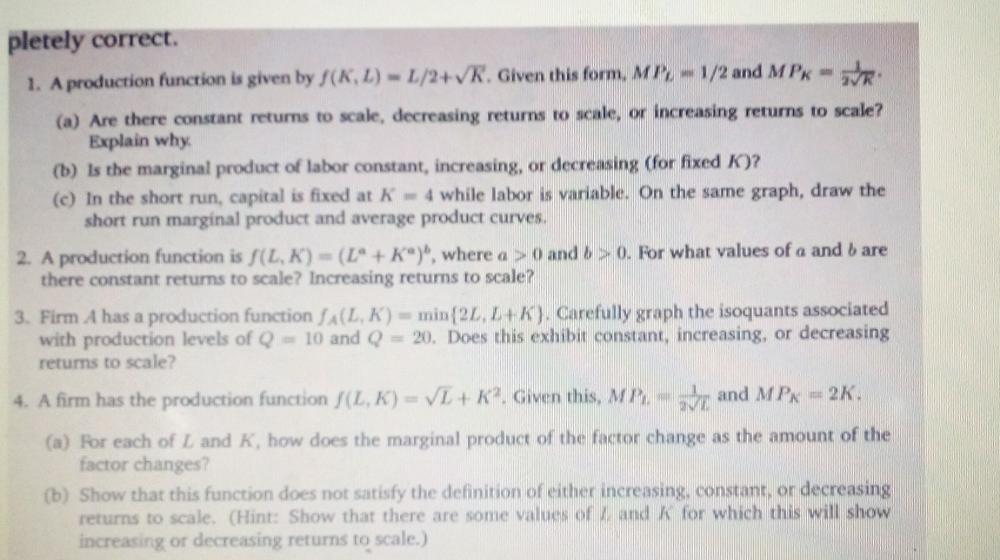

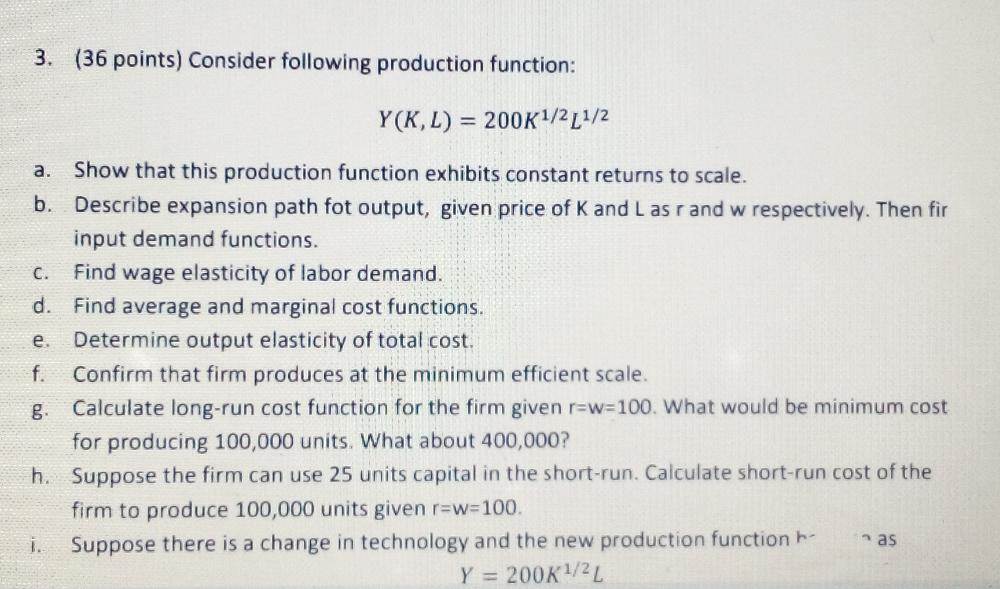

Problem 2 (30 pts) Explain your answers! A firm has a production technology involving two inputs, capital (K) and labor (L). /(K; L) - K1/3LV/3. The price of capital is r; the price of labor is w. and the output price is p. (a) Does the production function of the firm exhibit constant, increasing/ decreasing returns? Justify your answer. (b) Let r - I and w - 4 and assume both inputs are variable. Derive the firm's conditional input demands for producing y units of output, K(y) and (y). What is the firm's cost function ely)? What are the long-run average and marginal cost functions? For any output price p, derive the firm's long run supply function y - S(p). IIp - 4 how much output will the firm produce? (c) Now assume that in the short run the firm's quantity of capital is fixed at K 1. What is the conditional input demand for labor for producing y units of output? What is the short run cost function of the firm. c'fly)? What are the firm's short run average and marginal cost functions? Are there any fixed costs? For any out put price p derive the firm's short run supply function y - 5"(p) of For what out put quantity. ? is K | the optimal long run level of capital? Show that the long run average cost curve (hom ( b) ) and the short run average cost curve (from (c) ) are Cangent al y y'. Explain whypletely correct. 1. A production function is given by f(K. L) - L/2+VK. Given this form. MP - 1/2 and MPk - JR. (a) Are there constant returns to scale, decreasing returns to scale, or increasing returns to scale? Explain why (b) Is the marginal product of labor constant, increasing, or decreasing (for fixed K)? (c) In the short run, capital is fixed at K .= 4 while labor is variable. On the same graph, draw the short run marginal product and average product curves. 2. A production function is f(L, K) - (L- + K"), where a >. ( and 6 2 0. For what values of a and b are there constant returns to scale? Increasing returns to scale? 3. Firm A has a production function fA(L, K) - min (21, I K ). Carefully graph the isoquants associated with production levels of Q = 10 and Q = 20. Does this exhibit constant, increasing, or decreasing returns to scale? 4. A firm has the production function /(L. K) = VL + A?. Given this, MA. and MPx 2K (a) For each of L and K, how does the marginal product of the factor change as the amount of the factor changes? (b) Show that this function does not satisfy the definition of either increasing, constant, or decreasing returns to scale. (Hint: Show that there are some values of I, and & for which this will show increasing or decreasing returns to scale.)3. (36 points) Consider following production function: Y (K, L) = 200K1/2[1/2 a. Show that this production function exhibits constant returns to scale. b. Describe expansion path for output, given price of K and L as r and w respectively. Then fir input demand functions. C. Find wage elasticity of labor demand. d. Find average and marginal cost functions. e. Determine output elasticity of total cost. f. Confirm that firm produces at the minimum efficient scale. g. Calculate long-run cost function for the firm given r=w=100. What would be minimum cost for producing 100,000 units. What about 400,000? h. Suppose the firm can use 25 units capital in the short-run. Calculate short-run cost of the firm to produce 100,000 units given r=w=100. i. Suppose there is a change in technology and the new production function he in as Y = 200K1/2L3. (36 points) Consider following production function: Y (K, L) = 200K1/21 1/2 a. Show that this production function exhibits constant returns to scale. b. Describe expansion path fot output, given price of K and Las r and w respectively. Then find input demand functions. C. Find wage elasticity of labor demand. d. Find average and marginal cost functions. e. Determine output elasticity of total cost. f. Confirm that firm produces at the minimum efficient scale. g. Calculate long-run cost function for the firm given r=w=100. What would be minimum cost for producing 100,000 units. What about 400,000? h. Suppose the firm can use 25 units capital in the short-run. Calculate short-run cost of the firm to produce 100,000 units given r=w=100. i. Suppose there is a change in technology and the new production function become as Y = 200K1/24 Verify this change is capital saving technological progress