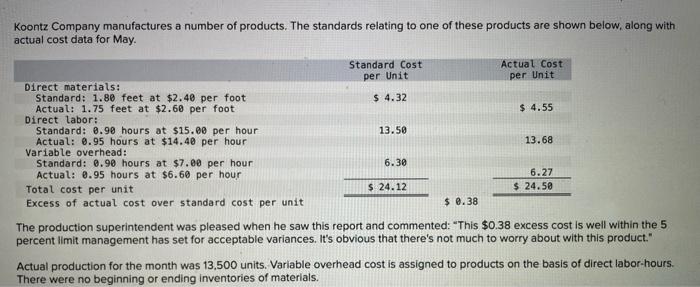

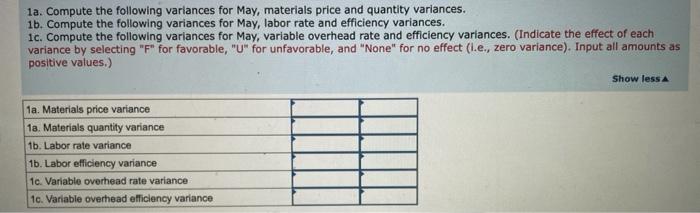

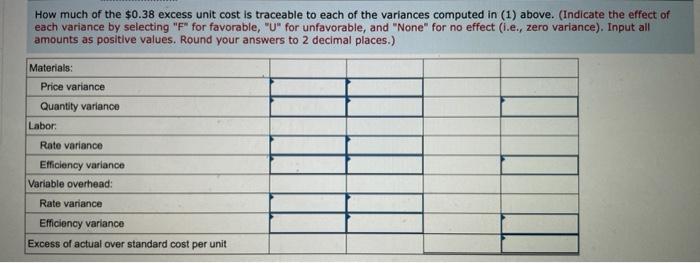

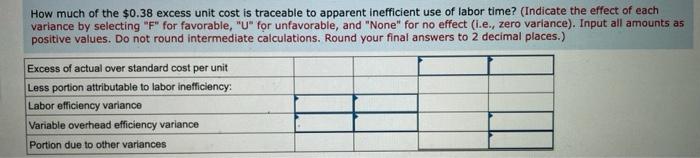

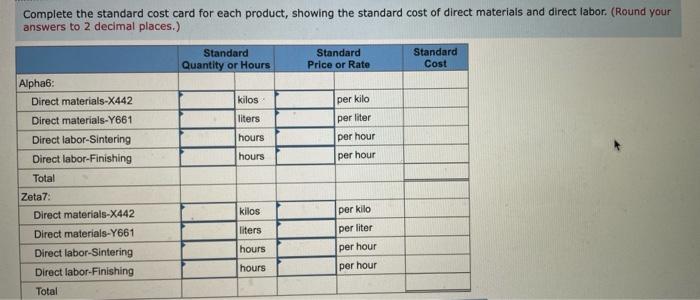

Koontz Company manufactures a number of products. The standards relating to one of these products are shown below, along with actual cost data for May. Standard Cost Actual Cost per Unit per Unit $ 4.32 $ 4.55 13.50 Direct materials: Standard: 1.80 feet at $2.40 per foot Actual: 1.75 feet at $2.60 per foot Direct labor: Standard: 0.99 hours at $15.00 per hour Actual: 0.95 hours at $14.40 per hour Variable overhead: Standard: 0.90 hours at $7.00 per hour Actual: 0.95 hours at $6.60 per hour Total cost per unit Excess of actual cost over standard cost per unit 13.68 6.30 6.27 $ 24.50 $ 24.12 $ 0.38 The production superintendent was pleased when he saw this report and commented: This $0.38 excess cost is well within the 5 percent limit management has set for acceptable variances. It's obvious that there's not much to worry about with this product." Actual production for the month was 13,500 units. Variable overhead cost is assigned to products on the basis of direct labor-hours. There were no beginning or ending inventories of materials. 1a. Compute the following variances for May, materials price and quantity variances. 1b. Compute the following variances for May, labor rate and efficiency variances. ic. Compute the following variances for May, variable overhead rate and efficiency variances. (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (l.e., zero variance). Input all amounts as positive values.) Show less 1a. Materials price variance 18. Materials quantity variance 1b. Labor rate variance 1b. Labor efficiency variance 10. Variable overhead rate variance 1c. Variable overhead efficiency variance How much of the $0.38 excess unit cost is traceable to each of the variances computed in (1) above. (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (.e., zero variance). Input all amounts as positive values, Round your answers to 2 decimal places.) Materials: Price variance Quantity variance Labor Rate variance Efficiency variance Variable overhead: Rate variance Efficiency variance Excess of actual over standard cost per unit How much of the $0.38 excess unit cost is traceable to apparent inefficient use of labor time? (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (i.e., zero variance). Input all amounts as positive values. Do not round intermediate calculations. Round your final answers to 2 decimal places.) Excess of actual over standard cost per unit Less portion attributable to labor inefficiency: Labor efficiency variance Variable overhead efficiency variance Portion due to other variances per liter Complete the standard cost card for each product, showing the standard cost of direct materials and direct labor. (Round your answers to 2 decimal places.) Standard Standard Standard Quantity or Hours Price or Rate Cost Alpha: Direct materials-X442 kilos per kilo Direct materials-Y661 liters Direct labor-Sintering hours per hour Direct labor-Finishing hours Total Zeta7: Direct materials-X442 kilos Direct materials-Y661 liters Direct labor-Sintering hours per hour Direct labor-Finishing hours per hour Total per hour per kilo per liter