Answered step by step

Verified Expert Solution

Question

1 Approved Answer

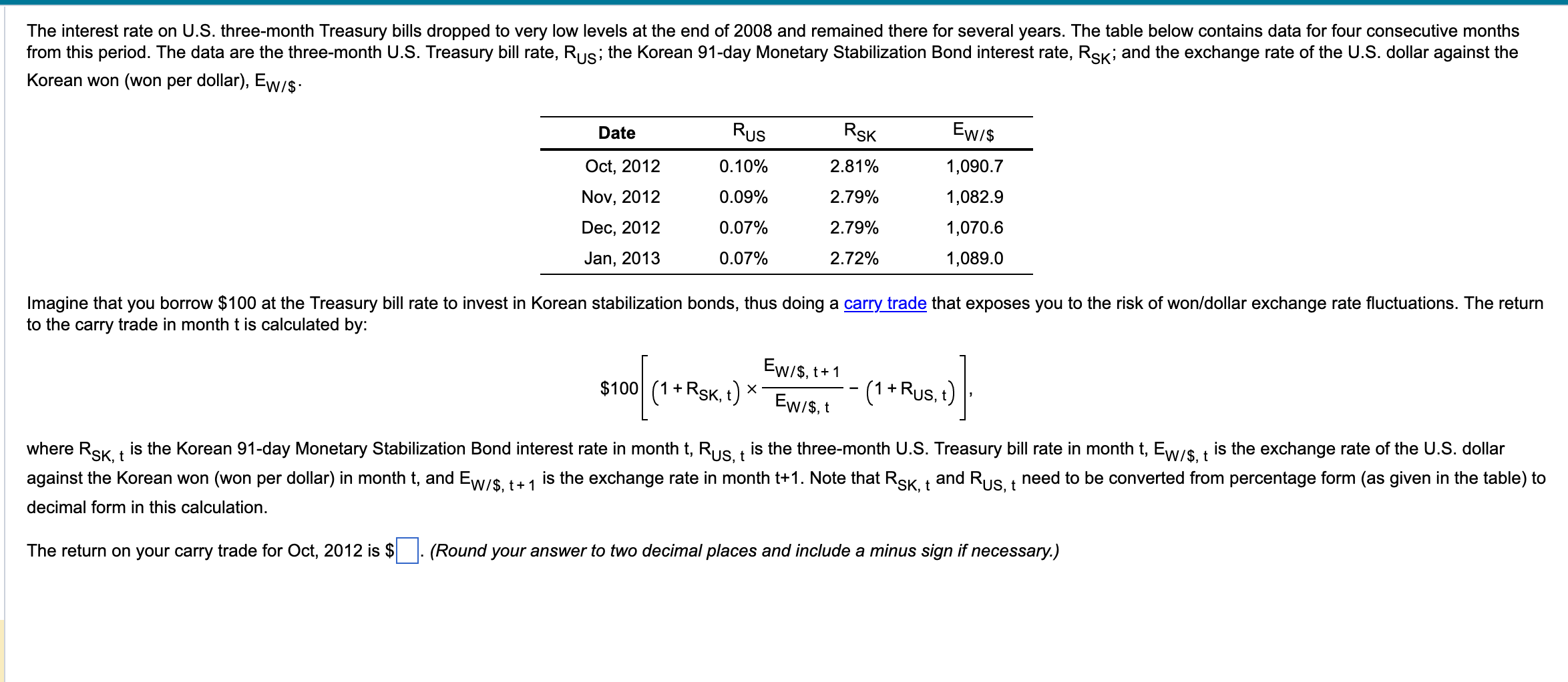

Korean won (won per dollar), EW/$. Imagine that you borrow $100 at the Treasury bill rate to invest in Korean stabilization bonds, thus doing a

Korean won (won per dollar), EW/$. Imagine that you borrow $100 at the Treasury bill rate to invest in Korean stabilization bonds, thus doing a that exposes you to the risk of won/dollar exchange rate fluctuations. The return to the carry trade in month t is calculated by: $100[(1+RSK,t)EW/$,tEW/$,t+1(1+RUS,t)] decimal form in this calculation. The return on your carry trade for Oct, 2012 is $ (Round your answer to two decimal places and include a minus sign if necessary.)

Korean won (won per dollar), EW/$. Imagine that you borrow $100 at the Treasury bill rate to invest in Korean stabilization bonds, thus doing a that exposes you to the risk of won/dollar exchange rate fluctuations. The return to the carry trade in month t is calculated by: $100[(1+RSK,t)EW/$,tEW/$,t+1(1+RUS,t)] decimal form in this calculation. The return on your carry trade for Oct, 2012 is $ (Round your answer to two decimal places and include a minus sign if necessary.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Infrastructure Planning And Finance

Authors: Vicki Elmer, Adam Leigland

1st Edition

0415693187, 978-0415693189