Answered step by step

Verified Expert Solution

Question

1 Approved Answer

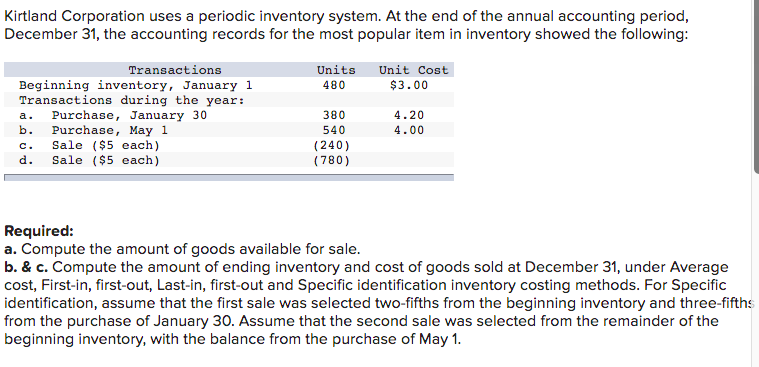

Kirtland Corporation uses a periodic inventory system. At the end of the annual accounting period, December 31, the accounting records for the most popular

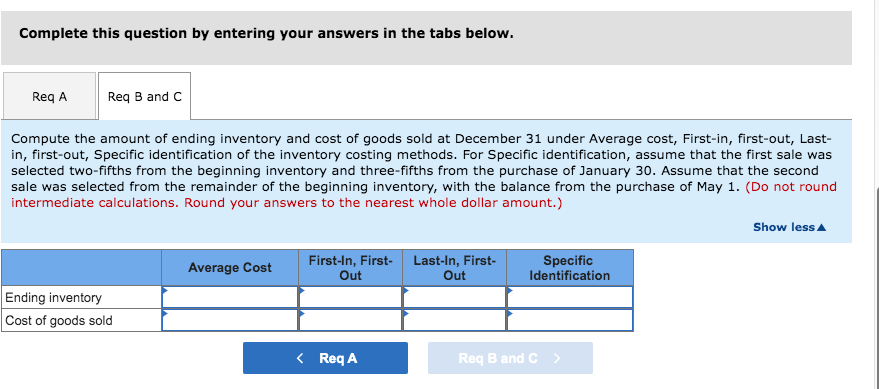

Kirtland Corporation uses a periodic inventory system. At the end of the annual accounting period, December 31, the accounting records for the most popular item in inventory showed the following: Transactions Units Unit Cost Beginning inventory, January 1 Transactions during the year: Purchase, January 30 Purchase, May 1 Sale ($5 each) Sale ($5 each) 480 $3.00 a. 380 4.20 b. 540 4.00 (240) (780) c. d. Required: a. Compute the amount of goods available for sale. b. & c. Compute the amount of ending inventory and cost of goods sold at December 31, under Average cost, First-in, first-out, Last-in, first-out and Specific identification inventory costing methods. For Specific identification, assume that the first sale was selected two-fifths from the beginning inventory and three-fifths from the purchase of January 30. Assume that the second sale was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1. Complete this question by entering your answers in the tabs below. Req A Req B and C Compute the amount of ending inventory and cost of goods sold at December 31 under Average cost, First-in, first-out, Last- in, first-out, Specific identification of the inventory costing methods. For Specific identification, assume that the first sale was selected two-fifths from the beginning inventory and three-fifths from the purchase of January 30. Assume that the second sale was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1. (Do not round intermediate calculations. Round your answers to the nearest whole dollar amount.) Show lessA Average Cost First-In, First- Out Last-In, First- Out Specific Identification Ending inventory Cost of goods sold < Req A Reg B and C Kirtland Corporation uses a periodic inventory system. At the end of the annual accounting period, December 31, the accounting records for the most popular item in inventory showed the following: Transactions Units Unit Cost Beginning inventory, January 1 Transactions during the year: Purchase, January 30 Purchase, May 1 Sale ($5 each) Sale ($5 each) 480 $3.00 a. 380 4.20 b. 540 4.00 (240) (780) c. d. Required: a. Compute the amount of goods available for sale. b. & c. Compute the amount of ending inventory and cost of goods sold at December 31, under Average cost, First-in, first-out, Last-in, first-out and Specific identification inventory costing methods. For Specific identification, assume that the first sale was selected two-fifths from the beginning inventory and three-fifths from the purchase of January 30. Assume that the second sale was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1. Complete this question by entering your answers in the tabs below. Req A Req B and C Compute the amount of ending inventory and cost of goods sold at December 31 under Average cost, First-in, first-out, Last- in, first-out, Specific identification of the inventory costing methods. For Specific identification, assume that the first sale was selected two-fifths from the beginning inventory and three-fifths from the purchase of January 30. Assume that the second sale was selected from the remainder of the beginning inventory, with the balance from the purchase of May 1. (Do not round intermediate calculations. Round your answers to the nearest whole dollar amount.) Show lessA Average Cost First-In, First- Out Last-In, First- Out Specific Identification Ending inventory Cost of goods sold < Req A Reg B and C

Step by Step Solution

★★★★★

3.49 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

Cost of goods so...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Robert Libby, Patricia Libby, Daniel Short

8th edition

78025559, 978-0078025556